ACCA F9 Financial Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 6: Cash management

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 135

There has to be a trade-off. The greater the liquidity and safety, then generally the

lower will be the interest rate earned (profitability).

4.2 Ways of investing short term

There are various possible short-term investment options for cash.

Savings accounts and interest-earning deposits

Savings accounts

. Some banks might allow a business to place short-term cash in a

savings account. However, banks do not like companies to use a savings account in

the same way as a normal current account, with frequent deposits and withdrawals.

The bank might insist on a minimum amount of deposit and a minimum notice

period for withdrawals.

If the surplus is fairly large, a bank will usually help a business customer to place

surplus cash on short-term deposit in the

money markets (interbank market). Money

market rates might be higher than rates on savings accounts.

Money market investments

It is also possible to purchase some money market investments, such as Treasury

bills and Certificates of Deposit.

Treasury bills

are short-term debt instruments issued by the government. They are

usually issued by the government for a period of three months (91 days) or possibly

six months, and redeemed at the end of that time. They are very secure (‘risk-free’)

since the central government owes the money. They are also very liquid, and can be

sold in the market before maturity if required. However, because they are short-

term, very liquid and very safe, the rate of return (yield) tends to be low.

(Note: Treasury bills are issued at a discount to their par value and are redeemed at

par. For example UK 91-day Treasury bills might be issued at £99.00 and redeemed

by the government at maturity for £100. During the 91-day period the bills can be

sold in the market if required, and the market price should move towards £100 as

the maturity date approaches.)

Certificates of Deposit

issued by banks. These are certificates giving their holder

the right to ownership of a deposit of cash with the bank, plus interest, at a date in

the future (the maturity date for the CD). The market for CDs is liquid, and CDs can

be sold easily if the cash is required before the bank deposit reaches maturity.

Short-dated government bonds

. The government issues long-dated bonds

(‘Treasury bonds’) as well as short-dated Treasury bills. When these bonds are

nearing their maturity, they are an attractive short-term investment. They are as

secure as Treasury bills, and possibly even more liquid.

Paper F9: Financial management

136 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Longer-term securities as short-term investments

Bonds

traded in the bond markets. These normally offer a higher return than short-

term investments, because there is greater risk for the investor. Bondholders can sell

their investment in the secondary bond market if they need to convert the

investment back into cash.

However, there is an investment risk. Bond prices can fall if bond yields in the

market rise. Bond prices can also fall if the credit rating of the bond issuer falls. In

addition, the bond market is not always liquid, so it might also be difficult to sell the

bonds for a fair price when the cash is needed. (However, the domestic market for

government bonds is normally very liquid. The problem with market liquidity

relates more to corporate bonds and the international bond markets.)

Bonds are therefore inadvisable as a short-term investment, unless the investor is

willing to accept the risk that bond prices might fall.

Equity. Investing in the shares of other companies is a high-risk investment as there

is no guarantee of return of capital value. Share prices can fall as well as rise, and

dividend payments are at the discretion of the directors, and usually only paid twice

a year. If the shares are quoted, then there will be some liquidity as they will be

tradable in the secondary market.

Investing in shares is not recommended as a short-term investment for surplus cash,

because of the risk from volatility in share prices.

4.3 Dealing with shortfalls of cash

If the cash flow forecast or the cash budget indicates a shortage of cash, measures

must be taken to deal with the problem. An entity must have the cash that it needs

to continue in operation.

If the entity does not have short-term investments that it can sell, it will need to

obtain long-term capital or short-term funds.

Long-term funding. A company can consider raising long-term funds by issuing

new shares for cash.

Alternatively, an entity might be able to borrow long term, by means of issuing loan

stock (bonds) or obtaining a medium-term bank loan.

Various short-term sources of cash might also be available.

Bank overdrafts – These are very popular with small and medium-sized

businesses. Obtaining a bank overdraft is usually the easiest way for a small

business to obtain finance.

− The advantage of a bank overdraft is that the borrower pays interest only on

the amount of the overdraft balance.

− However, overdrafts are expensive (the interest rate is comparatively high

compared with other sources of finance). Overdrafts are also are repayable to

the bank on demand. The bank can ask for immediate repayment at any time

Chapter 6: Cash management

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 137

that it wishes. Overdrafts can therefore be a high-risk source of finance,

especially for businesses with cash flow difficulties – in other words, the

businesses that are usually in greatest need of an overdraft!

− Bank overdrafts should only be used to finance fluctuating levels of cash

shortfalls. If the cash shortfall looks more permanent, other sources of

finance should be used.

Short-term bank loans – The main difference between a loan and a bank

overdraft is that a loan is arranged for a specific period and the capital

borrowed, together with the interest, is repaid according to an agreed schedule

and over an agreed time period. They are not repayable on demand before

maturity, provided the borrower keeps up the payments. Interest is payable on

the full amount of the outstanding loan. However, the bank may demand

security for a loan, for example in the form of a fixed and floating charge over

the assets of the business.

Debt factoring – Some business entities use the services of a debt factor. The

debt factor undertakes to administer the sales receivables ledger of the client

business, issuing invoices and collecting payments. In addition, the factor will be

prepared to advance cash to the client business in advance of receiving payment.

Typically, a factor will lend a client up to 80% of the value of outstanding trade

receivables, and charge interest on the amount of the loan. However, debt factor

services can be expensive.

4.4 Cash management in larger organisations

Larger businesses find it much easier than smaller businesses to raise cash when

they are expecting a cash shortfall. Similarly, when they have a cash surplus, they

find it easier to invest the cash.

Cash management in a large organisation is often handled by a specialist

department, known as the

treasury department. One role of the treasury

department is to centralise the control of cash, to make sure that:

cash is used as efficiently as possible

surpluses in one part of the business (for example, in one profit centre) are used

to fund shortfalls elsewhere in the business, and

surpluses are suitably invested and mature when the cash is needed.

Making the management of cash the responsibility of a centralised treasury

department has significant advantages.

Cash is managed by specialist staff – improving cash management efficiency.

All the cash surpluses and deficits from different bank accounts used by the

entity can be ‘pooled’ together into a central bank account. This means that cash

can be channelled to where it is needed, and overdraft interest charges can be

minimised.

Central control over cash lowers the total amount of cash that needs to be kept

for precautionary reasons. If individual units had to hold their own ‘safety stock’

of cash, then the total amount of surplus cash would be higher (when added

together) than if cash management is handled by one department.

Paper F9: Financial management

138 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Putting all the cash resources into one place increases the negotiating power of

the treasury department to get the best deals from the banks.

4.5 Functions of a treasury department

The central treasury department is responsible for making sure that cash is available

in the right amounts, at the right time and in the right place. To do this, it must:

produce regular cash flow forecasts to predict surpluses and shortfalls

arrange short-term borrowing and investment when necessary

arrange to purchase foreign currency when needed, and arrange to sell foreign

currency cash receipts

protect the business against the risk of adverse movements in foreign exchange

rates, when the business has receipts and payments, or loans and investments

deal with the entity’s banks

finance the business on a day-to-day basis, for example by arranging facilities

with a bank

advise senior management on long-term financing requirements.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 139

Paper F9

Financial management

CHAPTER

7

Introduction to investment

appraisal and capital

investment decisions

Contents

1 Capitalexpenditure,investmentappraisaland

capitalbudgeting

2 Accountingrateofreturn(ARR)method

3 Thepaybackmethodofcapitalinvestment

appraisal

4 Relevantcostsininvestmentdecisions

Paper F9: Financial management

140 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Capital expenditure, investment appraisal and capital budgeting

Capital expenditure

Investment appraisal

Capital budgeting

Features of investment projects

Methods of investment appraisal

The basis for making an investment decision

1 Capital expenditure, investment appraisal and capital

budgeting

1.1 Capital expenditure

Capital expenditure is spending on non-current assets, such as buildings and

equipment, or investing in a new business. As a result of capital expenditure, a new

non-current asset appears on the statement of financial position (balance sheet),

possibly as an ‘investment in subsidiary’.

In contrast revenue expenditure refers to expenditure that does not create long-term

assets, but is either written off as an expense in the income statement in the period

that it is incurred, or that creates a short-term asset (such as the purchase of

inventory).

Capital expenditure initiatives are often referred to as investment projects, or ‘capital

projects’. They can involve just a small amount of spending, but in many cases large

amounts of expenditure are involved.

A distinction might possibly be made between:

essential capital spending to replace worn-out assets and maintain operational

capability

discretionary capital expenditure on new business initiatives that are intended to

develop the business make a suitable financial return on the investment.

Examination questions usually focus on discretionary capital expenditure.

1.2 Investment appraisal

Before capital expenditure projects are undertaken, they should be assessed and

evaluated. As a general rule, projects should not be undertaken unless:

they are expected to provide a suitable financial return, and

the investment risk is acceptable.

Investment appraisal is the evaluation of proposed investment projects involving

capital expenditure. The purpose of investment appraisal is to make a decision

Chapter 7: Introduction to investment appraisal and capital investment decisions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 141

about whether the capital expenditure is worthwhile and whether the investment

project should be undertaken.

1.3 Capital budgeting

Capital expenditure by a company should provide a long-term financial return, and

spending should therefore be consistent with the company’s long-term corporate

and financial objectives. Capital expenditure should therefore be made with the

intention of implementing chosen business strategies that have been agreed by the

board of directors.

Many companies have a capital budget, and capital expenditure is undertaken

within the agreed budget framework and capital spending limits. For example, a

company might have a five-year capital budget, setting out in broad terms its

intended capital expenditure for the next five years. This budget should be

reviewed and updated regularly, typically each year.

Within the long-term capital budget, there should be more detailed spending plans

for the next year or two.

Individual capital projects that are formally approved should be included within

the capital budget.

New ideas for capital projects, if they satisfy the investment appraisal criteria

and are expected to provide a suitable financial return, might be approved

provided that they are consistent with the capital budget and overall spending

limits.

Investment appraisal and capital budgets

Investment appraisal therefore takes place within the framework of a capital budget

and strategic planning. It involves

Generating capital investment proposals in line with the company’s strategic

objectives.

Forecasting relevant cash flows relating to the project

Evaluating the projects

Implementing projects which satisfy the company’s criteria for deciding whether

the project will earn a satisfactory return on investment

Monitoring the performance of investment projects to ensure that they perform

in line with expectations.

1.4 Features of investment projects

Many investment projects have the following characteristics:

The project involves the purchase of an asset with an expected life of several

years, and involves the payment of a large sum of money at the beginning of the

project. Returns on the investment consist largely of net income from additional

profits over the course of the project’s life.

Paper F9: Financial management

142 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The asset might also have a disposal value (residual value) at the end of its

useful life.

A capital project might also need an investment in working capital. Working

capital also involves an investment of cash.

Alternatively a capital investment project might involve the purchase of another

business, or setting up a new business venture. These projects involve an initial

capital outlay, and possibly some working capital investment. Financial returns

from the investment might be expected over a long period of time, perhaps

indefinitely.

1.5 Methods of investment appraisal

There are four methods of evaluating a proposed capital expenditure project. Any

or all of the methods can be used, but some methods are preferable to others,

because they provide a more accurate and meaningful assessment.

The four methods of appraisal are:

Accounting rate of return (ARR) method

Payback method

Discounted cash flow (DCF) methods:

− Net present value (NPV) method

− Internal rate of return (IRR) method

Each method of appraisal considers a different financial aspect of the proposed

capital investment.

Chapter 7: Introduction to investment appraisal and capital investment decisions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 143

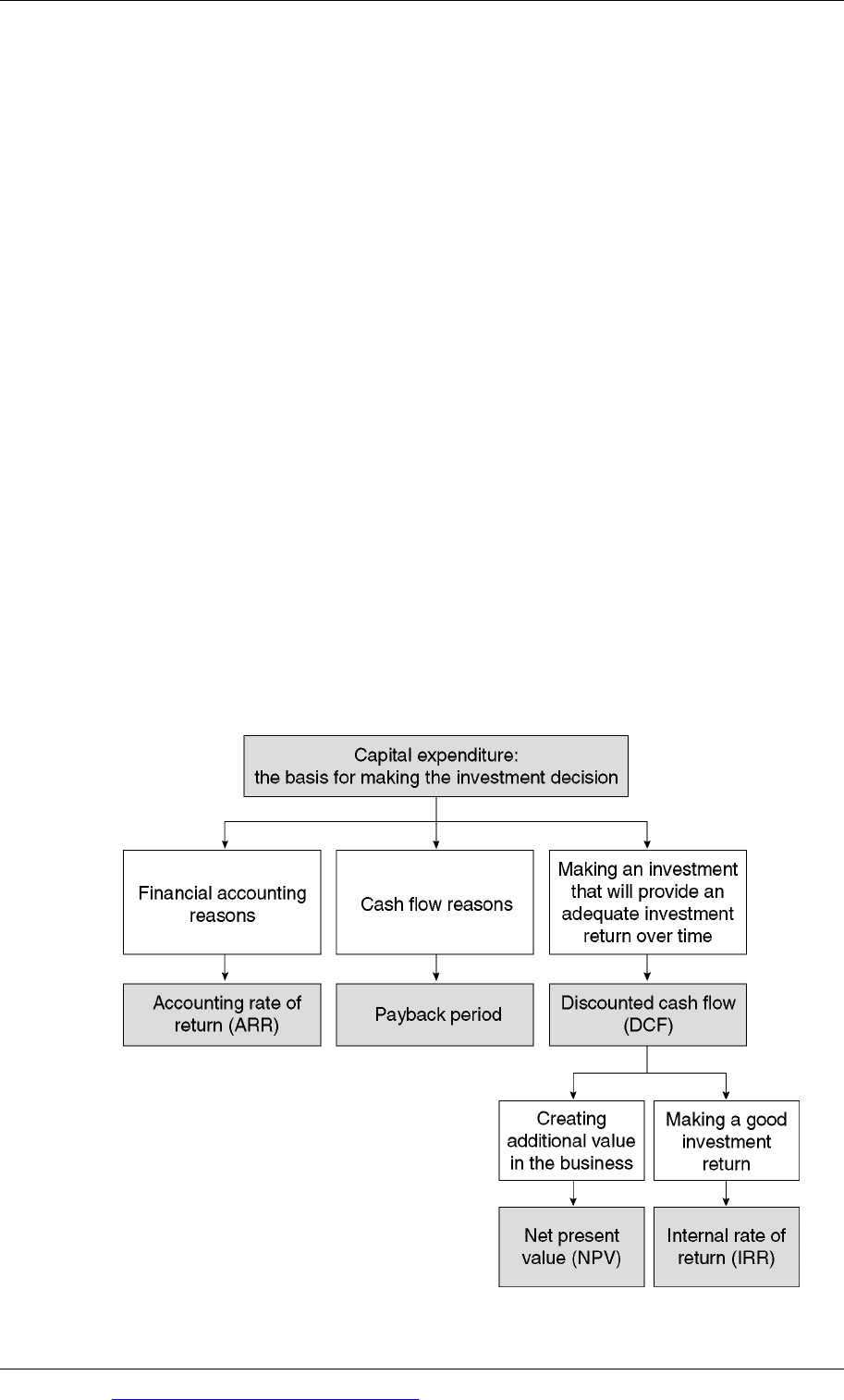

1.6 The basis for making an investment decision

When deciding whether or not to make a capital investment, management must

decide on a basis for decision-making. The decision to invest or not invest will be

made for financial reasons in most cases, although non-financial considerations

could be important as well.

There are different financial reasons that might be used to make a capital

investment decision. Management could consider:

the effect the investment will have on the accounting return on capital

employed, as measured by financial accounting methods. If so, they might use

accounting rate of return (ARR) /return on investment (ROI) as the basis for

making the decision

the time it will take to recover the cash invested in the project. If so, they might

use the payback period as the basis for the investment decision

the expected investment returns from the project. If so, they should use

discounted cash flow (DCF) as a basis for their decision. DCF considers both the

size of expected future returns and the length of time before they are earned.

There are two different ways of using DCF as a basis for making an investment

decision:

Net present value (NPV) approach. With this approach, a present value is given

to the expected costs of the project and the expected benefits. The value of the

project is measured as the net present value (the present value of income or

benefits minus the present value of costs). The project should be undertaken if it

adds value. It adds value if the net present value is positive (greater than 0).

Internal rate of return (IRR) approach. With this approach, the expected return

on investment over the life of the project is calculated, and compared with the

minimum required investment return. The project should be undertaken if its

expected return (as an average percentage annual amount) exceeds the required

return.

The remainder of this chapter considers the accounting rate of return (ARR) method

and the payback method of appraisal

Paper F9: Financial management

144 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

capitalWorking

2

valueResidualequipmen

t

o

f

costInitial

employedCapital +

⎥

⎦

⎤

⎢

⎣

⎡

+

=

Accounting rate of return (ARR) method

Decision rule for the ARR method

Definition of ARR

Advantages and disadvantages of using the ARR method

2 Accounting rate of return (ARR) method

The accounting rate of return (ARR) from an investment project is the accounting

profit, usually before interest and tax, as a percentage of the capital invested. It is

similar to return on capital employed (ROCE), except that whereas ROCE is a

measure of financial return for a company or business as a whole, ARR measures

the financial return from specific capital project.

The essential feature of ARR is that it is based on accounting profits, and the

accounting value of assets employed.

2.1 Decision rule for the ARR method

The decision rule for capital investment appraisal using the ARR method is that a

capital project meets the criteria for approval if its expected ARR is higher than a

minimum target ARR or minimum acceptable ARR.

Alternatively the decision rule might be to approve a project if the return on capital

employed (ROCE) of the company as a whole will increase as a result of

undertaking the project.

2.2 Definition of ARR

If accounting rate of return (ARR) is used to decide whether or not to make a capital

investment, we calculate the expected annual accounting return over the life of the

project. The financial return will vary from one year to the next during the project;

therefore we have to calculate an average annual return.

If the ARR of the project exceeds a target accounting return, the project would be

undertaken. If its ARR is less than the minimum target, the project should be

rejected and should not be undertaken

Unfortunately, a standard definition of accounting rate of return does not exist.

There are two main definitions:

Average annual profit as a percentage of the average investment in the project

Average annual profit as a percentage of the initial investment.

You would normally be told which definition to apply. If in doubt, assume that

capital employed is the average amount of capital employed over the project life.