ACCA P4 Advanced Financial Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 3: Capital investment appraisal

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 65

Example

Using the same example as for the payback period calculation, and assuming a cost

of capital of 10%, the discounted payback period is calculated as follows:

Year

Annual cash

flow

Discount

factor at 10%

PV of cash

flow

Cumulative

NPV

$ $ $

0 (200,000) 1.000

(200,000)

(200,000)

1 (40,000) 0.909

(36,360)

(236,360)

2 30,000 0.826

24,780

(211,580)

3 120,000 0.751

90,120

(121,460)

4 150,000 0.683

102,450

(19,010)

5 100,000 0.621

62,100

43,090

6 50,000 0.564

28,200

71,290

NPV

+ 71,290

The discounted payback period is Year 5, and we can estimate it in years and

months as:

4 years + (19,010/62,100) × 12 months

= 4 years 4 months.

The discounted period for a capital investment is always longer than the ‘ordinary’

non-discounted payback period.

One criticism of the discounted payback method of project evaluation is the same as

for the non-discounted payback method. It ignores the expected cash flows from the

project after the payback period has been reached.

One measure of time to recover an investment that recognises the values of the cash

flows over the entire life of the project is duration.

2.3 The concept of duration

Duration can be defined as the time to recover one half of the project value.

The concept of duration is widely used by analysts in the bond markets. It is a

measure of how long an investor in bonds must wait before his investment in the

bond is recovered.

Duration of bonds

For example, suppose that there are two bonds X and Y, each with a maturity of

four years. The returns for the investor on the bonds will be as follows:

Year Year Year Year Total return

$ $ $ $ $

Bond X 10 10 10 110 140

Bond Y 20 20 20 120 180

For the investor, investing in a bond would be a four-year capital investment.

Paper P4: Advanced Financial Management

66 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

If the investor is interested in how long he must wait to recover his investment, we

could calculate the average time that this will take. Average time can be calculated

as the weighted average number of years that this will take.

To calculate a weighted average period for obtaining the investment returns, the

cash flows in each year should be given a weighting. For an investment with n

years, the weighting for Year 1 should be 1, for Year 2 it should be 2 and for year 3 it

should be 3, and so on. The weighting for the cash flow in Year n is n.

With four-year bonds, the weighting for the return in Year 1 is therefore 4, and so

on.

Bond X Bond Y

Year Return R Weighting W R × W Return R Weighting

W

R × W

1 10 1

10

20

1 20

2 10 2

20

20

2 40

3 10 3

30

20

3 60

4 110 4

440

120

4 480

140

500

180

600

The non-discounted average time to recover the investment is:

For Bond X, 500/140 = 3.57 years

For bond Y, 600/180 = 3.33 years.

Calculating the duration of a bond

The average times calculated above are similar to the calculation of a non-

discounted payback period. The calculation fails to recognise the time value of

money by discounting the returns in each year before weighting them.

A value for the duration of a bond, known as Macaulay’s duration, is calculated

using the present value of the returns in each year.

In the previous example of the two bonds, suppose that the investor’s cost of capital

is 10%. The value for Macaulay’s duration of each bond is calculated as follows:

Bond X

Year Return R Discount factor

at 10%

PV of return Weighting PV × W

1 10 0.909

9.09

1

9.09

2 10 0.826

8.26

2

16.52

3 10 0.751

7.51

3

22.53

4 110 0.683

75.13

4

300.52

99.99

348.66

Duration of Bond X = 348.66/99.99 = 3.49 years.

Bond Y

Year Return R Discount factor

at 10%

PV of return Weighting PV × W

1 20 0.909

18.18

1

18.18

2 20 0.826

16.52

2

33.04

3 20 0.751

15.02

3

45.06

4 120 0.683

81.96

4

327.84

131.68

424.12

Duration of Bond Y = 424.12/131.68 = 3.22 years.

Chapter 3: Capital investment appraisal

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 67

The significance of bond duration

The duration of a bond is an indication of the price sensitivity of the bond to a

change in market yields on bonds. When there is a rise in interest rate, the fall in

price of a bond (as a percentage) is greater for bonds with a higher/longer duration.

The actual amount by which bonds will change in price following a change in

market interest rates can also be calculated.

Investors in bonds can therefore manage the risk in their bond portfolio by selecting

bonds with a suitable duration.

2.4 Capital investment projects and duration

Duration can be calculated for a capital investment project in exactly the same way

as for a bond. It is a measure of the average time to obtain the returns from the

investment. Another way of saying this is that the duration of a project is the time

required to cover one half of the value of the investment returns.

Duration can be used in capital investment appraisal to assess the payback on a

project. Unlike payback and discounted payback, however, it takes into

consideration the total expected returns from the entire project (at their discounted

value), not just the returns up to the payback time.

If the duration of a project is short relative to the life of the project – for example,

if the duration is less than half the expected total life of the project – this means

that most of the returns from the project will be recovered in the early years.

If the duration of a project is a large proportion of the total life of the project – for

example if the duration is 75% or more of the total life of the project – this means

that most of the returns from the project will be recovered in the later years.

It could therefore be argued that duration is the best available method of assessing

the time for an investment to provide its return on the capital invested.

Example

The same example that was used earlier for the payback period calculation and

discounted payback period can be used to calculate the duration of a project. The

cash flows and present values are as follows:

Year

Annual cash

flow

Discount

facotr at 10%

PV of cash

flow

$ $

0 (200,000) 1.000

(200,000)

1 (40,000) 0.909

(36,360)

2 30,000 0.826

24,780

3 120,000 0.751

90,120

4 150,000 0.683

102,450

5 100,000 0.621

62,100

6 50,000 0.564

28,200

NPV

+ 71,290

Paper P4: Advanced Financial Management

68 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

To calculate duration for a project, the negative cash flows at the beginning of the

project are ignored. Duration is calculated using cash flows from the year that the

cash flows start to turn positive.

However, if there are negative cash flows in any year after the cash flows turn

positive, such as in the final year of the project, these negative cash flows are

included in the calculation of duration (as negative values).

In this example, the cash flows start to turn positive from Year 2, so duration is

calculated using the present values of the cash flows from Year 2 to Year 6. The Year

2 cash flow is given a weighting of 2, the Year 3 cash flow a weighting of 3, and so

on.

Duration is therefore calculated as follows:

Year

Annual cash

flow

Discount

factor at 10%

PV of cash

flow

Weighting PV ×

Weighting

$ $

2 30,000 0.826

24,780

2

49,560

3 120,000 0.751

90,120

3

270,360

4 150,000 0.683

102,450

4

409,800

5 100,000 0.621

62,100

5

310,500

6 50,000 0.564

28,200

6

169,200

307,650

1,209,420

The duration of the project is 1,209,420/307,650 = 3.93 years.

Chapter 3: Capital investment appraisal

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 69

DCF: internal rate of return (IRR) and modified internal rate of return

(MIRR)

The investment decision rule with IRR

Calculating a project IRR

NPV, IRR and financial management

Modified internal rate of return (MIRR)

3 DCF: Internal rate of return (IRR) and modified rate of

return (MIRR)

The internal rate of return (IRR) of a project is the discounted rate of return on the

investment.

It is the average annual investment return from the project.

Discounted at a cost of capital equal to the IRR, the NPV of the project cash flows

must come to 0.

3.1 The investment decision rule with IRR

An organisation might establish the minimum rate of return that it wants to earn on

an investment. If other factors such as non-financial considerations and risk and

uncertainty are ignored, the investment decision using IRR should be based on the

following rule:

If a project IRR is equal to or higher than the minimum acceptable rate of return,

it should be undertaken.

It the IRR is lower than the minimum required return, it should be rejected.

Since NPV and IRR are both methods of DCF analysis, the same investment decision

should normally be reached using either method.

3.2 Calculating a project IRR

The IRR of an investment can be calculated by inputting the project cash flows into a

financial calculator. An

approximate IRR can be calculated using interpolation.

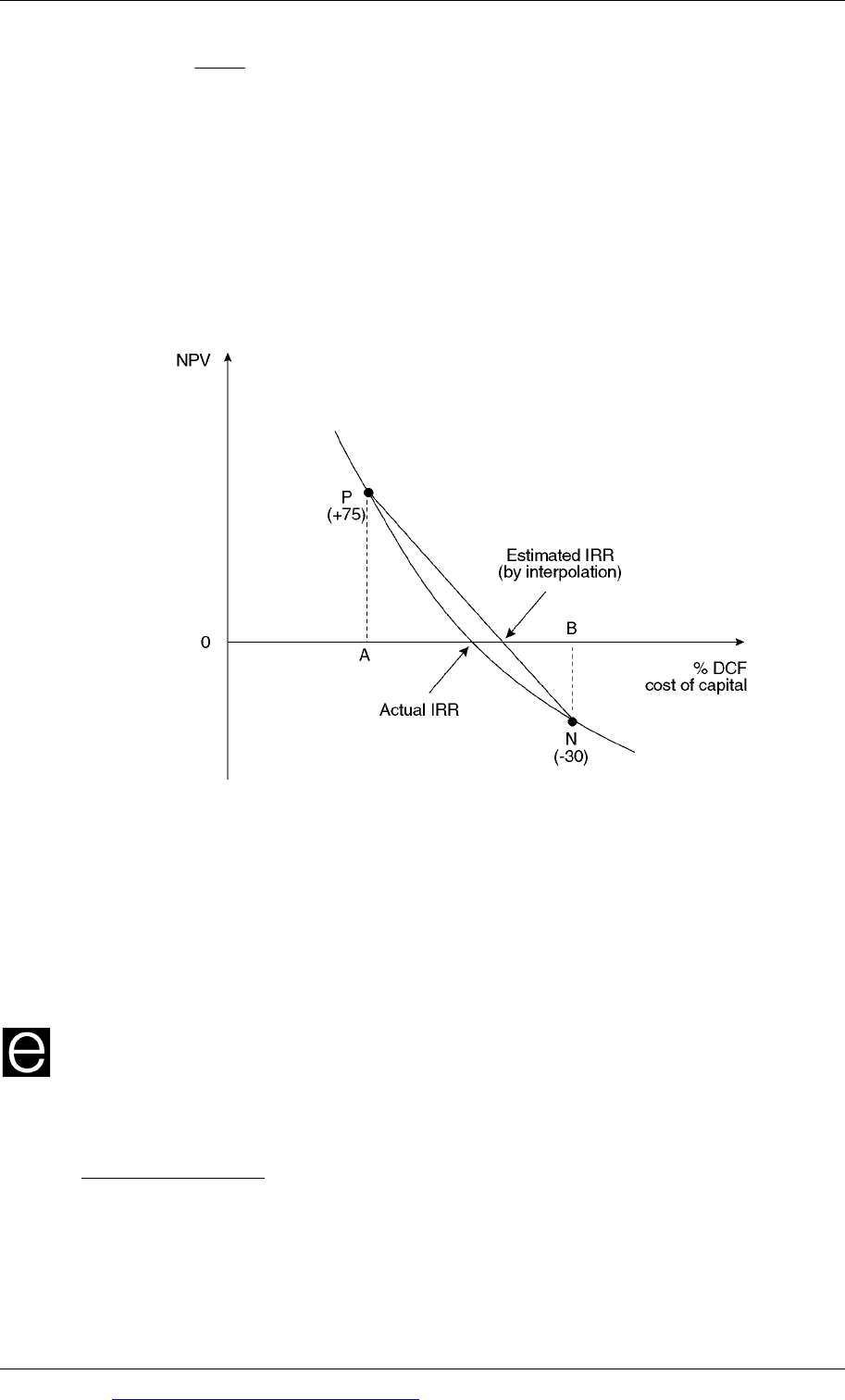

Calculating IRR by interpolation

To calculate the approximate IRR by interpolation, you must have the NPV for the

project at two different discount rates (cost of capital). Ideally, one NPV should be

positive and the other NPV should be negative.

If the NPV at A% is positive, + $P, and if the NPV at a higher cost of capital B% is

negative, - $N, then:

Paper P4: Advanced Financial Management

70 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

IRR = A%+

P

P + N

× B − A

()

%

⎡

⎣

⎢

⎤

⎦

⎥

Ignore the minus sign for the negative NPV. For example, if P = + 75 and N = - 30,

then P + N = 105.

To calculate the approximate IRR by interpolation, you must have the NPV for the

project at two different discount rates (cost of capital). Ideally, one NPV should be

positive and the other NPV should be negative.

The interpolation method is only approximate and is not exact. This is because it

assumes that the IRR decreases at a constant rate between the two NPVs.

For a ‘typical’ project, the IRR estimated by the interpolation method is slightly

higher than the actual IRR. The interpolation method gives a more accurate estimate

of the IRR when:

both NPVs in the calculation are close to 0, and

the NPV at A% is positive and the NPV at B% is negative.

Example

A business requires a minimum expected rate of return of 12% on its investments. A

proposed capital investment has the following expected cash flows:

Year

$

0 (80,000)

1 20,000

2 36,000

3 30,000

4 17,000

Chapter 3: Capital investment appraisal

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 71

Required

Calculate the NPV at a cost of capital of 10% and a cost of capital of 15%. Use these

NPV figures to estimate the IRR.

Answer

Year

Cash flow

Discount factor

at 10%

Present value

at 10%

Discount

factor at 15%

Present value

at 15%

0 (80,000) 1.000 (80,000) 1.000 (80,000)

1 20,000 0.909

18,180

0.870 17,400

2 36,000 0.826

29,736

0.756 27,216

3 30,000 0.751

22,530

0.658 19,740

4 17,000 0.683

11,611

0.572 9,724

NPV

+ 2,057

(5,920)

The IRR is above 10% but below 15%.

Using the interpolation method:

The NPV is + 2,057 at 10%.

The NPV is – 5,920 at 15%.

The NPV falls by 7,977 (2,057 + 5,920) between 10% and 15%.

The estimated IRR is:

IRR =10%+

2,057

2,057 + 5, 920

()

× 15 −10

()

%

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

= 10% + 1.3%

= 11.3%

Recommendation

The project is expected to earn a DCF return below the target rate of 12%, and on

financial grounds it is not a worthwhile investment.

3.3 NPV, IRR and financial management

In strategic financial management, the NPV method of investment appraisal is more

important than the IRR method. This is because the value of an investment or a

financial instrument is the present value of the expected future cash flows that it

will produce, discounted at a suitable cost of capital.

The expected NPV of a new investment by a company could possibly be taken as an

estimate of the change that should result in the total value of the company, if the

investment is undertaken, provided that investors are aware of the project and its

expected NPV.

However, although the NPV method is used much more often, the IRR method

might sometimes be used for project appraisal.

Paper P4: Advanced Financial Management

72 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

3.4 Modified internal rate of return (MIRR)

A criticism of the IRR method is that in calculating the IRR, an assumption is that all

cash flows earned by the project can be reinvested to earn a return equal to the IRR.

For example, suppose that a project has an NPV of + $300,000 when discounted at

the cost of capital of 8%, and the IRR of the project is 14%. In calculating the IRR, an

assumption would be that all cash flows from the project will be reinvested as soon

as they are received to earn a return of 14% - even though the company’s cost of

capital is only 8%.

Modified internal rate of return is a calculation of the return from a project, as a

percentage yield, where it is assumed that cash flows earned from a project will be

reinvested to earn a return equal to the company’s cost of capital. So in the previous

example of the project with an NPV of $300,000 at a cost of capital of 8%, MIRR

would be calculated using the assumption that project cash flows are reinvested

when they are received to earn a return of 8% per year.

Using MIRR for project appraisal

It might be argued that if a company wishes to use the discounted return on

investment as a method of capital investment appraisal, it should use MIRR rather

than IRR, because MIRR is more realistic because it is based on the cost of capital as

the reinvestment rate.

Calculating MIRR

The MIRR of a project is calculated as follows:

Step 1. Take the negative net cash flows in the early years of the project, and

discount these to a present value. The total PV of these cash flows is the PV of

the investment phase of the project. If the only year of negative cash flow is Year

0, the PV of the investment phase is the cash flow in Year 0. However, if there

are negative cash flows in Year 1, or Year 1 and 2, discount these to a present

value and add them to the Year 0 cash outflow.

Step 2. Take the cash flows from the year that the project cash flows start to turn

positive and compound these to an end-of-project terminal value, assuming that

cash flows are reinvested at the cost of capital. For example, if cash flows are

positive from Year 1 of a five-year project:

-

compound the cash flow in Year 1 to and end-of-year 5 value using the

cost of capital as the compound rate

-

compound the cash flow in Year 2 to and end-of-year 5 value using the

cost of capital as the compound rate

-

compound the cash flow in Year 3 to and end-of-year 5 value using the

cost of capital as the compound rate

-

compound the cash flow in Year 4 to and end-of-year 5 value using the

cost of capital as the compound rate

-

add the compounded values for each year to the cash flow at the end of

Year 5.

Chapter 3: Capital investment appraisal

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 73

The total of the compounded values is the total value of returns during the

‘recovery’ phase of the project, expressed as an end-of-project value.

Step 3. The MIRR is then calculated as follows:

MIRR =

1

B

A

n −

where

n = the project life in years

A = the end-of-year investment returns during the recovery phase of the project

(as calculated in Step 2)

B = the present value of the capital investment in the investment phase (as

calculated in Phase 1).

Study the following example carefully:

Example

A business requires a minimum expected rate of return of 8% on its investments. A

proposed capital investment has the following expected cash flows and NPV.

Year

Cash flow Discount

factor at 8%

Present

value

$

$

0 (60,000) 1.000 (60,000)

1 (20,000) 0.926

(18,520)

2 30,000 0.857

25,710

3 50,000 0.794

39,700

4 40,000 0.735

29,400

5 (10,000) 0.681

(6,810)

NPV

+ 9,480

The IRR of the project is about 11.5% (workings not shown).

The modified internal rate of return (MIRR) is calculated as follows:

Step 1. The PV of investment in the investment phase

Year

Cash flow Discount

factor at 8%

Present

value

$

$

0 (60,000) 1.000 (60,000)

1 (20,000) 0.926

(18,520)

(78,520)

Paper P4: Advanced Financial Management

74 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Step 2. Reinvest cash flows in the recovery phase at the cost of capital, 8%

Year

Cash flow Compound at 8%

to end of Year 5

Present

value

$

$

2 30,000 × (1.08)

3

37,791

3 50,000 × (1.08)

2

58,320

4 40,000 × (1.08)

1

43,200

5 (10,000)

(10,000)

Total

129,311

Step 3. Calculate MIRR using the formula

MIRR =

1

520,78

311,129

5 −

MIRR = 0.1049 or 10.49%, say 10.5%.

The IRR is 11.5%, but the MIRR is lower because it assumes a lower reinvestment

rate of cash inflows.