ACCA P7 (INT) Advanced Audit & Assurance - Study Text - 2010 (Emile Woolf Publishing)

Подождите немного. Документ загружается.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 385

(2) In the year to 31

st

January 20X5, John Smith received a bonus of $200,000, but

you were unable to obtain any information in respect of the calculation and

authorisation of the bonus. No other director of Top Toys received a bonus in

that year and the next highest paid director received a total emoluments

package of $30,000.

(3) There is a dispute with a major supplier over the credit facilities offered to Top

Toys. The supplier manufactures and supplies 30% of the Top Toys’ purchases

and claims that Top Toys has continually exceeded its credit period and that

its accounting staff are impatient and incompetent.

(4) The company’s overdraft limit of $250,000 is due for renegotiation in April

20X6.

Required

Identify the potentially high risk areas of the audit.

17 Red Recruitment

Your firm has recently been appointed auditor of Red Recruitment, a small

company set up two years ago by the managing director, Roy Red, who was

previously an investment banker. The initial capital was provided equally by Roy

and the bank. The bank loan and the current overdraft facility are secured on the

company’s assets. The overdraft is running just under its limit.

The company places highly qualified personnel in management positions. Roy

employs the following staff:

A senior recruitment consultant, Greta Green.

Three other recruitment consultants.

An office manager, Bob Blue.

A bookkeeper, Paula Pink.

Greta places clients in employment and supervises and trains the other recruitment

consultants.

Bob is in charge of all office administration. He raises invoices for fees when Roy

instructs him to do so and pays invoices when Roy tells him to. Roy is the sole

cheque signatory.

Paula maintains the accounting records on a PC located in the general office. The PC

is regularly backed up and copies retained in a drawer under the desk on which the

PC stands.

Required

Identify, from the situation outlined above, circumstances that should be taken into

account when planning the audit. Explain why these matters should be taken into

account.

Paper P7 INT: Advanced audit and assurance

386 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

18 PJ’s Powertools

PJ’s Powertools is a company which assembles a range of power tools from bought-

in components.

Required

(a) For each of the following issues state the enquiries you would make and the

procedures you would perform in order to reach a conclusion as to whether

the items are fairly stated in the financial statements.

(1) A provision against warranty claims.

(2) The annual depreciation charge on a compressed air system purchased

by the company during the year for its assembly department.

(b) Explain why the audit of provisions is a difficult area for the auditor.

19 Ready Removals

Ready Removals is a removals company. In the year ended 31

st

March 20X7 the

company made a trading profit of $80,000. You are the manager in charge of the

audit. The following issues have arisen:

(1) A customer is suing the company for $100,000 for damage caused to antique

furniture. The company is defending the claim and believes that the furniture

was reproduction as opposed to antique and therefore worth only $10,000.

(2) A balance due from Speedy Storage in respect of sub-contract work, of

$30,000, has been outstanding for over six months. Your firm has been asked

by Ready Removals’ accountant not to write to Speedy Storage for direct

confirmation of this amount as the latter company objects to such letters. You

have been assured by the accountant that the relationship between the two

companies is good and that the outstanding balance will be paid.

(3) Ready Removals has recently invested in four new removal vans and is

currently carrying out extensive refurbishment of its premises. As a result of

this expenditure the company has reached its overdraft limit of $50,000.

Required

For each of the above issues:

(a) state, with reasons, the audit work that you would expect to find in

undertaking your review of the audit working papers for the year ended 31

st

March 20X7

(b) draft the relevant sections dealing with these issues of the management

representation letter you would wish the directors to sign.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 387

20 Fine Feathers

Fine Feathers retails women’s clothes through a chain of over 30 stores. Each of

these stores is located in prime city-centre sites. The company is growing rapidly.

You are the audit manager in the firm that has recently been appointed as auditor to

Fine Feathers. The audit partner has asked you to review a number of the

company’s accounting policies and practices. These are set out below.

(1) The majority of the company’s sites are acquired on short leases (typically 10

to 25 years), with rent reviews usually every five years. A premium is usually

paid to secure the lease, although this is normally associated with a period of

reduced rent. Such premiums are capitalised and amortised over the life of the

lease on a straight line basis.

(2) Before a new site can be opened for business it undergoes extensive

refurbishment. During the refurbishment period, costs incurred (including

rates and services as well as contractors’ fees) are debited to a holding

account. On completion of the refurbishment, the costs are transferred to short

leaseholds.

(3) Fine Feathers is very aware of the importance of image in the retail fashion

industry. Following a survey by independent consultants, all the existing

shops are to be restyled to project a new image. These costs will be capitalised.

Required

(a) Identify and comment on the accounting and auditing issues raised by the

above.

(b) List the further information that you require in order to be able to form an

opinion on the above practices.

21 Marvellous Manufacturing

You are the manager in charge of the audit of Marvellous Manufacturing. Your

subsequent events review for the year ended 31 March 20X7 has identified the

following events, all of which took place after the reporting period:

(1) A third of the sales force was made redundant. Provision has been made in

the financial statements for the year ended 31 March 20X7 for redundancy

payments of $500,000.

(2) One of Marvellous Manufacturing’s largest customers, Rafters Retail, notified

its intention to go into liquidation with an outstanding debt of $250,000. The

directors consider that the current general provision for bad debts will cover

any potential loss.

(3) A writ has been issued against the company by a former sales director who is

claiming $120,000 for breach of his service agreement following his dismissal

during the year ended 31 March 20X7. No provision has been made in the

financial statements for the year ended 31 March 20X7 in respect of this claim.

(4) A fire at the company’s warehouse destroyed its entire inventory. The

inventories had a book value of $2 million. This loss has not been included in

the financial statements for the year ended 31 March 20X7.

Paper P7 INT: Advanced audit and assurance

388 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Required

State the enquiries you would make and the evidence you would seek in order to

reach a conclusion on the accounting treatment of the above in the financial

statements for the year ended 31 March 20X7.

22 Wally’s Wines

You are the audit manager in charge of the audit of Wally’s Wines, a company

which imports and distributes wine. In recent years the company has become less

profitable due to the large range of wines now carried by supermarkets. The draft

financial statements for the year ended 31 March 20X7 show that current liabilities

exceed current assets by $200,000.

The company’s major source of finance is a bank loan of $500,000 which is due for

repayment in full on 31 October this year. The company is currently negotiating

with its bankers for a replacement long-term loan of $1 million. They intend to use

some of the loan to reposition themselves in the marketplace to establish the

superiority of their wines over those sold in supermarkets.

The directors submitted a profit forecast with their loan application and are

optimistic that their application will be successful. However, they do not expect

negotiations to be completed before the annual general meeting in September. Your

firm has been asked not to approach the bank directly.

Required

(a) Set out the audit procedures you would perform in order to establish the

status of Wally’s Wines as a going concern.

(b) Discuss the alternative audit opinions that might be relevant to the financial

statements of Wally’s Wines together with the circumstances in which each

would be appropriate.

23 The Pepper Group

The Pepper Group is an international business, made up of ten subsidiaries and a

head office. You are the manager in charge at the firm undertaking the group audit,

but there are separate local auditors for the Cayenne subsidiary in the United States,

the Habenaro subsidiary in Mexico and the Hybrid subsidiary in Columbia. You are

aware of the following information:

(1) Hybrid is a loss-making subsidiary, with losses at the current year end

totalling $2.7 million. There are significant control problems, high levels of

bad debts and 25% staff turnover. The local auditors have already stated their

intention to give a qualified opinion for the year just ended because of the

material issues found.

(2) Cayenne is operating to a different financial year to that of the group as a

whole, being October 20X1 rather than December 20X1.

(3) Shortly after the year end, in January 20X2, the Pepper Group announced the

sale of Habenaro for $25 million and this disposal is currently underway.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 389

(4) The Pepper Group is guaranteeing loans of approximately $10 million for its

subsidiaries.

Required

(a) Set out how you would plan and control the group audit of the Pepper Group.

(b) Consider the impact of each of the above issues on the group audit.

(c) Explain the nature of the relationship between your firm and the auditors of

the subsidiaries, making particular reference to the extent to which your firm

may rely on the component auditors’ work and to the considerations involved

where joint audits are conducted.

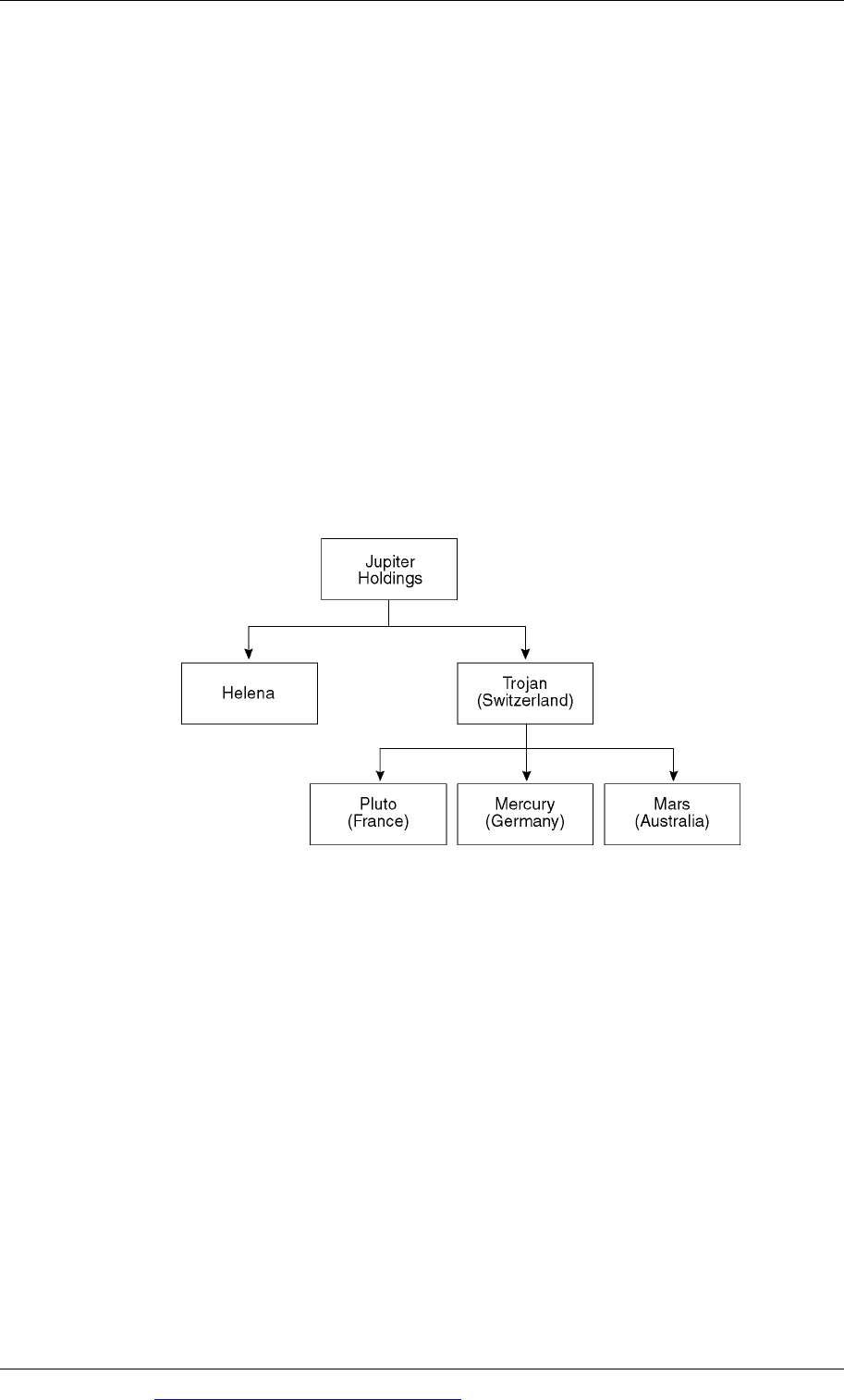

24 Jupiter Holdings

The following diagram shows the structure of the Jupiter Holdings group, a listed

company with subsidiaries both locally and overseas. All subsidiaries are wholly-

owned. All of Jupiter Holdings’ overseas operations are run via Trojan.

During the year ended 31 December 20X4 the board of Jupiter Holdings decided to

restructure the group and the following events took place:

(1) Mars was sold on 1 August 20X4 to an Australian competitor, Venus. The

consideration was in the form of shares in Venus, such that Trojan now owns

30% of Venus.

(2) Pluto was sold on 30 November 20X4 to Helena. The consideration was $1

million settled in cash.

(3) To stimulate the operations of Helena and Pluto, 26% of the Helena group was

sold to Interesting Investments on 1 December 20X4.

You are the audit manager on the Jupiter Holdings audit. In addition to the main

group financial statements, Helena is also required by Interesting Investments to

prepare group financial statements. Your office audits the Jupiter Holdings group,

Helena and Pluto. Your Swiss associate audits Trojan. Mercury (which is not

material to the group) is not audited, and Venus and Mars are audited by a small

Paper P7 INT: Advanced audit and assurance

390 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Australian practice. With the exception of Mercury, all members of the group are

material.

Required

Prepare notes for a planning meeting with the engagement partner setting out the

significant matters which need to be considered at this stage in respect of:

(a) the Helena audit

(b) the Jupiter Holdings audit.

25 Audit-related services

Explain the key characteristics of the following audit-related services:

(a) A review engagement

(b) Agreed-upon procedures

(c) A compilation engagement

26 Assurance work

‘The growth in assurance-type work provides a great money spinning opportunity

for audit firms to provide a lower level of assurance, involving less work and

reduced engagement risks, compared to the standard audit.’

Required

Discuss this statement.

27 Elleander Designs

You are one of three audit managers working for a medium-sized firm of

accountants which has just taken on the audit of Elleander Designs. Elleander

Designs retails designer clothes through its two shops located in busy towns 30

kilometres apart.

The clothes sold are very exclusive. They are designed by the company’s owner,

Mrs Catur, who is also the managing director. 50% of the company’s clothes are

made to order, with the remainder being produced as inventory for the two shops.

Each hand made piece can take up to three months from commencement of design

to finishing and can sell for up to $10,000.

Mrs Catur splits her time equally between the two shops. She employs two shop

managers, two assistants, and other staff who make up her designs in workrooms

above each shop. There are two other directors: Mr Catur, her husband, the finance

director, and Ms Craft, her sister, who is the marketing director.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 391

The following is an extract from the financial statements:

Year ended 30 September

20X2 (draft)

Year ended 30 September

20X1 (actual)

Non-current assets

Intangible

(goodwill)

Property, plant and

equipment

$

67,500

40,000

$

75,000

45,000

Current assets

Inventories

Finished goods

Work in progress

150,000

45,000

210,000

75,000

Note to the draft accounts

There is a legal claim pending. However, the directors consider that it is so

unlikely to succeed that no provision has been made for it in the financial

statements.

The goodwill figure arose when Elleander Designs, which was originally a

partnership, incorporated to become a limited company in July 20X1.

Required

(a) State the evidence you would require from Elleander Designs in order to

verify the year end inventories figures and justify your answer.

(b) Briefly describe what audit work you would perform to verify the figure for

goodwill in the financial statements.

(c) Explain what is meant by an ‘accounting estimate’ and describe what work

you would perform to verify whether or not the figure for the legal claim

pending should be included in the financial statements.

(d) Elleander Designs has approached its bank to discuss raising finance for a new

exciting 12 month partnership venture with a major clothes designer. The

bank has asked for a five year forecast to be examined and reported on by an

accountant. Briefly describe what work you would carry out in connection

with the forecast, including the contents of your firm’s report.

28 Cranford Communications

Cranford Communications operates via a head office and several branches. The

company has a mainframe computer at its head office, which is linked via a

communications network to terminals at its branches.

You are a manager at a firm which has been asked to carry out a systems reliability

review over the general controls operating in Cranford Communications’ computer

system. Your initial work has identified the following weaknesses:

(1) There is no physical restriction at every site to the rooms in which the

terminals are kept.

Paper P7 INT: Advanced audit and assurance

392 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(2) Staff can change passwords at their discretion.

(3) In the computer room at the head office there are no fire extinguishers or air

conditioning.

(4) There is no formal disaster recover plan.

(5) Back up media is held on site.

Required

Identify the possible consequences of the above weaknesses and suggest

recommendations to remedy them, clearly describing how the control procedures

should operate.

29 Internal and external audit

(a) Explain the difference between the internal and external audit functions.

(b) List the advantages and disadvantages of a company outsourcing its internal

audit function to its external auditors.

30 Holiday Snacks

You are the audit manager in charge of the audit of Holiday Snacks, a company

which runs a chain of snack bars operating in a number of seaside holiday resorts.

Your firm has been the auditor for a number of years and has always had to

substantively test cash sales because of a lack of control over the recording of

takings. The audit reports to date have been unmodified.

You have recently been informed that the company has taken on a newly qualified

certified accountant as chief internal auditor and an unqualified assistant internal

auditor. Since their appointment half way through the year ended 31

st

December

20X5 the two have spent most of their time carrying out substantive tests on cash

sales.

The directors are hopeful that your audit fee this year will decrease because you will

be able to rely on the work carried out by the internal auditors.

Required

Explain the issues that will be relevant to your firm in deciding:

(a) whether you can rely on the work performed by the internal auditors

(b) how much reliance to place on that work.

31 Aaron Automotives and Bling Bonnets

You are the manager responsible for the audit of two, unrelated, audit clients. In

each case you are currently reviewing the audit working papers and the audit

seniors’ recommendations for the type of audit report to be issued. Details are as

follows:

(1) Aaron Automotives is a subsidiary of Verity Vehicles. Serious going concern

problems have been noted during this year’s audit. Aaron Automotives will

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 393

be unable to trade for the foreseeable future unless it continues to receive

financial support from Verity Vehicles. A letter of support has been received

and a copy is filed on the current audit file.

The audit senior has suggested that, due to the seriousness of the situation, the

audit opinion should be modified.

(2) During the year, Bling Bonnets has made a small loan to one of its directors

but this has not been disclosed in the financial statements. Such disclosure is

required by local legislation. Your audit report gives an opinion on

compliance with such legislation.

The audit senior has suggested that, as the amount involved is small, an

unmodified opinion should be issued.

Required

For each client, comment on the suitability or otherwise of the seniors’ proposals for

the audit reports. Where you disagree, indicate what kind of modification (if any)

should be given instead.

32 Gorgeous Goods and Conrads Contracts

Described below are situations which have arisen in two unrelated audits and

which are considered material.

(1) Gorgeous Goods

Although you are satisfied that closing inventories this year are fairly stated, the

audit report on the previous year’s financial statements was modified due to a

restriction on the scope of the audit work in respect of the closing inventory figure.

This led to a qualified opinion.

(2) Conrads Contracts

The financial statements disclose the fact that a provision may be required to reduce

inventories to their net realisable value if a contract with a major customer,

representing 60% of the company’s revenue, is not renewed. A decision on this by

the customer is not expected until after the accounts are due to be signed.

Required

(a) State what is meant by, and explain the relationship between, the concepts of

materiality and true and fair.

(b) State, with reasons, the effect on the audit reports of the situations described

above.

33 Polar Publishing

You are the manager in charge of the audit of Polar Publishing which publishes a

number of specialist monthly magazines. Most readers take out an annual subscription,

which can commence in any month of the year. The company’s revenue is made up of

40% from sales of magazines and 60% from advertising revenue.

Paper P7 INT: Advanced audit and assurance

394 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

On review of the audit working papers, you have come across the following file

note points:

(1) Details of readers and their subscription renewal dates are stored on the

computerised database. The client has allowed routine database maintenance

work to slip badly behind schedule. At the final audit there is a backlog of

new subscriptions and notification of cancelled subscriptions and changes of

addresses which have not been input onto the database.

(2) The advertising manager has been under considerable pressure due to staff

shortages in the advertising department. In order to sell sufficient advertising

space he has been offering a variety of special deals to advertisers. The

negotiations all take place over the phone and the manager keeps notes of the

conversations in his desk drawer. Towards the year end, the manager was so

busy that he had no time to send out the usual confirmation letters. The

confirmation letters are used as the basis for allocating advertising space.

Required

Set out, in a manner suitable for inclusion in a report to management, the

weaknesses arising from the above, the consequences of those weaknesses and

recommendations for improvement.

34 Non-audit services

The current practice of many audit firms offering substantial non-audit services to

their audit clients compromises the integrity of the auditing profession and is not in

the interests of management.

Required

Discuss the above, indicating whether factors such as client size and listed status

would make any difference to your opinion.

35 Auditor’s liability

Increasingly, the auditing profession is finding itself on the receiving end of large

negligence suits.

Required

Discuss what measures could be taken within individual firms, by the profession as

a whole, or by governments to reduce the size or incidence of such claims.

36 The audit of small businesses

There is a view held by some, that small businesses are unauditable by their very

nature. However, others would say that because the auditor of a small business is

much more closely involved with his client, his knowledge of that client is extensive

and he is therefore better placed to audit it, whereas larger audits are much more

mechanical.

Required

Discuss.