ACCA F9 Financial Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 8: Discounted cash flow

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 165

DCF is based on cash flows, not accounting profits. It is therefore much more

suitable than the ARR method for investment appraisal.

It evaluates all cash flows from the project, unlike the payback method which

considers only those cash flows in the payback period.

It gives a single figure, the NPV, which can be used to assess the value of the

investment project. The NPV of a project is the amount by which the project

should add to the value of the company, in terms of ‘today’s value’.

The NPV method provides a decision rule which is consistent with objective of

maximisation of shareholders’ wealth. In theory, a company ought to increase in

value by the NPV of an investment project (assuming that the NPV is positive).

The main disadvantages of the NPV method are:

The time value of money and present value are concepts that are not easily

understood

There might be some uncertainty about what the appropriate cost of capital or

discount rate should be for applying to any project. Cost of capital is considered

in more detail in a later chapter.

Paper F9: Financial management

166 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Internal rate of return (IRR) method

The investment decision rule with IRR

Calculating the IRR of an investment project

Advantages and disadvantages of the IRR method

Summary: comparison of the four investment appraisal methods

3 Internal rate of return (IRR) method

The internal rate of return method (IRR method) is another method of investment

appraisal using DCF.

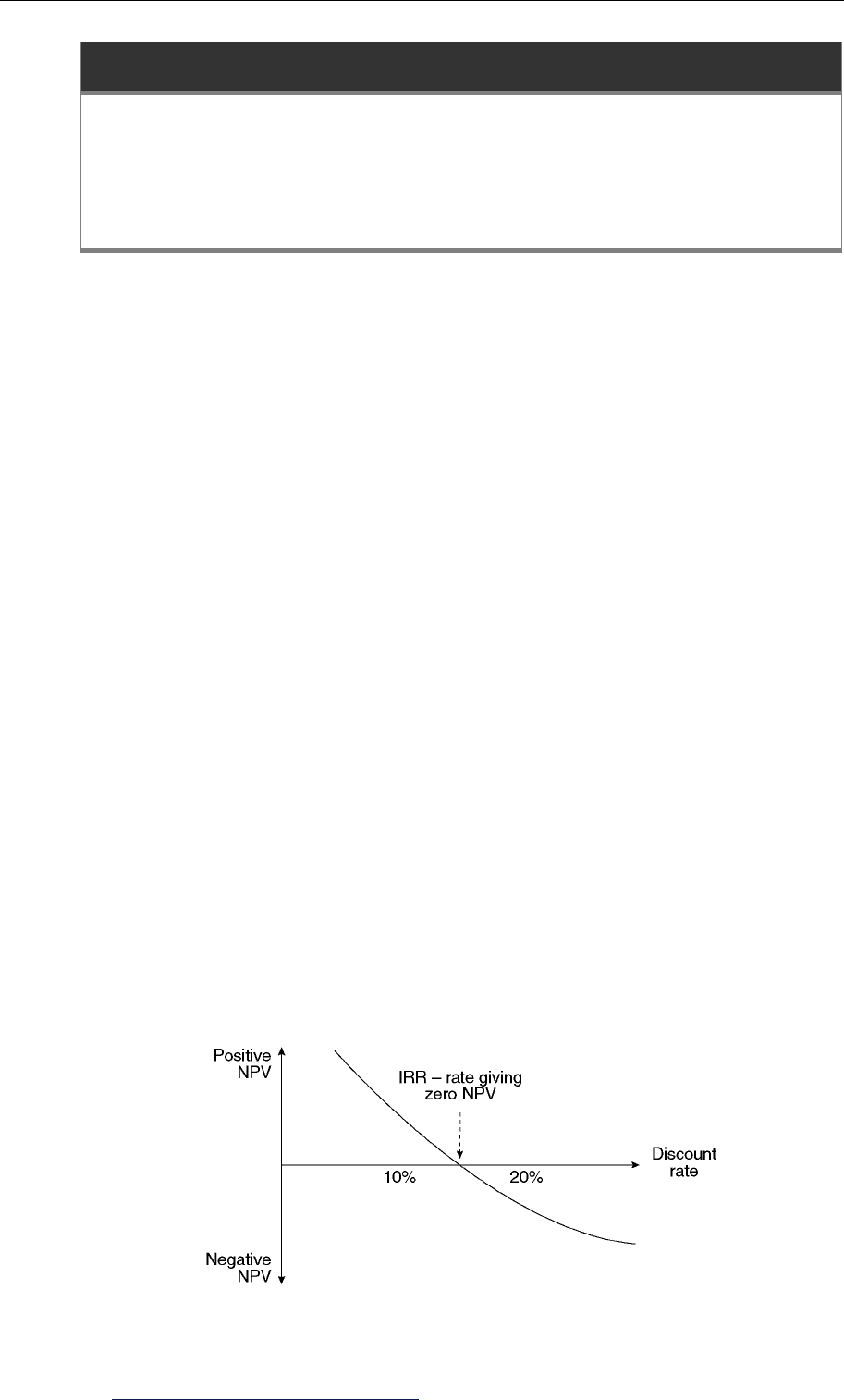

The internal rate of return of a project is the discounted rate of return on the

investment.

It is the average annual investment return from the project

Discounted at the IRR, the NPV of the project cash flows must come to 0.

The internal rate of return is therefore the discount rate that will give a net present

value = $0.

3.1 The investment decision rule with IRR

A company might establish the minimum rate of return that it wants to earn on an

investment. If other factors such as non-financial considerations and risk and

uncertainty are ignored:

If a project IRR is equal to or higher than the minimum acceptable rate of return,

it should be undertaken

It the IRR is lower than the minimum required return, it should be rejected.

Since NPV and IRR are both methods of DCF analysis, the same investment decision

should normally be reached using either method.

The internal rate of return is illustrated in the diagram below:

Chapter 8: Discounted cash flow

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 167

3.2 Calculating the IRR of an investment project

The IRR of a project can be calculated by inputting the project cash flows into a

financial calculator. In you examination, you might be required to calculate an IRR

without a financial calculator. An approximate IRR can be calculated using

interpolation.

To calculate the IRR, you should begin by calculating the NPV of the project at two

different discount rates.

One of the NPVs should be positive, and the other NPV should be negative.

(This is not essential. Both NPVs might be positive or both might be negative,

but the estimate of the IRR will then be less reliable.)

Ideally, the NPVs should both be close to zero, for better accuracy in the estimate

of the IRR.

When the NPV for one discount rate is positive NPV and the NPV for another

discount rate is negative, the IRR must be somewhere between these two discount

rates.

Although in reality the graph of NPVs at various discount rates is a curved line, as

shown in the diagram above. Using the interpolation method we assume that the

graph is a straight line between the two NPVs that we have calculated. We can then

use linear interpolation to estimate the IRR, to a reasonable level of accuracy.

The interpolation formula

If the NPV at A% is positive, + $P

and if the NPV at B% is negative, - $N

()

⎥

⎦

⎤

⎢

⎣

⎡

−×

+

+= %A B

N P

P

A% IRR

Ignore the minus sign for the negative NPV. For example, if P = + 75 and N = - 30,

then P + N = 105.

Example

A business requires a minimum expected rate of return of 12% on its investments. A

proposed capital investment has the following expected cash flows.

Year

$

0 (80,000)

1 20,000

2 36,000

3 30,000

4 17,000

Paper F9: Financial management

168 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Required

Calculate the NPV at a cost of capital of 10% and a cost of capital of 15%. Use these

NPV figures to estimate the IRR

Answer

Year

Cash

flow

Discount

factorat10%

Presentvalue

at10%

Discount

factorat15%

Present

valueat15%

$ $ $

0 (80,000) 1.000 (80,000) 1,000 (80,000)

1 20,000 0.909 18,180 0.870 17,400

2 36,000 0.826 29,736 0.756 27,216

3 30,000 0.751 22,530 0.658 19,740

4 17,000 0.683 11,611 0.572 9,724

–

–––––––

––––––––

NPV +2,057 (5,920)

–

–––––––

––––––––

The IRR is above 10% but below 15%.

Using the interpolation method:

The NPV is + 2,057 at 10%.

The NPV is – 5,920 at 15%.

The NPV therefore falls by 7,977 between 10% and 15%.

The estimated IRR is:

()

()

⎥

⎦

⎤

⎢

⎣

⎡

−×

+

+= %10 15

5,920 2,057

2,057

10% IRR

= 10% + 1.3%

= 11.3%

Recommendation

The project is expected to earn a DCF return below the target rate of 12%, and on

financial grounds it is not a worthwhile investment.

3.3 Advantages and disadvantages of the IRR method

The main advantages of the IRR method of investment appraisal are:

As a DCF appraisal method, it is based on cash flows, not accounting profits.

Like the NPV method, it recognises the time value of money.

It is easier to understand an investment return as a percentage return on

investment than as a money value NPV in $.

For accept/reject decisions on individual projects, the IRR method will reach the

same decision as the NPV method.

Chapter 8: Discounted cash flow

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 169

The disadvantages of the IRR method are:

It is a relative measure (% on investment) not absolute measure in $. Because it is

a relative measure, it ignores the absolute size of the investment. For example,

which is the better investment if the cost of capital is 10%:

− an investment with an IRR of 15% or

− an investment with an IRR of 20%?

If the investments are mutually exclusive, and only one of them can be

undertaken the correct answer is that it depends on the size of each of the

investments. This means that the IRR method of appraisal can give an incorrect

decision if it is used to make a choice between mutually exclusive projects

Unlike the NPV method, the IRR method does not indicate by how much an

investment project should add to the value of the company.

Example

There are two mutually exclusive projects.

Year Project 1

Project 2

$ $

(1,000) (10,000)

1,200 4,600

- 4,600

- 4,600

IRR 20%

18%

NPV at 15% + $43 + $503

Which is better?

Answer

Project 2 is better, because it has the higher NPV. Project 2 will add to value by $503

but Project 1 will add value of just $43.

3.4 Summary: comparison of the four investment appraisal methods

A comparison of the four investment appraisal methods is given in the table below.

The key points to note are that:

DCF is superior to the ARR method and payback method of investment appraisal

It is often equally as good to use NPV or IRR

However, NPV has two advantages over IRR

− The NPV method indicates the value that the investment should add (if the

NPV is positive) or the value that it will destroy (if the NPV is negative).

− When there are two or more mutually exclusive projects, the NPV will

always identify the project that should be selected. This is the project that

will provide the highest value (NPV).

Paper F9: Financial management

170 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The IRR method has the advantage of being more easily understood by non-

accountants

Another disadvantage of the IRR method is that a project might have two or

more different IRRs, when some annual cash flows during the life of the project

are negative. (The mathematics that demonstrate this point are not shown here.)

ARR Payback Discounted cash flow

Disadvantages Advantages Advantages

Financial

profits, not

cash flows

Balance sheet

values, not

cash

investment

cost.

Cash flows, not

accounting

values

Focus on

recovering the

cost of the

investment

Based on investment cash flows, not

accounting profit

Recognises the time value of money

Recognises all cash flows, over the full life of

the project

By far the best investment appraisal method

Required return is based on the organisation’s

cost of finance.

Disadvantages NPV IRR

Choice of

maximum

payback period

is arbitrary

Indicates the increase in

the value of the

company that should

be expected if it were to

undertake the

investment.

More easily

understood than

NPV by a non-

accountant.

Ignores cash

from the project

after payback

If a choice has to be made between two (or

more) mutually exclusive projects, the NPV

method is more reliable than IRR.

Ignores the time

value of money.

Chapter 8: Discounted cash flow

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 171

Annuities and perpetuities

Definition of an annuity

Calculating the PV of an annuity

Annuity discount tables

Using annuities and annuity factors for investment appraisal

Definition of a perpetuity

Present value of a perpetuity

4 Annuities and perpetuities

4.1 Definition of an annuity

An annuity is a constant cash flow for a given number of time periods. A capital

project might include estimated annual cash flows that are an annuity.

Examples of annuities are:

$30,000 each year for years 1 – 5

$20,000 each year for years 3 – 10

$500 each month for months 1 – 24.

The present value of an annuity can be calculated using annuity factors, rather than

using discount factors to calculate the present value of the cash flow for each

individual year.

4.2 Calculating the PV of an annuity

If you need to calculate the present value of $50,000 per year for years 1 – 3 at a

discount rate of 9%, you could calculate this as follows:

Year

Cash flow

Discount factor

at 9%

Present

value

$

$

1 50,000 1/(1.09) = 0.917

45,850

2 50,000 1/(1.09)

2

= 0 842

42,100

3 50,000 1/(1.09)

3

= 0.772

38,600

NPV

126,550

There is a formula for calculating the present value of an annuity. The formula is:

PV =

A

r

× 1 −

1

1 + r

()

n

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

Where:

A = the constant annual cash flow (the annuity)

Paper F9: Financial management

172 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

r = discount rate, as a proportion

n = number of time periods

The present value of $50,000 per year for three years at a discount rate of 9% can

therefore be calculated as:

$50,000

0.09

× 1 −

1

1.09

()

3

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

= [$50,000/0.09] × (1 – 0.0.77218) = $50,000 × 0.22782

= $126,567.

4.3 Annuity discount tables

Another way of calculating the PV of an annuity is to multiply the annuity by the

sum of the discount factors for the years in which the cash flows occur. In the

example above, the PV of $50,000 for years 1 – 3 at a discount rate of 9% could be

calculated as:

$50,000 × (0.917 + 0.842 + 0.772) = $50,000 × 2.531 = $126,550.

The discount factors for annuities are simply the sum of the annual discount factors

for each year of the annuity. Discount tables for annuities are included in the

formula and tables sheets near the end of this text. These tables will be provided in

your examination. An extract is shown below.

Extract from annuity tables

Discount rates (r)

Periods

(n) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909

2 1.970 1.942 1.913 1.886 1.859 1.833 1.808 1.783 1.759 1.736

3 2.941 2.884 2.829 2.775 2.723 2.673 2.624 2.577 2.531 2.487

4 3.902 3.808 3.717 3.630 3.546 3.465 3.387 3.312 3.240 3.170

5 4.853 4.713 4.580 4.452 4.329 4.212 4.100 3.993 3.890 3.791

The annuity factors are for periods starting in period 1 (year 1). For example, the

annuity factor for years 1 – 3 at 9%, from the table, is 2.531.

Examples

The annuity factor for years 1 – 2 at a cost of capital of 8% = 1.783 (n = 2, discount

factor 8%. This is the sum of the discount factors at 8% for years 1, and 2 (0.926 +

0.857).

The annuity factor for years 1 – 5 at a cost of capital of 10% = 3.791 (n = 5, discount

factor = 10%). This is the sum of the discount factors at 10% for years 1, 2, 3, 4 and 5

(0.909 + 0.826 + 0.751 + 0.683 + 0.621).

Chapter 8: Discounted cash flow

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 173

4.4 Using annuities and annuity factors for investment appraisal

Annuity discount factors can be used in DCF investment analysis, mainly to make

the calculations easier and quicker.

Example

What is the present value of the cash flows for a project, if the cash flows are $60,000

each year for years 1 – 7, and the cost of capital is 15%?

Answer

$60,000 × 4.160 (annuity factor at 15%, n = 7) = $249,600.

Example

What is the present value of the following cash flows, when the cost of capital is

12%?

Year

Annualcash

flow

Discount

factorat12%

Present

value

$ $

0 (100,000)

1 10,000

2 15,000

3–15 20,000

NPV

Answer

Annuity factor at 12%, years 1 – 15 = 6.811

Annuity factor at 12%, years 1 – 2 = 1.690

Therefore annuity factor at 12%, years 3 – 15 = 6.811 – 1.690 = 5.121

Year

Annualcash

flow

Discount

factorat12%

Present

value

$ $

0 (100,000) 1.000 (100,000)

1 10,000 0.893 8,930

2 15,000 0.797 11,955

3–15 20,000 5.121 102,420

NPV +23,305

Paper F9: Financial management

174 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example

A company is considering an investment of $70,000 in a project. The project life

would be five years.

What must be the minimum annual cash returns from the project to earn a return of

at least 9% per annum?

Answer

Investment = $70,000

Annuity factor at 9%, years 1 – 5 = 3.890

Minimum annuity required = $17,995 (= $70,000/3.890)

Exercise 3

A company is considering an investment of $70,000 in a project. The project life

would be ten years. The cash flows would be $15,000 each year for years 1 – 5 and

$10,000 each year for years 6 – 10. The cost of capital is 8%.

What is the NPV of the project?

4.5 Definition of a perpetuity

A perpetuity is a constant annual cash flow ‘forever’, or into the long-term future.

In investment appraisal, an annuity might be assumed when a constant annual cash

flow is expected for a long time into the future.

4.6 Present value of a perpetuity

The present value of a perpetuity is C/r, where:

C is the constant annual cash flow in perpetuity

r is the cost of capital, for example 0.08, 0.10 etcetera.

Examples

The present value of $2,000 in perpetuity, starting in Year 1, given a cost of capital of

8%, is: $2,000/0.08 = $25,000.

The present value of $5,500 in perpetuity, starting in Year 4, given a cost of capital of

11%, is calculated as follows:

The perpetuity starts in Year 4, therefore the ‘present value’ as at the end of Year

3 = $5,500/0.11 = $50,000.