ACCA P7 (INT) Advanced Audit & Assurance - Study Text - 2010 (Emile Woolf Publishing)

Подождите немного. Документ загружается.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 435

A depreciation policy needs to be formulated to write off the cost of the

refurbishment over its ‘useful life’. In order to establish this, a decision

will need to be made as to how long the refurbishment will accrue

benefits before more refurbishment (e.g. the refit in point (3)) is needed.

Given that this life may not be as long as that of the leases themselves, it

would seem appropriate to categorise these costs separately in non-

current assets, i.e. not as part of the short leaseholds.

Auditing issues

Again, this area is likely to remain material given the planned

expansion.

Although it should be relatively straightforward to vouch the costs

included, it will be difficult to assess the ‘useful life’ of the

refurbishments.

However, it does seem likely (especially given the refit described in

point (3)) that a facelift will be needed every so many years, making it

unlikely that these costs should be amortised over the same period as

the leases themselves.

(3) Image survey/refit

Accounting issues

Again, there is the problem of whether a clear future economic benefit

(i.e. an asset) arises from these costs and if so for how long.

If the independent survey supports increased revenue because of the

refit then the costs could be carried forward over the periods expected to

benefit from this image.

If future benefits are not ‘probable’ then the costs should be written off

immediately.

Auditing issues

The audit firm will need to consider the materiality of these costs though

it seems likely that they will be material this year.

In any case, in the first year of audit, the firm should establish a

precedent for such costs for the future.

Even if future benefits are ‘probable’ it will be very difficult to establish

the period which may benefit.

(b) Further information

(1) Amortisation of lease premiums

The size of the lease premiums.

The frequency of such premiums being associated with a period of

reduced rent.

The length of the period of reduced rent.

Dates of the rent reviews.

Paper P7 INT: Advanced audit and assurance

436 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The likely increase in rents.

The likelihood of the company selling the site before the end of the

lease term.

History of selling sites during the lease term.

(2) Refurbishment of new sites

The frequency of refurbishment after the initial refurbishment.

Whether future plans include such refurbishments.

The materiality of the rates/services capitalised.

(3) Image survey/refit

The date and success of the last major refit.

Frequency and success of similar refits in similar companies.

A copy of the survey.

Whether there are documented plans for any more such refits.

21 Marvellous Manufacturing

(1) Redundancy payments

Enquiries

Are additional redundancies likely in the foreseeable future?

What are the reasons for the redundancies (e.g. reorganisation of

operations)?

Are the redundancies associated with the discontinuance of a business

segment?

When were the directors’ plans re the redundancies announced to the

workforce/made public?

Evidence

Client schedule showing the make-up of the provision for agreement to

payroll and personnel records.

Post year end cash book payments to confirm amounts provided.

Redundancy notices/board minutes to confirm the date on which the

decision was made.

Sales order books to establish the impact on sales levels arising from the

redundancies.

(2) Bad debt

Enquiries

What steps are being taken to find new customers to lessen the impact of

the loss of Rafters Retail?

Were any inventories manufactured to order for Rafters Retail?

Have such goods been separately identified in year end inventories?

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 437

What steps are being taken to recover the debt (e.g. attending meetings

arranged by the liquidator)?

How much of the debt is likely to be recoverable?

Evidence

Correspondence with the liquidator to establish the likelihood/amount of

debt recovery.

Schedule of inventory provision to establish if any provision was made

against goods manufactured to order for Rafters Retail.

Insurance policy documents (if insured for such losses).

The make-up of the current balance (i.e. year end balance and/or post year

end transactions).

(3) Claim by former sales director

Enquiries

Why was the director dismissed?

What is the nature of the alleged breach?

What are the company’s intentions? (e.g. out of court settlement)

Evidence

The service agreement, in order to establish whether the director’s action is

in accordance with its terms.

Legal correspondence/board minutes to assess the most likely course of

action/outcome and the amounts involved.

The director’s personnel records including dismissal notice etc.

Post year end cash book payments to the former director.

(4) Fire destroying inventories

Enquiries

To what extent have inventories been replaced since the fire?

To what extent were manufacturing processes disrupted by the loss of raw

materials inventories?

Have orders/customer goodwill been lost due to delays in despatching

goods to customers?

What was the cause of the fire?

Evidence

Insurance policy, to establish extent to which the loss of inventories (and

any consequential loss) is recoverable.

Correspondence with insurers to ascertain whether claim will be settled in

full.

Sales order books to establish any significant loss in customer goodwill.

Paper P7 INT: Advanced audit and assurance

438 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Cash book payments to suppliers for ‘emergency’ purchases of raw

materials.

22 Wally’s Wines

(a) Audit procedures

Re profit forecast

Check the validity of the assumptions on which it was based.

Check that accounting policies used are valid in the circumstances and

consistent with the company’s usual policies.

Check the calculations.

Consider the likelihood of the forecast being achieved, i.e. the likely

success of the repositioning.

Consider whether Wally’s Wines has the marketing/selling expertise to

achieve this or, if not, whether they are planning to buy such expertise in.

Check that the costs of the above have been built into the forecast.

Check that future interest charges on the new borrowings have been built

into the forecast.

Consider the accuracy of any previous forecasts.

Consider the reliability of any external advice taken.

Re cash flow projection for the year to 31

st

March 20X8

Ensure that after settling liabilities the new loan will be sufficient.

Ensure all cash requirements have been taken into account.

Compare the cash flow forecast for the first month(s) with actual results to

assess accuracy.

Other

Consider the likelihood of obtaining the new loan, including any

indications given by the bank to date and any interim correspondence.

Ask the directors whether there are any alternative sources of finance

which may be available if the bank does not grant the loan. If there is,

obtain confirmation from the likely source that this would be available.

Inform the directors that unless your firm is satisfied that the required

finance can be obtained, you will modify your audit opinion – therefore

some confirmation from the bank (or other lender) must be obtained.

Consider whether even if the bank will not get a new loan it might extend

the existing loan.

Discuss with the directors whether the annual general meeting (and

therefore the signing of the audit report) could be postponed until the

bank has made their decision.

Consider the position of the company if new finance is not obtained. Could

the company sell surplus non-current assets? Is the existing loan secured

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 439

over any of the company’s assets or by personal guarantees of the

directors?

Consider seeking advice from an insolvency practitioner.

Consider the company’s previous experience and success in renewing

finance.

Review board minutes.

(b) Alternative audit opinions

Unmodified opinion

If the audit firm can satisfy itself that the going concern assumption is

appropriate.

Modified report with an emphasis of matter paragraph

Where the going concern assumption is appropriate but a material uncertainty

exists and the financial statements:

adequately disclose the principal events or conditions that may cast

significant doubt on the entity’s ability to continue as a going concern and

management’s plans to deal with those events or conditions , and

disclose clearly that there is a material uncertainty related to those events

or conditions.

Qualified or adverse opinion

Where there is not adequate disclosure of the above then the audit firm should

express a qualified or adverse opinion on the grounds of a material

misstatement (in respect of disclosure).

Where the going concern assumption is inappropriate

Where the going concern assumption is inappropriate, the audit firm should

express:

an adverse opinion if the financial statements have been prepared on a

going concern basis

an unmodified opinion if the financial statements have been prepared on

an alternative acceptable basis (e.g. break-up basis) and there is adequate

disclosure of this basis. An emphasis of matter paragraph may be required.

23 The Pepper Group

(a) Approach to planning and controlling the group audit

Planning

Obtain the instructions issued by head office for the preparation of the

group’s financial statements.

Obtain the timetable for the production of the individual financial

statements and the group financial statements.

Ensure that there is a standard format and layout of subsidiary financial

statements to facilitate consolidation.

Paper P7 INT: Advanced audit and assurance

440 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Consider audit staffing and skills required.

Liaise with component auditors of subsidiaries.

Consider potential problems that may arise, for example with Hybrid.

Consider the risks arising from the group relative to the subsidiaries.

Consider any additional procedures that may be required for subsidiaries

being audited by component auditors.

Consider whether materiality levels are acceptable.

Use questionnaires for the subsidiaries to establish accounting policies,

accounting details needed for consolidation but not available from the

accounts and information relevant for group accounts but not for

subsidiaries’ own accounts.

Controlling

The group audit will be subject to the same control and quality checks as any

other audit, including maintenance of documented files with auditors’

decisions documented, file review, supervision and discussion with

management. Effective planning, allocation of staff and review procedures for

group audits are all important elements of control.

(b) Impact of each issue on the group audit

(1) Hybrid

If Hybrid continues to make losses, the directors of Pepper may consider

there to have been an impairment in the value of the holding company’s

investments. If that is the case, the auditor will need to confirm that any

write-down is adequate by examining:

the extent of support to Hybrid by Pepper/what element of the $10

million guarantees relates to Hybrid

Hybrid’s cash flow projections

the extent of disclosure of guarantees in Pepper’s financial

statements.

There are clearly material problems for the subsidiary itself but

consideration needs to be made as to whether these issues are also

material to the group as a whole and whether the subsidiary control

problems are symptomatic of a wider problem.

If the issues are material to the group, then the impact on the audit

report will need to be considered.

(2) Cayenne

Cayenne’s year-end precedes that of the group by two months and

therefore figures used for this subsidiary will either be estimated or out-

of date in the group financial statements.

IAS 27 Consolidated and separate financial statements requires the

consolidated financial statements to be prepared as at the same

reporting date. Therefore, Cayenne should be made to prepare

additional financial statements as at the group year end – unless it is

impracticable to do so.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 441

If it is impracticable, provided the difference is no more than three

months (as is the case here), the October 20X1 financial statements may

be used provided adjustments are made for any significant transactions

or events occurring in November and December. The auditor will need

to consider whether any such adjustments need to be and have been

made.

(3) Habenaro

As the announcement was not made until after the year end, this is a

non-adjusting subsequent event that will have a significant impact on

the group statement of financial position. The auditor will need to

ensure adequate disclosure in the financial statements.

(4) Guarantees

These loans are an important liability for Pepper Group and the auditor

will need to ensure that there is appropriate disclosure in the financial

statements.

(c) Relationship with component auditors

The group auditor has overall responsibility for expressing an opinion on the

group financial statements and therefore needs to confirm that he is satisfied

with the work undertaken by the subsidiary auditors (referred to by ISA 600

as ‘ component auditors’ where they are not also the group auditor).

In reviewing the work of the component auditors, the group auditor needs to

confirm the following:

That all significant risks of material misstatement of the group financial

statements have been addressed in the audit of the components.

Whether there are any reasons why he cannot rely on the work of the

component auditors (for example, a lack of competence, independence, or

local regulation of auditors).

The materiality of the issues raised in the component financial statements

in relation to the group materiality level (in particular Hybrid, which

seems to be of most significant concern).

If a joint audit is to be undertaken, then it is important that the scope and

responsibilities are agreed and documented. This will involve a preliminary

meeting to agree approach, timing, staffing, responsibilities and working

papers.

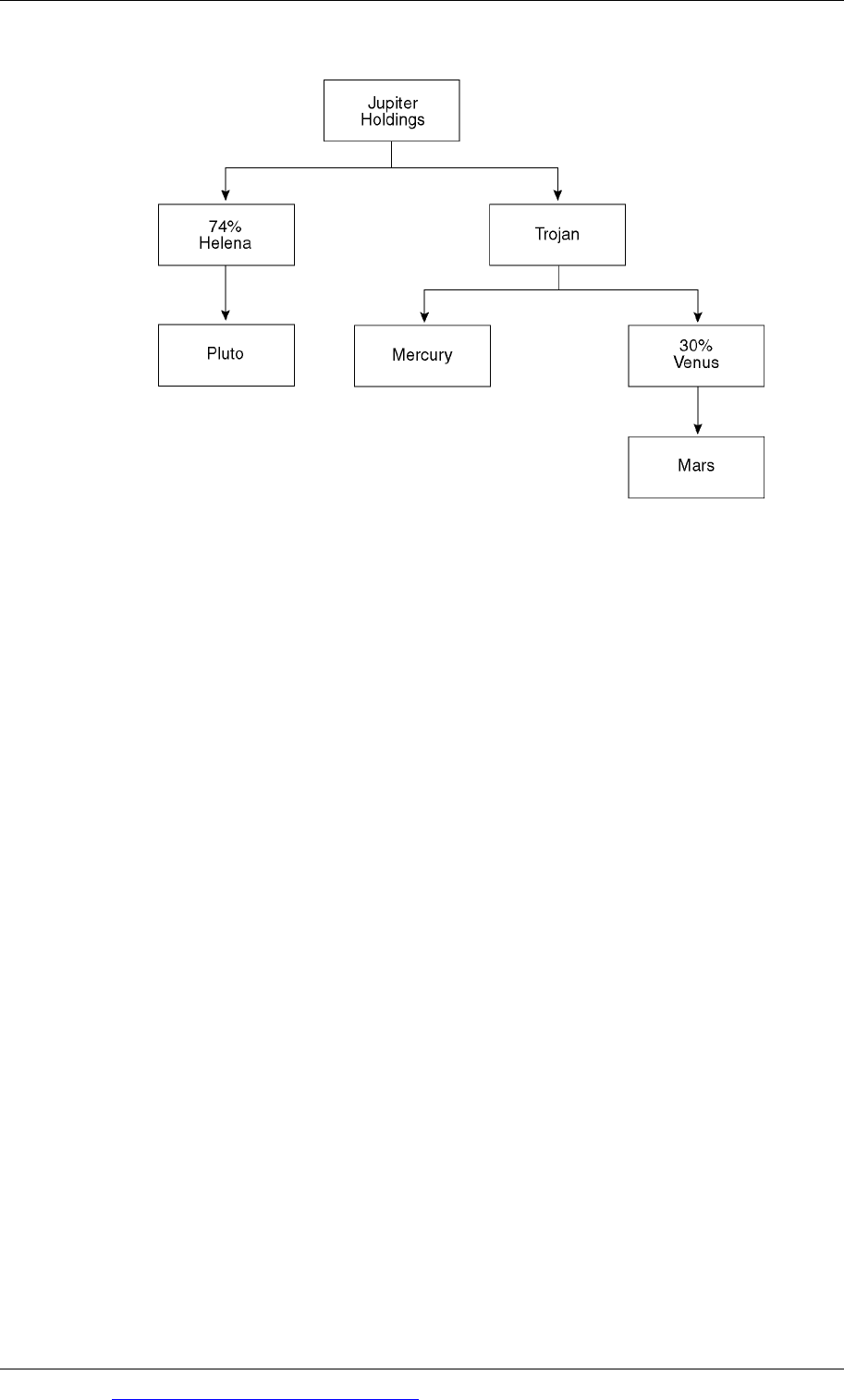

24 Jupiter Holdings

Planning notes: year ended 31

st

December 20X4

(a) The Helena audit

Engagement letter for Helena will need revising now that group financial

statements are to be prepared.

In respect of the acquisition of Pluto from Trojan.

− Method of finance used to raise the $1 million and any impact thereof.

Paper P7 INT: Advanced audit and assurance

442 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

− Whether special accounts were prepared at 30

th

November 20X4. If so,

these may be of use for the audit.

− Whether a fair value exercise was carried out.

− Check that Helena is applying the Jupiter group accounting policies re

goodwill, foreign exchange etc.

The timetable for the Helena audit and consolidation needs to be linked

into the Jupiter consolidation/audit.

Consider the level of assistance/information required by the auditors of

Interesting Investments (Helena may be classified as an associate of

Interesting Investments).

The results of Pluto need to be consolidated by Helena from 30

th

November 20X4 and disclosed appropriately in the Helena group income

statement/statement of comprehensive income.

Discussion of the effect on group structure and operations of Interesting

Investments taking a non-controlling interest in Helena.

(b) The Jupiter Holdings audit

General

Agreement of year-end timetable with client.

Given the various events during the year, discussions need to be held with

the board of the reasons behind each change, as there may be further

(going concern?) implications for the group.

This year’s audit is likely to be higher risk than last year’s. We need to

assess the implications for audit approach/staffing.

Ensure usual information re intra-group trading/balances is available in

order to eliminate on consolidation.

Everything that follows suggests that the work will need to be budgeted

very carefully. A fee increase would seem likely to be necessary.

Helena

Authorisation of disposal of shares by shareholders of Jupiter.

Correct calculation of any profit/loss on disposal.

Disclosure of that profit/loss.

Correct calculation of non-controlling interests.

Trojan

Contact Swiss office re audit approach/deadlines.

Confirm Swiss office still following firm’s world-wide audit/ethical

standards.

Require usual proforma accounts for consolidation.

Correct calculation of any profit/loss on disposal of Pluto.

Any profit/loss on sale of Pluto will need to be eliminated on

consolidation.

Enquire re use of cash from sale of Pluto by Trojan.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 443

Consider what involvement we need in the work performed by the Swiss

office. As a minimum:

− prepare a letter of instruction and organise a review of the Swiss

office’s report of work performed

− discuss the business activities of Trojan that are significant to the group

− discuss the risk of material misstatement of Trojan’s financial

statements with the Swiss office, and

− review the Swiss office’s documentation of identified significant risks

of misstatement.

Mercury

Although Mercury has not previously been material, we need to confirm

this is still the case.

In any case we should encourage the board to appoint auditors.

If a firm other than our associate is appointed, and we decide we need to

be involved in the audit, as a minimum, prepare a letter of instruction and

organise a review of the auditor’s report of work performed.

Venus and Mars

Need to establish the degree of influence that Trojan can exert over the

Venus group. If significant the group will need to equity account for the

Venus group from 1

st

August.

The results of Mars will need to be consolidated up until 1

st

August and

may need to be classified as discontinued, together with any profit/loss on

disposal.

We will need to be satisfied that the work of the (small) Australian firm

can be relied upon. Assuming that it can be, then, as a minimum, perform

the work listed under Trojan above. If further audit procedures are

considered necessary, decide whether that work can be carried out by the

Australian firm or should be carried out by ourselves.

If their work cannot be relied upon consider what procedures we need to

perform ourselves in order to obtain sufficient appropriate evidence and

reach an opinion on the group financial statements.

Paper P7 INT: Advanced audit and assurance

444 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Working

25 Audit-related services

(a) A review engagement

In a review engagement the accountant is engaged to review but not audit

financial or other information.

The work performed is less detailed than for an audit. As a result, the level of

assurance provided is seen to be moderate as opposed to the high assurance

given by an audit.

A review engagement could be:

an attestation engagement, or

a direct reporting engagement.

In an attestation engagement, an accountant might be engaged to attest to

(vouch for) the fact that certain procedures within an entity have been

performed. He will not comment on the quality of the procedures, merely that

they have been performed.

In a direct reporting engagement, an accountant will carry out an independent

examination of financial or other information prepared by his client for use by

a third party. The resultant special report will be on some aspect of his client’s

affairs and will usually provide negative assurance.

One of the most common forms of direct reporting engagement is ‘due

diligence’ work.

In the context of mergers and takeovers, Entity X, taking over Entity Y, is

likely to require a due diligence report into the valuation of the assets and

liabilities of Entity Y.