ACCA P3 Business Analysis - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 485

34 R&D strategy

Some companies must invest in R&D to survive and grow. The main financial

problems associated with R&D are likely to be as follows:

Deciding how much in total to invest in R&D each year.

Dividing the total spending between pure research, applied research and

development.

Recognising the probability of failure of many research projects and some

development projects. Returns are therefore extremely difficult to predict.

Even so, recognising the need to innovate. There is a risk that the ‘accounting

mentality’ will persuade companies to invest more in products they have

already developed, and avoid R&D.

Companies that do not spend enough on R&D will fail to innovate. They must

therefore copy new products that rival companies develop and bring to market.

However, these new products may be protected by patents.

There has to be a system for planning, monitoring and controlling spending on

R&D.

35 Rational strategic plans

The question gives a statement of the ‘rational model’ of strategic planning.

If we accept that the overall objective is to maximise the wealth of its shareholders,

there are several weaknesses with the rational model.

(a) There is a very large element of risk and uncertainty in long-term planning. At

best, management can only develop strategies that they think are likely to

increase shareholder wealth.

(b) Management is often under pressure to achieve a good performance (profits,

dividends and so on) in the short term. They may therefore prefer strategies

that provide good short-term results, without giving proper thought to the

long-term. Good short-term results are often achieved at the expense of

longer-term benefits. (For example, short-term profits can be increased by

choosing not to invest in new equipment.)

(c) Shareholders and other stakeholders often have conflicting interests, and it is

not possible to develop strategies that optimise the benefits of all groups.

(d) Management do not have perfect knowledge. The information available to

them is limited, and their ability to absorb and understand it all is also limited.

Managers therefore make strategic plans within the limits of what they know

and understand. This is the concept of ‘bounded rationality’ in strategic

planning.

(e) Managers may simply choose strategies that will provide results that are

acceptable and ‘good enough’ for shareholders and other stakeholders. This is

the concept of ‘satisficing’ (rather than ‘optimising’ to achieve the best results

possible).

Paper P3: Business analysis

486 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

36 Emergent strategy

(a) Strategy analysis is the process of assessing the strategic situation (perhaps

using techniques such as SWOT analysis) and identifying different alternative

strategies that might be chosen to pursue the entity’s objectives. The preferred

strategy is then selected.

Strategy formulation is the process of developing plans and establishing

targets for achieving the selected strategy.

Strategy implementation is putting the strategic plans into operation, and

monitoring actual progress by comparing actual achievements against the

targets.

(b) Mintzberg argued that some strategic plans might be developed and

implemented in this rational way. These are deliberate strategies.

More usually, planned strategies often do not go according to plan, because

unexpected developments occur that alter the situation. As a result, some of

the planned strategies might be abandoned, and new strategies selected in

response to the new circumstances. A strategy adopted in order to take

advantage of an unexpected opportunity is an emergent strategy. Mintzberg

argued that the strategies of entities are a combination of deliberate and

emergent strategies.

37 Stage in development

The situation can be analysed using Greiner’s growth model.

The company appears to have reached a ‘crisis of red tape’, and the way forward in

its development is ‘growth through collaboration’ between head office and

investment centre management. The collaboration should be based on team-work

and problem-solving, to replace the old systems of control through reporting and

accounting.

38 Business processes

(a) The Harmon process-strategy matrix is as follows:

Strategic importance

Low

High

Low

High

Process complexity

and dynamism

Simple, stable,

routine, ordinary

processes.

Should be capable of

high degrees of

automation

Simple, stable, but

valuable processes.

Should be capable of

high degrees of

automation to gain

efficiency

Complex, dynamic,

ordinary processes.

Might be better to

outsource

Complex, dynamic,

valuable processes.

Business process

redesign and

improvement

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 487

It is likely that the expense claim process would be in the bottom left-hand

quadrant: simple, stable, routine and not of great strategic importance.

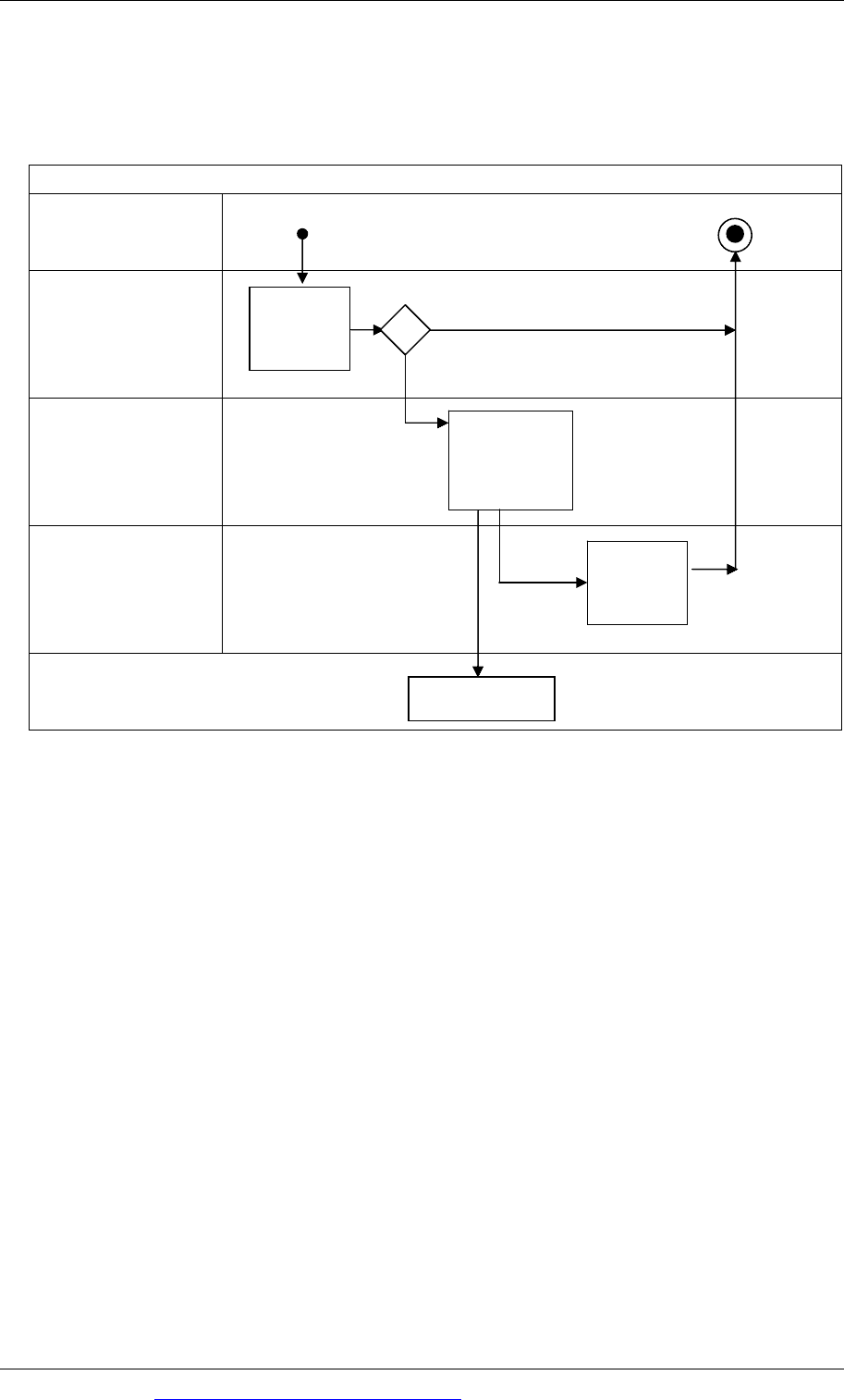

(b)

Expense claim process

Employee

Manager

Accounting

Cashier

Bank

39 Features of organisational change

Huczynski and Buchanan identified four basic features of organisational change,

that management should recognise

Triggers of change. These are developments, internal or external to the entity,

that point to the need for change. An entity should have surveillance or scanning

mechanisms in place to identify these triggers when they arise.

Interdependencies. Changes in one part of an organisation or in some aspect of

an organisation’s structure or operations will inevitably have a knock-on effect.

Other people within the organisation, and other processes and operations will

also be affected. (This is similar to the concepts in the McKinsey 7S model.)

Conflicts and frustrations. Change brings conflict and frustrations. Some want the

change to happen, and others resist it. People wanting change become frustrated at

the lack of change, or slow progress towards change. This leads to conflict.

Time lags. There are time lags in the change process. Planned changes rarely go

according to plan or according to the planned timetable. People accept change at

different rates, and systems and processes might change at different rates too.

Change can therefore be messy.

Expense

claim

approval

Details

posted,

payment

re

q

uested

Payment

notification

Initiating event

End of the process

Approved

Not approved

Bank transfer

Paper P3: Business analysis

488 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

40 Change

(a) BPR is an approach to introducing a transformational change within an

organisation. An entire business process is re-designed and re-organised (‘re-

engineered’). BPR usually involves reorganising work around a system,

instead of organising work by departmental functions. As a result, processes

are operated by multi-disciplinary teams.

(b) A suitable model might be the Lewin’s three-step change model, supported by

Lewin’s force field analysis.

(i) The three-step change process is unfreeze, move (change) and re-freeze.

The ‘unfreeze’ step is to develop a recognition amongst the people

affected that change is needed and is desirable, and obtaining agreement

about the nature of the changes that are required. The ‘move’ step is

making the change. Once a change has been made, there is a risk that

employees will go back into their former habits and ways of doing

things: ‘re-freeze’ means taking measures to ensure that the change

becomes established and the new ‘accepted way of doing things’.

(ii) Force field analysis can be used to assess the strength of resistance to

change, and the nature of the forces driving change. Lewin

recommended that the most effective approach t gaining acceptance of

change is to find ways of reducing the forces of resistance to change.

(c) Internal marketing involves establishing the views and opinions of people

inside the organisation and trying to ‘market’ an idea to them – for example,

trying to persuade them of the need for change. In the context of change

management, internal marketing means finding out the views of employees

towards a proposed change and trying to promote the change as ‘a good

thing’. In external marketing, the customer is the main consideration. In

internal marketing, the employee is the ‘customer’ whose views and opinions

must be taken into consideration: plans for change should be amended where

appropriate, in response to the views of employees.

41 Channel for marketing and distribution

For suppliers

A marketing and sales channel available to users 24 hours a day, 7 days a week.

Products can be sold to customers anywhere in the world, provided that there is

a reliable distribution channel.

Ability to respond immediately to customer requests.

Customers can access up-to-date information about products on the supplier’s

web site.

Direct mailing by e-mail is cheaper and more efficient that direct mail marketing

by post.

It is cheaper to operate an on-line marketing and sales operation than to open a

retail outlet.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 489

Electronic products can be delivered immediately to customers anywhere in the

world.

Can be linked easily to a system for recording management information about sales.

For customers

A convenient 24/7 method of shopping.

Easy access to a large number of potential suppliers

Ability to shop around for the best deal (for example, the lowest price)

Fast service

Convenience of immediate delivery for electronic products

42 Stefan Lund

(a)

Selling through the supermarket group

Advantages Disadvantages

Access to a large number of potential

customers

Potential for large sales volumes

The supermarket will probably sell the hats

as a fairly narrow product range of; therefore

less design requirements

Probably easily-managed distribution

arrangements

Possibly large sales volumes: this could act

as a drain on cash in the early stages of the

business.

Single customer: risk of losing the customer

if sales are disappointing or there are

problems with supply.

Stefan cannot use his own brand for the

products.

There may be pressure from the

supermarket group to reduce prices.

Sales prices for Stefan will be lower than the

prices charged by the supermarkets.

Selling through independent fashion shops

Advantages Disadvantages

Shops specialise in selling fashion goods.

Access to customers looking to buy fashion

goods.

Stefan can use his own brand for the

products.

Shops will probably want to sell products at

high prices, therefore potential for high gross

profit margins

Possibly low sales volumes

Shops will probably want a wide range of

differentiated products.

Need for high quality

Possibly higher costs of distribution (to the

shops)

Using some of the shops might be

unprofitable.

Sales prices for Stefan will be much lower

than the retail prices charged by the shops.

Selling through web site and Internet

Advantages Disadvantages

Products can be made to order.

Product quality may not be such an

important issue.

Stefan can use his own brand for the

products.

Ability to be flexible with design: new designs

can be varied to meet customer preferences.

Direct contact with users of the product

Higher prices and gross profit margins

Problem of attracting potential customers to

the web site.

Distribution will be more expensive and time-

consuming: products must be delivered to

customer addresses

Order-handling will be more complex due to

the larger volume of small orders to handle.

Paper P3: Business analysis

490 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(b)

Supermarkets Fashion shops Internet

Product Small product range

Large volumes

Quality important

Wide product range

Small volumes

Quality important

Wide product range

Volume difficult to predict

Quality probably less

important

Place Supermarkets Specialist shops Internet, web site, e-

commerce

Price Pricing probably critical:

low prices

Prices to the customer

will be high

Prices probably neither

high nor low.

Promotion Through the

supermarket’s own

brand

Need for brand

development

Need for brand

development.

Success of web site in

attracting ‘hits’ will be

critically important

43 Travel goods firm

Tutorial note: A suggested answer is given here. Your answer may differ in some

details.

Strengths

Strong brand and reputation

Worldwide facilities for manufacture and distribution

Managers with ideas for improving the business

Successful experience with EDI

Successful experience with web site and e-commerce.

Weaknesses

Poor communications between divisions within the company

Little or no access to information about competitors

Possibly the decentralisation of IS/IT systems is a weakness.

Opportunities

Possible use of intranet to improve internal communications and interchange of

ideas

Possible use of extranets to improve communications with customers

Possible use of an executive information system to provide more information

about competitors and the market.

Threats

Strong competition in the market. Competitors have made some successful

initiatives.

Significant fall in number of ‘hits’ on the web site.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 491

44 Electronic marketing

(a) To provide information about theatres on their web site. Theatres may have

linked web sites, or a joint web site for theatres in the same commercial group.

The information will relate partly to the theatres themselves (and their

location) but will provide details of what is on.

(b) To allow customers to buy tickets on line, choosing the date and time of the

performance, reserving the seats and paying for the tickets.

(c) To monitor traffic (‘hits’ at each web site) and so assess customer interest.

(d) To register customers who are interested in receiving information about future

shows, and e-mail information to these customers who are willing to receive it

(direct marketing).

(e) Perhaps also obtain customer feedback about performances.

There are other opportunities for electronic marketing. For example, theatres could

link with travel firms, hotels and restaurants to offer holiday breaks to customers as

a joint package of services and entertainment.

45 Leek and Flood

(b) Value chain analysis is a model for assessing performance. Each activity in the

value chain can be investigated, to establish whether it adds value

successfully.

(c) The activities in the value chain are the primary and secondary activities. In

this case study, the identifiable activities in the value chain are inbound

logistics (delivery of parts to the plumbers’ vans), operations (plumbing

services), marketing (door-to-door marketing, directory advertising, web site,

word of mouth), after-sales service (warranties and response to complaints)

and procurement (buying parts from the single supplier). There is also some

reference to human resource management, since plumbers are given regular

training. There is no information relating to infrastructure and technological

development.

46 Business case

A report presenting a business case for a new IS/IT system should be presented

clearly. The report should have a logical structure, and it should present the

necessary information. Appendices should be used to show details, and the main

body of the report should be kept reasonably short.

A logical structure for a report would be as follows:

(1) Introduction. Explain the purpose of the report and the terms of reference for

the report writer.

(2) Current position. Explain the current position. Indicate the nature of the

current problem or opportunity.

(3) Where we want to be. Explain the business objective, and what the business is

trying or should be trying to achieve.

Paper P3: Business analysis

492 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(4) Where we are. Compare ‘where we want to be’ with ‘where we are’ or ‘where

we will be if nothing is done’.

(5) Gap analysis. The comparison of ‘where we are’ and ‘where we want to be’

should be assessed, to establish the need for movement to get from ‘here to

there’.

(6) Options for closing the gap should be described in broad outline. There may

be several different ways of trying to close the gap.

(7) For each ‘realistic’ option there should be an estimate of the costs and benefits.

Benefits may not be measurable in financial terms, and a comparison of

financial costs with intangible benefits may be appropriate.

(8) Summary. A brief summary of each option should be given, with a

comparison of their ‘net benefits’.

(9) Recommendation. The report should conclude with a recommendation. If a

business case for a new system has been made successfully, the report’s

recommendation should be to develop the preferred option.

47 Risk management process

All projects have risks. The risk management process involves identifying and

assessing these risks, and taking measures to avoid or control them. The

effectiveness of risk control measures should be monitored. The process should be

repeated regularly, as a risk management control cycle.

The process involves:

(a) Risk identification. Risks must be identified, perhaps by a special risk

management committee, or by the project team.

(b) Risk assessment. Each risk must be assessed. The aim is to decide how

significant the risk may be. The reason for assessing significance is to make a

decision about the risk avoidance or control action that might be appropriate,

in view of the size of the risk.

(c) Typically, a risk is assessed by estimating the probability that an adverse

event will happen, and the impact it would have if it did happen. (The

expected value of the cost of a risk is its probability multiplied by its impact.)

(d) Having assessed each risk, management must decide on appropriate

measures to deal with it. Risks that would have an unacceptable impact

should be avoided. For example, the risk of damage from a natural disaster

can be avoided through insurance. For some risks, control measures may be

taken to reduce the risks. For example, the risks of errors in writing new

software for a system can be reduced by means of extensive testing.

(e) Control measures should be implemented.

(f) The effectiveness of control measures should be monitored.

(g) In cases where control measures fail to work, management should investigate

the reason for the control failure, and try to learn lessons for the future. If the

risk remains, more effective control measures should be devised and

implemented.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 493

48 Project manager

(a) A project has number of characteristics:

(i) The project should have a specific objective. The objective of a feasibility

study is to produce a feasibility report with a recommendation.

(ii) A project team is assembled to carry out the work. A feasibility study is

carried out by a specially-assembled study team.

(iii) A project should have a schedule and a time scale for completion. A

feasibility study has a target date for submitting the feasibility report.

(iv) A project should have a customer. For a feasibility study, this is the

steering committee (or similar decision-making body).

(v) A project should have a budget. A feasibility study ought to be given a

budget.

(b) Seven general responsibilities of a project manager include:

1 Selecting and organising the project team.

2 Agreement of the terms of reference with the project sponsor/computer

system user.

3 Planning the schedule of project activities.

4 Agreement of the project milestones and deliverables with the project

sponsor/senior management.

5 Control over the progress of the project

6 Control over the project budget

7 Conducting an end-of-project review meeting.

49 Project management software

1 The package can be used to produce charts and graphs, such as critical path

charts and Gantt charts

2 The package can be used to record budgeted and actual costs of the project,

and produce budgetary control reports.

3 The package can be used to schedule resources for the various tasks in a

project.

50 Requirements creep

Requirements creep is a term used to describe gradual changes made by the user to

the user requirements for a new system. If the user continually makes changes to the

requirements, completion of the project may be delayed.

There are two approaches to controlling requirements creep.

(a) Accept that requirements creep is inevitable, and use a Spiral method

approach to system development. Prototypes of the new system can be

introduced, and the system can be made operational, before the final

prototype is developed. This avoids delay in implementing the new system.

Paper P3: Business analysis

494 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The user also has the opportunity to make changes to the user requirements,

because new prototypes can be developed to include the new requirements.

(b) Establish a formal system for agreeing and authorising changes to user

requirements. The user will then need to justify changes, and get them

formally approved by management (at a suitable level of seniority). A formal

procedure could include:

A formal document including a request for a change to the user

requirements

A formal assessment of the impact the change will have (on the project

costs and completion time, and on the user’s costs and benefits from the

system)

A discussion of the proposed change and its impact, between the user and

the project team

Formal authorisation of the change in requirements

Recording the change and its justification in the documentation for the

project.

51 Balanced scorecard

(a) To set a number of performance targets in each of four key areas, with the aim

of achieving strategic objectives if all the performance targets are met.

(b) Financial targets

Customer satisfaction targets

Targets for the enhancement of internal processes

Targets for learning and growth (creating capabilities in employees and

systems).

(c) A balanced scorecard approach might be suitable for not-for-profit

organisations, where financial objectives are not as dominant as in commercial

organisations. Financial objectives in these organisations are often aimed at

achieving revenue targets or controlling costs, rather than making profits.

Profit-making entities might also choose a balanced scorecard approach when

they recognise the need to establish longer-term strategic objectives and not

concentrate exclusively on short-term profitability. The achievement of longer-

term objectives is often measured better by performance relating to non-

financial targets than by using financial targets (which tend to focus on the

short term).