ACCA F7 (INT) Financial Reporting - Study text - 2010 - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 4: The regulatory framework

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 65

trading in their shares. In the UK for example, companies whose shares are traded

on the main London Stock Exchange must first obtain a ‘listing’ for those shares

from the financial markets regulator. To obtain and retain this listing, companies

must comply with certain Listing Rules, which include some requirements relating

to when the information, including financial reports, that ‘listed companies’ must

prepare and provide to the stock market.

1.3 Principles and rules

Company law consists of detailed rules. Accounting standards may be rules-based

or principles-based. IASs and IFRSs are mainly principles-based, though it can be

argued that in practice they are a mixture of rules and principles.

It is possible for rules and principles to complement each other. Many countries

(including the UK, Canada and Australia) have a regulatory system in which

company law deals only with a few specific matters. Detailed financial reporting

practice is developed by the accounting profession through accounting standards.

Accounting standards are generally (though not always) principles-based. This

allows reporting practice to develop over time in response to the needs of users and

changes in the business environment. Accounting standards usually allow preparers

to exercise judgement in developing accounting policies that are appropriate to the

circumstances of their particular entity.

In other countries (including most European countries and Japan), the content of

financial statements and accounting practice are prescribed in great detail by

company law. There is very little scope for individual judgement. Until fairly

recently, accounting standards were almost non-existent in these countries.

Because their existing framework is based on detailed rules, some users of

financial statements in these countries consider principles-based accounting to

be insufficiently rigorous.

Paper F7: Financial reporting (International)

66 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Constitution and objectives of the IASC Foundation and the IASB

The IASC Foundation

Structure of the IASC Foundation

The International Accounting Standards Board (IASB)

The International Financial Reporting Interpretations Committee (IFRIC)

Standards Advisory Council (SAC)

The influence of IOSCO

IFRSs and IASs

National standard setters and the IASB

2 Constitution and objectives of the IASC Foundation

and IASB

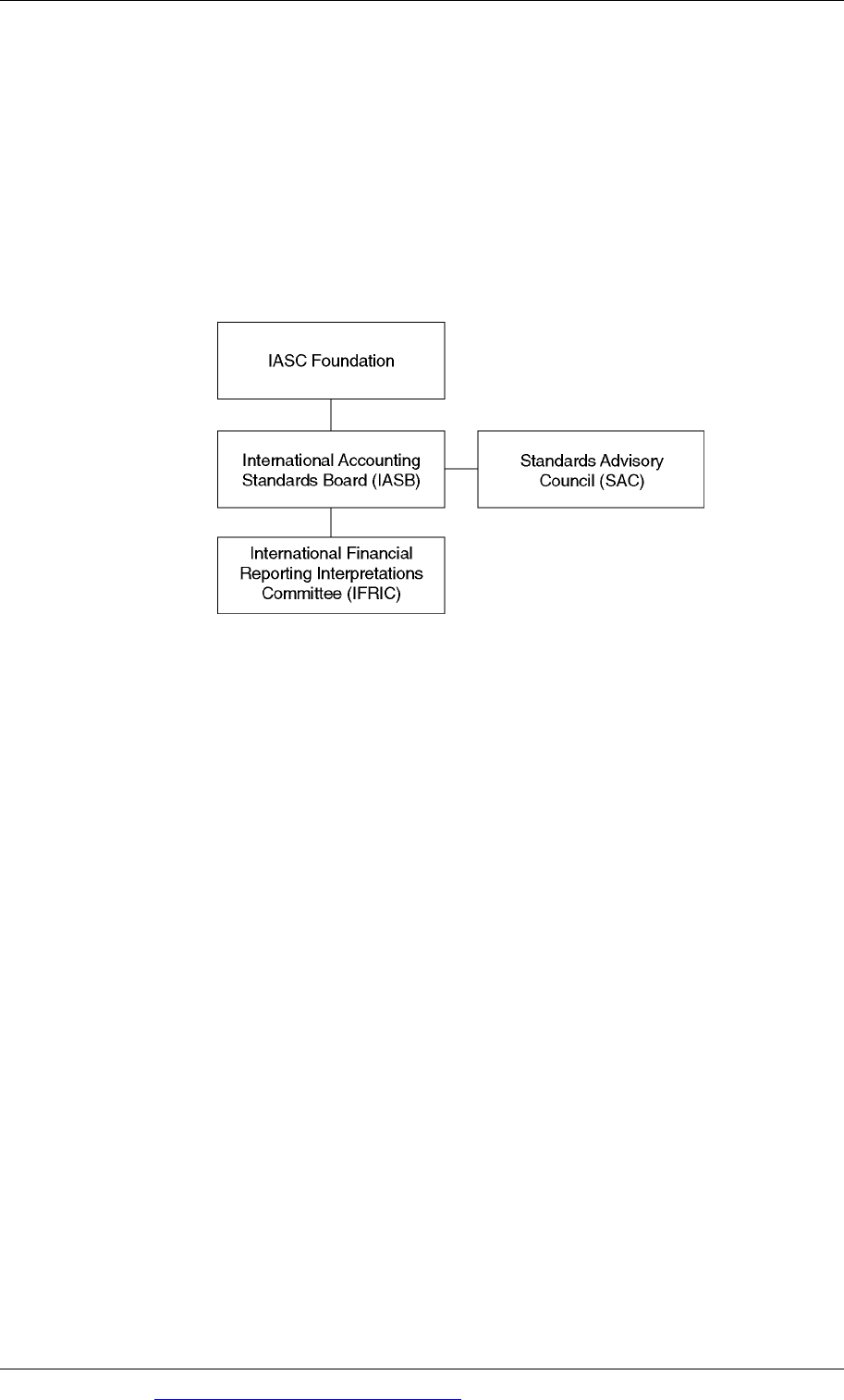

2.1 The IASC Foundation

The original International Accounting Standards Committee (IASC) was established

in 1973 to develop international accounting standards. The aim of international

standards is to harmonise accounting procedures throughout the world. The first

International Accounting Standards (IASs) were issued in 1975.

However, international accounting standards cannot be applied in any country

without the approval of the national regulators in that country. Many countries,

including the US and the UK, have continued to develop their own national

accounting standards.

In 2001, the constitution of the IASC was altered, and the Trustees formed the

International Accounting Standards Committee Foundation or IASC Foundation.

The 22 Trustees of the IASC Foundation are responsible for:

governance of the Foundation and the bodies within it

fund-raising.

The International Accounting Standards Board (IASB) is the standard-setting body

of the IASC Foundation.

The chairman of the IASB is also the Chief Executive of the IASC Foundation, and is

accountable to the Trustees.

The objectives of the IASC Foundation

The objectives of the IASC Foundation are to:

develop, in the public interest, a single set of high-quality global accounting

standards

Chapter 4: The regulatory framework

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 67

promote the use and rigorous application of those standards

to take account of the special needs of small and medium sized entities and

emerging economies

to bring about the convergence of national accounting standards and the

international accounting standards.

2.2 Structure of the IASC Foundation

The current structure of the IASC Foundation is as follows.

2.3 The International Accounting Standards Board (IASB)

The IASB is responsible for developing international accounting standards.

The IASB consists of 14 members, all with technical expertise in accounting, who are

appointed by the Trustees. Each IASB member is appointed for a five-year term,

which might be renewed once for a further five years.

Each IASB member has one vote, and approval of 8 members is required for the

publication of:

an exposure draft

a revised International Accounting Standard (IAS)

an International Financial Reporting Standard (IFRS)

a final Interpretation of the International Financial Reporting Interpretations

Committee (IFRIC).

The IASB has full responsibility for all IASB technical matters, including the issue of

IFRSs and revised IASs, and has full discretion over the technical agenda of the

IASB.

2.4 The International Financial Reporting Interpretations Committee (IFRIC)

The role of IFRIC is to issue rapid guidance where there are differing possible

interpretations of an international accounting standard. Its role is therefore to:

interpret international accounting standards (IASs and IFRSs)

Paper F7: Financial reporting (International)

68 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

issue timely guidance on issues not covered by an IAS or IFRS, within the

context of the IASB Framework

publish draft Interpretations for public comment. After studying responses to

the draft Interpretation, it will obtain IASB approval for a final (published)

Interpretation.

2.5 Standards Advisory Council (SAC)

The Standards Advisory Council (SAC) provides a forum through which the IASB is

able to gather opinions and advice from different countries and industries. The SAC

consists of experts from different countries and different business sectors, who offer

advice to the IASB.

2.6 The influence of IOSCO

IOSCO is the International Organisation of Securities Commissions. Securities

Commissions are the regulators of the stock markets in their country. The US

Securities and Exchange Commission (SEC) is a key IOSCO member.

Within each country, the financial markets regulator is responsible for the rules that

companies must follow if they wish to have their shares traded on the stock market.

An aim of IOSCO is to develop international investment, and a view of IOSCO is

that international investment will be encouraged if all major companies use the

same accounting standards for reporting their financial position and performance.

IOSCO has therefore been an influential supporter of the development of

international accounting standards. An IOSCO representative is a non-voting

observer at meetings of the IASB.

In 1995 the IASC agreed with IOSCO to develop a set of core standards. IOSCO also

agreed that if it approved these core standards, it would endorse them as an

acceptable basis of accounting for companies seeking to raise capital and list their

shares in all global stock markets (including the US).

The IASC completed its core standards with the issue of IAS39 in December 1998.

They were endorsed by IOSCO in 2000. IOSCO has now recommended that its

members (including the SEC) should permit multinational issuers of shares to use

financial statements based on IASs and IFRSs for cross-border share offerings and

listings. (However, the SEC is one of the few authorities that has not accepted IFRS

financial statements for company registration purposes.)

In 2004, the European Union (EU) agreed that all listed European companies should

prepare their group financial statements in accordance with IASs and IFRSs, for

periods beginning on or after 1

st

January 2005.

Companies listed on any stock exchange in the EU must therefore publish accounts

that comply with international accounting standards.

Chapter 4: The regulatory framework

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 69

2.7 IFRSs and IASs

When the new Constitution of the IASC Foundation was set up in 2001, the IASB

became the body responsible for:

developing and publishing accounting standards as IFRSs and

approving and publishing Interpretations of IFRSs.

Before the new Constitution was established, standards had been published as

International Accounting Standards (IASs) and Interpretations were published as

SIC Interpretations.

The IASB decided that all IASs and SICs that had been issued previously would

continue to be applicable, unless they are subsequently amended or withdrawn.

This means that IASs still in issue have the same status as IFRSs. It is convenient to

refer to IASs and IFRSs as ‘international accounting standards’.

2.8 National standard setters and the IASB

The IASB has no power to enforce its standards. Without the support of at least the

major national standard setters, IFRSs are unlikely to be adopted.

However, there are strong arguments for international convergence. (International

convergence means that the accounting standards of different countries move

towards each other, so that they are increasingly similar.) Most national standard

setters are committed to the principle of international convergence.

All the major national standard setting bodies are represented on the IASB, so that

they can influence the development of new standards and their views are taken into

account.

All the major national standard setters issue Discussion Papers and Exposure Drafts

in their own countries so that preparers and users in each country can comment on

them. Several national standard setters (including the UK Accounting Standards

Board) allow entities to adopt IFRSs rather than local standards if they choose.

Many standard setters are carrying out short term convergence projects in which

domestic standards are moved closer to IFRSs and IASs.

In addition, the IASB has been working with national standard setters on specific

projects. For example:

the IASB and the UK ASB worked together to develop IAS 36 Impairment of

assets and IAS 37 Provisions, contingent liabilities and contingent assets (and the

equivalent UK standards)

some other recent standards have been developed by a group of national

standard setters and the IASB working together

the IASB Framework was originally based on work carried out by the US FASB;

the Framework has in turn influenced the UK ASB in developing its own

conceptual framework

national standard setters sometimes carry out the research for IASB projects. For

example, the UK ASB has carried out work on accounting for leases.

Paper F7: Financial reporting (International)

70 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The role of the FASB

The US Financial Accounting Standards Board (FASB) has a special role in

developing new international standards.

The IASB and the FASB are currently working together in the following ways:

A short term convergence project aims to reduce differences between certain

IASs and IFRSs and certain US standards. The IASB issued IFRS 5: Non-current

assets held for sale and discontinued operations as a result of this project.

Several joint projects are in progress to develop new standards on business

combinations, revenue recognition and performance reporting.

The two standard setters are jointly developing a new conceptual framework.

This will eventually replace the current IASB Framework.

However, many preparers and users are becoming concerned about the growing

influence of the FASB. They fear that future international standards will be suitable

for large listed companies only and will be too rigid and detailed for small and

medium-sized entities and those in developing countries.

Chapter 4: The regulatory framework

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 71

The standard-setting process

Developing a new standard

Interpretations of IFRSs

3 The standard-setting process

3.1 Developing a new standard

The development of a new or revised accounting standard involves widespread

consultation and discussion.

A subject is identified as being appropriate for a new or revised standard.

An advisory group is established to give advice to the IASB.

A discussion document is issued by the IASB for public comment.

After receiving comments on the discussion document, the IASB issues an

Exposure Draft (provided it is approved by at least 8 IASB members.) The

Exposure Draft also includes the opinions of any dissenting IASB members, and

the basis for the IASB’s conclusions.

All comments on the Exposure Draft and discussion documents are considered.

An approved IFRS is published (provided it is approved by at least 8 IASB

members.) This will also include the opinions of any dissenting IASB members,

and the basis for the IASB’s conclusions.

Each new or revised standard has a date for implementation.

3.2 Interpretations of IFRSs

An Interpretation of an IFRS might be developed by IFRIC. The purpose of an

Interpretation is to give guidance and clarification on issues where an IFRS is not

clear, and so the interpretation is uncertain.

The need for an Interpretation might become apparent after a new IFRS has been

issued.

IFRIC publishes a draft Interpretation for comment.

After considering the comments received, IFRIC approves an Interpretation.

This interpretation is submitted to the IASB for approval. If approved by at least 8

IASB members, the Interpretation is published.

Paper F7: Financial reporting (International)

72 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Specialised, not-for-profit and public sector entities

Types of entity

Objectives of specialised entities

Accounting standards and specialised entities

4 Specialised, not-for-profit and public sector entities

4.1 Types of entity

Most of this study text is about the financial statements of profit-making entities,

such as limited liability companies.

Other types of entity also prepare and publish financial statements. These entities

include:

Not-for-profit entities: such as charities, clubs and societies. Each of these

organisations is set up for a specific purpose. For example, a charity might be set

up to campaign for the protection of the natural environment or to help the poor.

Public sector entities: these include central government bodies; local

government bodies; and other organisations that operate for the benefit of the

general public, such as state schools and hospitals. A public sector entity is

owned by the state or by the general public.

Many different types of entity could be described under these headings. These

entities are different from limited liability companies, partnerships and sole traders

in one vital respect. They do not primarily exist to make a profit.

In practice, the terms ‘specialised entity’, ‘not-for-profit entity’ and ‘public benefit

entity’ are often used interchangeably.

4.2 Objectives of specialised entities

The main objective of large commercial entities is to maximise their profits in order

to provide a return to their owners (investors) in the form of a dividend. This may

not be their only objective (for example, they may provide employment to the local

community, or aim to operate in a socially responsible way), but it is their main

objective.

The objective of owner-managed businesses (small privately owned entities) is also

to make a profit.

In contrast, the main objective of a specialised entity is to carry out the activities for

which it has been created. Again, this may not be the only objective, because all

entities need some form of income. Many large charities, for example, carry out

trading activities. However, making a profit is not the main aim. In fact, most not-

for-profit entities will aim to break even, rather than to generate a surplus of income

over expenditure.

Chapter 4: The regulatory framework

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 73

4.3 Accounting standards and specialised entities

International accounting standards are designed for profit-making entities.

Whether they are relevant to not-for-profit entities will depend on the way in which

these entities have to report and the information that they have to provide. There is

a great deal of variation from organisation to organisation and from country to

country.

In some countries, charities and public sector bodies are required to follow

accounting standards specifically designed for the purpose (in the UK these are

called Statements of Recommended Practice.) Alternatively, the form and content of

financial statements and the accounting treatments to be followed may be

prescribed by law. IASs and IFRSs are probably largely irrelevant for these entities.

Some not-for-profit entities may be able to draw up financial statements in any form

that its members or officers wish. Many not-for-profit entities prepare financial

statements on a cash basis, rather than on an accruals basis. Public sector bodies

may also use ‘cash accounting’. (This was the case in the UK until fairly recently.)

IASs and IFRSs require accruals accounting.

In some countries, public sector bodies and many charities are increasingly expected

to apply commercial-style accounting practices. Even for those entities that are not

formally required to adopt them, IASs and IFRSs are a useful source of information

on current best practice.

Paper F7: Financial reporting (International)

74 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP