Анализ статистических данных в MINITAB - Моделирование временного ряда (Time Series Forecasting)

Подождите немного. Документ загружается.

Chapter 13

Time Series Forecasting

Topics to be covered in this chapter:

Time Series Plot

Trend Analysis

Seasonal Patterns

Decomposition

Autocorrelation

Moving Average Models

Exponential Smoothing Models

Time Series Plot

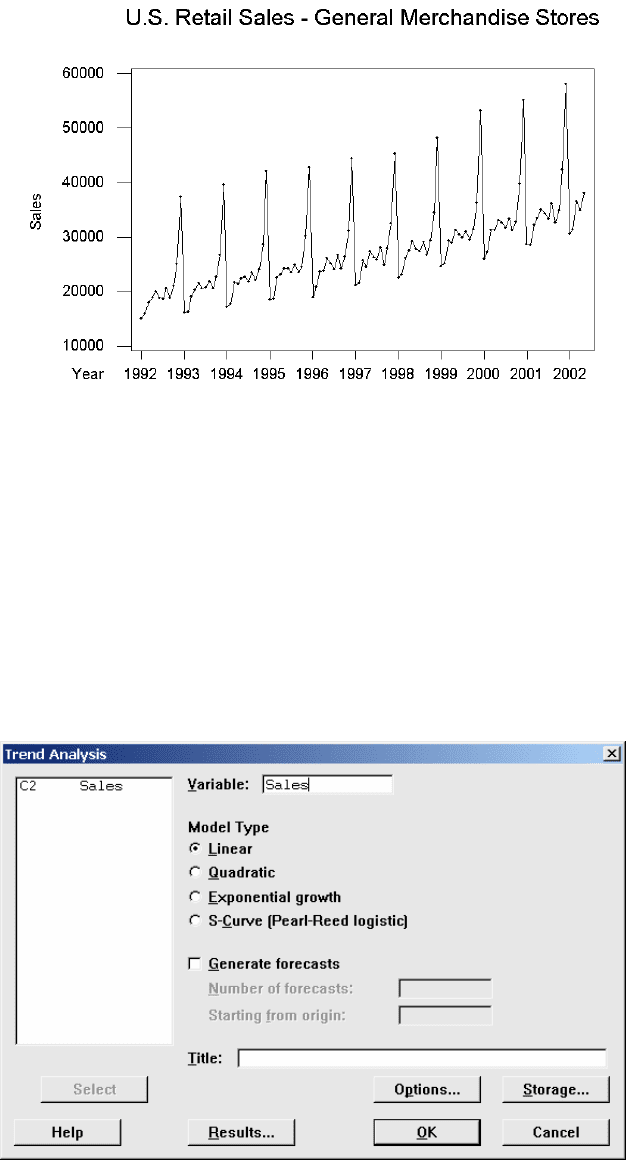

Example 13.1 of PBS discusses monthly retail sales of General Merchandise Stores beginning January

1992 and ending May 2002 (125 months). The data are provided in EG13_001.MTW. Minitab can be

used to plot the monthly retail sales by selecting

Stat h Time Series h Time Series Plot

from the menu. This command plots measurement data on the y-axis versus time data on the x-axis.

Minitab assumes that the y-axis data occurred in the order that the values appear in the column, in

equally spaced time intervals. If the data did not occur that way, you may want to use

Graph h Plot

to plot the y-axis data versus a date/time column on the x-axis.

In the dialog box, Graph variables defines the variables to be used in each graph. Under Y en-

ter a column containing the observations on the graph. The x-axis is automatically the time axis. The

x-axis time scales can be labeled with values from a date/time column, called a date/time stamp, or with

time units chosen in the dialog box: index units, calendar units, or clock units.

203

204 Chapter 13

Click on the Annotation button to add a title to the plot. You can also change the default start

time, suppress time unit scales, or tell Minitab to use a different time interval by clicking on the Options

button. For each time unit axis shown in the Options sub-dialog box, check the box to show the time

scale, or uncheck the box to suppress the axis. This is useful for getting rid of cluttered axes. For the

retail sales data, we uncheck the box to suppress the month axis:

Time Series Forecasting 205

Since January 1992, overall sales have gradually increased and a distinct pattern repeats itself

approximately every 12 months.

Trend Analysis

Example 13.2 of PBS discusses monthly retail sales of General Merchandise Stores beginning January

1992 and ending May 2002 (125 months). The pattern of increasing growth in the time series plot of

the retail sales data is an example of a linear trend. Minitab can be used to estimate the linear trend.

Select

Stat h Time Series h Trend Analysis

from the menu. This command fits a general trend model to time series data and provides forecasts.

You can choose among linear, quadratic, exponential, and S-curve models. To forecast future sales,

check Generate forecasts and enter a number in Number of forecasts. In the Starting from origin box,

enter a positive integer to specify a starting point for the forecasts. If you leave this space blank, Mini-

206 Chapter 13

tab generates forecasts from the end of the data. For the retail sales data, we enter Sales as the Variable

and under Model Type, choose Linear. Minitab estimates the linear trend to be

Y

t

= 18736.5 + 145.53 t

where t is the number of months elapsed beginning with the first month of the time series.

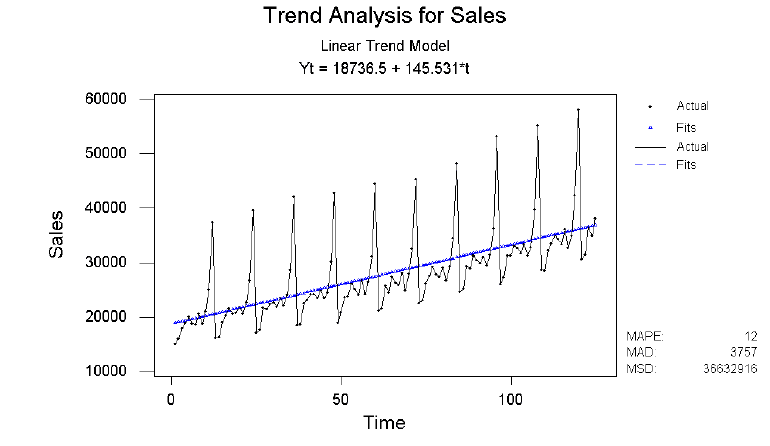

Trend Analysis

Data Sales

Length 125.000

NMissing 0

Fitted Trend Equation

Yt = 18736.5 + 145.531*t

Accuracy Measures

MAPE: 12.4750

MAD: 3756.77

MSD: 36632916

The trend analysis includes a graphic display plot as shown below. To turn the graphics display on (or

off), click on the Results button in the trend analysis dialog box.

We can also use regression techniques to fit a linear model to the above data. This gives additional out-

put, such as the

value for the model. First, select

2

R

Calc h Make Patterned Data h Simple Set of Numbers

from the menu to create a variable x (or t), where x is the number of months

elapsed, beginning

with the first month of the time series. That is, x = 1 corresponds to January 1992, x = 2 corresponds to

February 1992, etc. Next, select

Time Series Forecasting 207

Stat h Regression h Regression

from the menu. Enter Sales as the response variable and x as the predictor variable and click OK.

Regression Analysis: Sales versus x

The regression equation is

Sales = 18736 + 146 x

Predictor Coef SE Coef T P

Constant 18736 1098 17.06 0.000

x 145.53 15.12 9.62 0.000

S = 6102 R-Sq = 42.9% R-Sq(adj) = 42.5%

Analysis of Variance

Source DF SS MS F P

Regression 1 3446933715 3446933715 92.59 0.000

Residual Error 123 4579114499 37228573

Total 124 8026048215

The trend-only model ignores the seasonal variation in the retail sales time series. Notice that the

value for the trend-only model is 42.9% or 0.429.

2

R

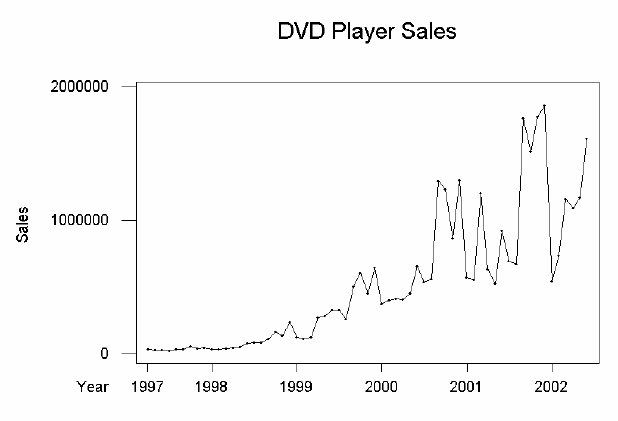

Case 13.1 of PBS discusses the sales of DVD players since the introduction of the DVD format

in March 1997. At the end of June 2002, nearly 33 million DVD players had been sold in the U.S. with

over 18,000 titles available in the DVD format. The Consumers Electronic Association tracks monthly

sales of DVD players. The data are provided in CA13_001.MTW. Select Stat h Time Series h Time

Series Plot from the menu to plot the DVD sales data.

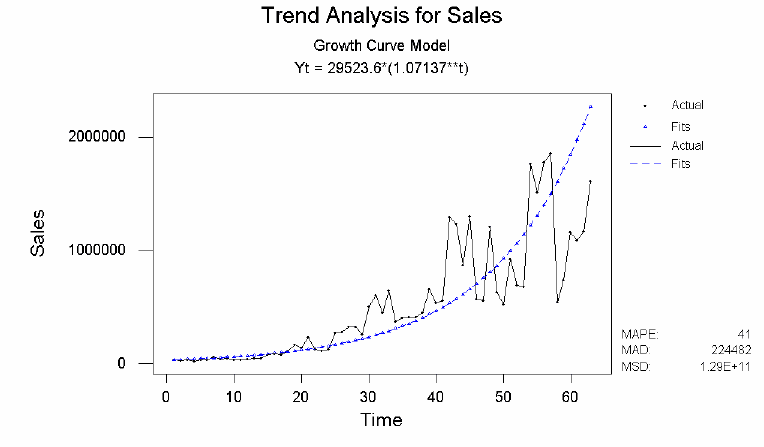

The pattern of increasing growth in this plot is an example of an exponential trend. Minitab

can be used to estimate the exponential trend. Select Stat h Time Series h Trend Analysis from the

menu. In the dialog box, enter Sales as the Variable. Under Model Type, choose Exponential growth.

As shown in the trend analysis, Minitab estimates the exponential trend to be

)07137.1(6.29523

t

t

Y =

208 Chapter 13

where t is the number of months elapsed, beginning with the first month of the time series. Since

1.07137 is equal to e

0.06894

, this is equivalent to the model given in Case 13.1 of PBS.

Trend Analysis

Data Sales

Length 63.0000

NMissing 0

Fitted Trend Equation

Yt = 29523.6*(1.07137**t)

Accuracy Measures

MAPE: 40.6388

MAD: 224482

MSD: 129023909665

The graphic display plot illustrates the exponential growth together with the raw data.

Seasonal Patterns

A trend equation may be a good description of the long run behavior of the data, but we need to account

for short run phenomena like seasonal variation to improve the accuracy of our forecasts. As in Exam-

ple 13.3 of PBS, we can use indicator variables to add the seasonal pattern to the trend model for the

monthly retail sales data. First, select

Calc h Make Patterned Data h Simple Set of Numbers from

the menu to create a new variable Month that takes the value 1 for each January, 2 for each February,

…. and 12 for each December in the data set. Next select

Calc h Make Indicator Variables

from the menu. In the dialog box, enter Month under Indicator variables for, and specify 12 new col-

umns in the Store results in textbox. This will create 12 indicator variables, one for each month. Name

the indicator variables X1, X2,…,X12. Select

Stat h Regression h Regression from the menu and

Time Series Forecasting 209

enter Sales as the response variable. Enter x and all 12 indicator variables as the predictor variables and

click OK. (Recall that we defined the variable x in the previous section as the number of months

elapsed beginning with the first month of the time series). We get the following output from Minitab:

Regression Analysis: Sales versus x, X1, ...

* X12 is highly correlated with other X variables

* X12 has been removed from the equation

The regression equation is

Sales = 37473 + 140 x - 24276 X1 - 23749 X2 - 20271 X3 - 20250 X4 - 18518 X5

- 19575 X6 - 20324 X7 - 18627 X8 - 20878 X9 - 18933 X10 - 13842 X11

Predictor Coef SE Coef T P

Constant 37472.7 343.4 109.14 0.000

x 140.130 2.393 58.57 0.000

X1 -24276.2 421.4 -57.61 0.000

X2 -23748.7 421.4 -56.36 0.000

X3 -20271.2 421.3 -48.11 0.000

X4 -20250.5 421.3 -48.07 0.000

X5 -18518.0 421.3 -43.96 0.000

X6 -19574.5 431.4 -45.37 0.000

X7 -20323.6 431.3 -47.12 0.000

X8 -18626.9 431.3 -43.19 0.000

X9 -20878.1 431.2 -48.42 0.000

X10 -18933.0 431.2 -43.91 0.000

X11 -13842.2 431.2 -32.10 0.000

S = 964.1 R-Sq = 98.7% R-Sq(adj) = 98.6%

Analysis of Variance

Source DF SS MS F P

Regression 12 7921942577 660161881 710.22 0.000

Residual Error 112 104105638 929515

Total 124 8026048215

Minitab automatically removes the last indicator variable from the equation because it is highly

correlated with the first 11 indicator variables. The

value for the trend-and-season model is 98.7%

which is a dramatic improvement over the trend-only model. Recall that the

value for the trend-

only model was 42.9%.

2

R

2

R

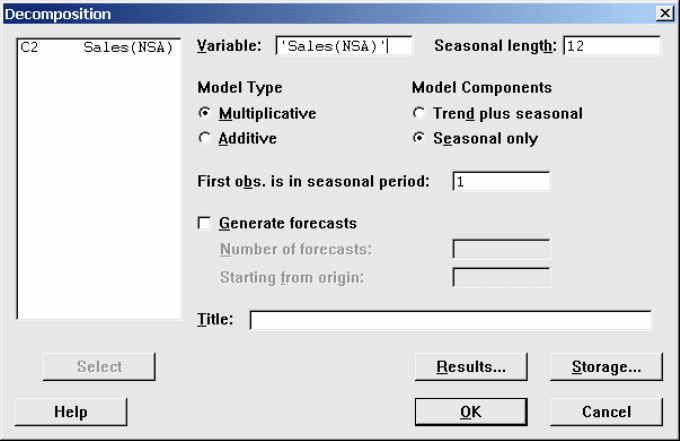

Decomposition

Another approach to accounting for seasonal variation is to calculate an adjustment factor for each sea-

son. The trend is adjusted each particular season by multiplying it by the appropriate seasonality factor.

Using seasonality factors views the model as a trend component times a seasonal component.

Y = TREND

× SEASON

Example 13.4 of PBS calculates the seasonality factors for the retail sales data. Minitab can be used to

calculate seasonality factors by selecting

Stat h Time Series h Decomposition

from the menu. You can use decomposition to separate the time series into linear trend and seasonal

components. You can choose whether the seasonal component is additive or multiplicative with the

trend.

210 Chapter 13

In the dialog box, enter the column containing the time series under Variable, and a positive in-

teger as the Seasonal length. Since the retail sales data is monthly data, we use a seasonal length of 12.

Under Model Type choose Multiplicative, and under Model Components choose Seasonal only. By

default the first observation is in seasonal period one because Minitab assumes that the first data value

in the series corresponds to the first seasonal period. Enter a different number to specify a different

starting value. Check Generate forecasts if you want to generate forecasts.

Minitab calculates the following seasonality factors for the retail sales data:

Time Series Decomposition

Data Sales(NSA)

Length 125.000

NMissing 0

Seasonal Indices

Period Index

1 0.781569

2 0.805703

3 0.919066

4 0.930090

5 0.988080

6 0.958632

7 0.931024

8 0.984559

9 0.910419

10 0.982894

11 1.15661

12 1.65135

These seasonal indices (or seasonality factors) differ slightly from the indices in Example 13.4 of PBS.

This is because in Minitab the data is smoothed before the seasonal indices are found.

Time Series Forecasting 211

Autocorrelation

The residuals from a regression model that uses time as an explanatory variable should be examined for

signs of autocorrelation. Examples 13.7 and 13.8 of PBS examine the residuals that result from fitting

an exponential trend to the DVD player sales data. The data are provided in CA13_001.MTW. First,

select

Calc h Calculator from the menu and calculate log

e

(Sales). Name this column lnSales. Next,

select

Stat h Regression h Regression from the menu and regress lnSales on the predictor variable x,

where x is the number of months elapsed beginning with the first month of the time series. In the dialog

box, click on the Storage button and check Residuals to obtain the residuals from the exponential trend

model. Finally, select

Graph h Plot from the menu and plot the residuals versus x, i.e., in time order.

The pattern in the plot indicates positive autocorrelation among the residuals. An alternative plot for

detecting autocorrelation is a lagged residual plot. Select

Stat h Time Series h Lag

from the menu. In the dialog box, enter the column containing the variable that you want to lag under

Series. Under Store lags in, select the storage column for the lags and then specify the value for the lag.

To lag the residuals of the DVD Sales data, specify a lag of one and name the output column lag_RES.

212 Chapter 13

Since the lag selected is one, Minitab moves the row elements of a column down one row. There will

be one missing value symbol (*) at the top of the output column. The output column has the same

number of rows as the input column, so the last value from the input column is not lagged.

Next, select

Graph h Plot from the menu and plot the residuals versus the lagged residuals. The graph

on the following page shows a linear pattern with positive slope. This indicates that the residuals may

have positive autocorrelation

.