ACCA F6 FA09 Study Text 2010

Подождите немного. Документ загружается.

Chapter 20: Overseas aspects of corporation tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 365

Treatment of intra-group transactions with overseas subsidiaries

An explanation of the problem

The transfer pricing provisions

4 Treatment of intra-group transactions with overseas

subsidiaries

4.1 An explanation of the problem

As a consequence of the close relationship between group companies, intra-group

transactions can be arranged at any price the companies choose, or even free of

charge. As a result, the pricing of intra-group transactions can result in group profits

being transferred from one company in the group to another.

The ability to manipulate the pricing of transactions provides groups with the

possibility of valuable tax planning opportunities (e.g. maximising use of losses

within a group and/or ensuring that profits are taxed at the lowest rate of tax

available within the group).

Such tactics could be particularly useful in international groups, for example

between a UK group company and an overseas group company. By selling to an

overseas subsidiary at a price below market price, or buying goods from an

overseas subsidiary at a price above the market price, profits can be shifted out of

the UK corporation tax charge and advantage taken of tax rates abroad which may

be lower.

However, anti-avoidance legislation (the transfer pricing provisions) has been

introduced to prevent the manipulation of profits in this way.

4.2 The transfer pricing provisions

The transfer pricing rules apply to transactions between 50% group companies. A

50% group exists where one company controls another company or they are both

under common control. (Essentially control exists when there is an interest in the

equity shares of the company in excess of 50%. A more detailed definition of control

is explained in a later chapter.)

For the purposes of the examination, the rules only apply to large groups of

companies. A large group is defined as a group with:

at least 250 employees, and

either revenue of at least €50 million or total assets of at least €43 million.

For corporation tax purposes, groups are responsible for applying the arm’s length

principle to their intra-group transactions.

Paper F6 (UK): Taxation FA2009

366 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

An arm’s length price is the price that would be charged in a normal commercial

transaction between two independent parties.

Group companies falling within the rules are allowed to deal with intra-group

transactions in one of two ways:

(1) charge and account for intra-group transactions on an arm’s length basis in

their financial accounts, or

(2) charge and account for the transactions at any desired price, then make an

adjustment in the UK company’s adjustment of profit computation to reflect

all intra-group transactions with that company at an arm’s length price.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 367

Paper F6 (UK)

Taxation FA2009

CHAPTER

21

Group corporation tax

Contents

1 Associated companies

2 Group loss relief

3 Group chargeable gain provisions

Paper F6 (UK): Taxation FA2009

368 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Associated companies

Introduction

Definition of an associated company

Consequences of being associated

1 Associated companies

1.1 Introduction

A group of companies is not treated as a single entity for the purpose of corporation

tax. The consolidated accounts for the group are irrelevant for tax purposes.

Instead, for corporation tax purposes, each company within a group is taxed

separately in its own right.

However, in calculating the corporation tax of each company, the tax legislation

allows the group to deal with certain items on a group wide basis as if it were a

single entity.

When dealing with an examination question involving a group, your starting point

should be to determine the number of associated companies.

1.2 Definition of an associated company

Companies are associated if:

one company is under the control of another, or

two or more companies are under the common control of another person, which

could be another company, an individual or a partnership.

Control in this context means an interest of more than 50% in:

the share capital, or

the voting rights, or

the rights to the distributable profits, or

the net assets on a winding up of the company.

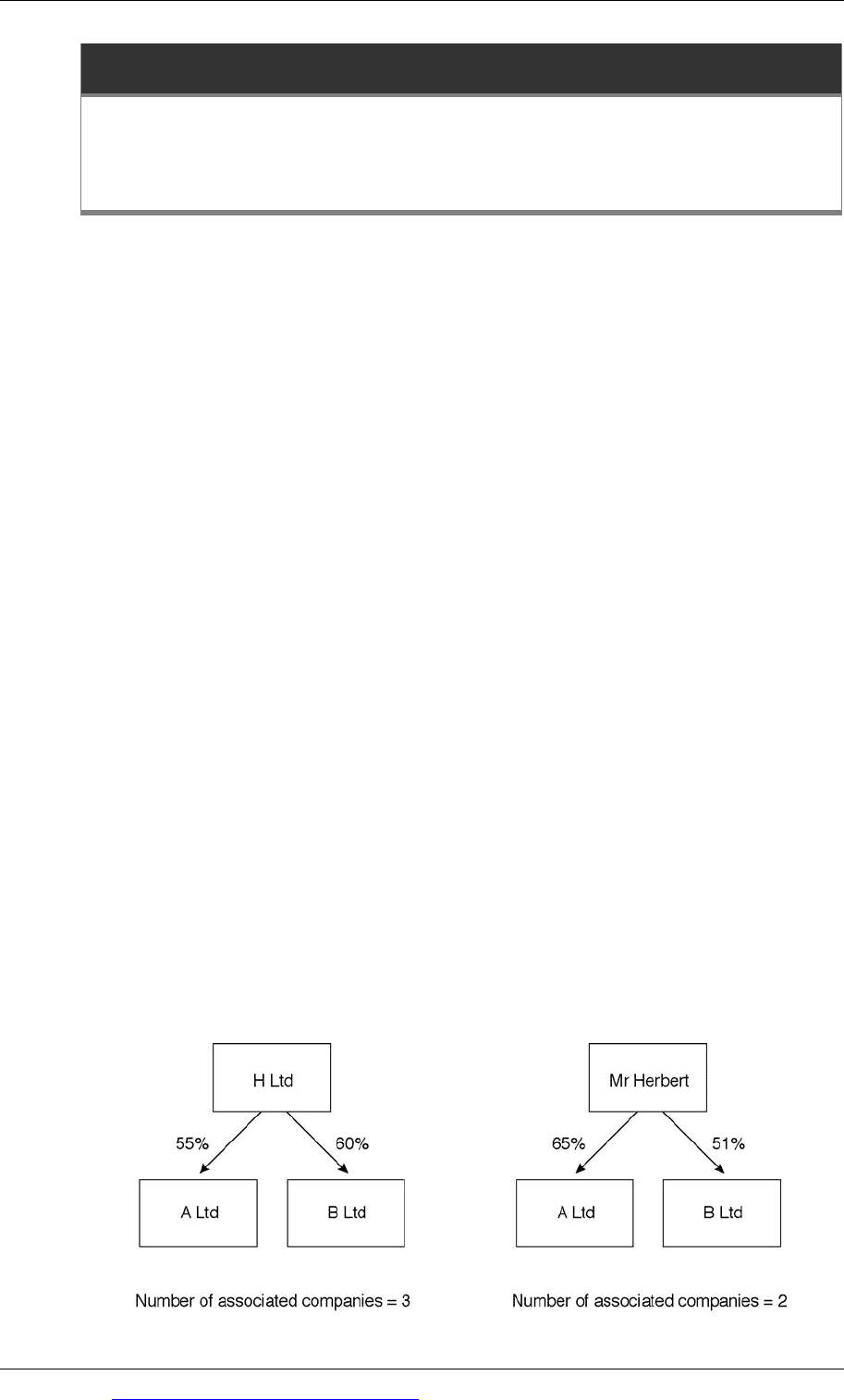

For example:

Chapter 21: Group corporation tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 369

Where a group relationship exists, the companies are under the common control of

the holding company and therefore they are associated for corporation tax

purposes.

Companies within a group are associated if the company has been part of the group

relationship at any time in the CAP. The definition of associated company therefore

includes companies which have been acquired, or disposed of, part way through the

CAP. These joiners and leavers are deemed to be associated for the entire CAP.

The definition of associated company also includes overseas companies, but it

excludes dormant companies (i.e. non-trading companies).

1.3 Consequences of being associated

The consequences of being associated companies are as follows:

When calculating profits for each company in the group, any intra-group

dividends are ignored entirely. They are not treated as franked investment

income (FII).

For the purpose of establishing the rate of corporation tax applicable to each

company in the group, the statutory limits must be divided by the number of

associated companies.

Example

For the year ended 31 March 2010 I Ltd had PCTCT of £400,000 and did not receive

any dividends. It has three associated companies.

Required

Calculate the corporation tax liability of I Ltd for the year ended 31 March 2010.

Answer

I Ltd – corporation tax liability computation – y/e 31 March 2010

£

PCTCT

400,000

FII Nil

Profits

400,000

Small companies rate

Lower limit

Upper limit

300,000 ÷ 4

1,500,000

÷ 4

75,000

375,000

Decision: Full rate of 28% applies (since profits are above £375,000)

Corporation tax liability

£400,000 × 28%

£112,000

Note

I Ltd has three associated companies, therefore the statutory limits must be divided

by four (i.e. I Ltd plus 3).

Paper F6 (UK): Taxation FA2009

370 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Group loss relief

Definition of a 75% group for group loss relief purposes

An outline of how group loss relief works

The rules for group relief from the surrendering company’s point of view

The rules for group relief from the recipient company’s point of view

Tax planning and group loss relief

2 Group loss relief

2.1 Definition of a 75% group for group loss relief purposes

Where one company owns, directly or indirectly, at least a 75% interest in the

ordinary share capital of another company, group loss relief (often referred to

simply as group relief) may be available.

For group relief to be available, the company must also own at least 75% of the

rights to the distributable profits and the net assets on a winding up of the

company. However, for the examination, the ownership of the shares is the key

deciding factor.

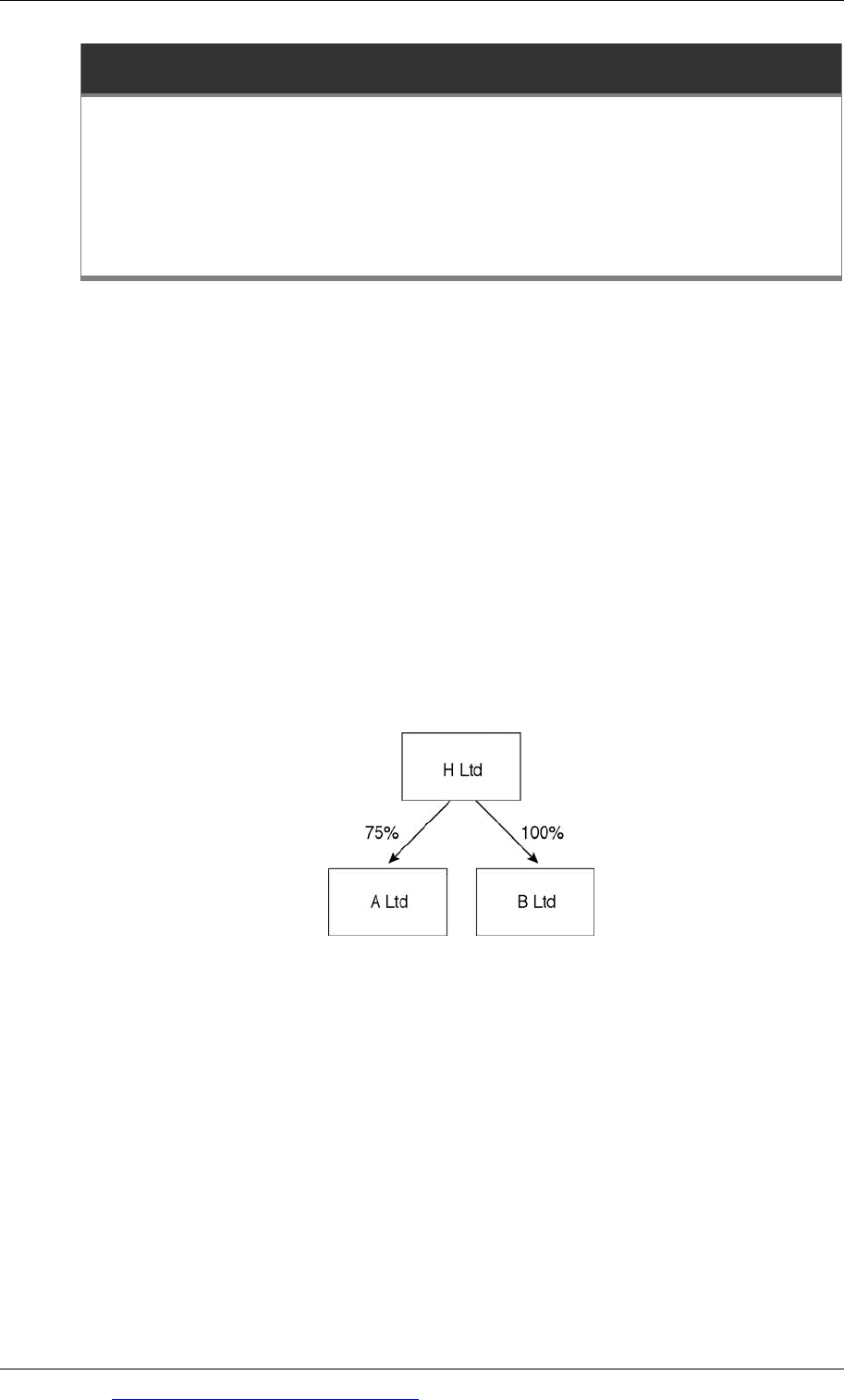

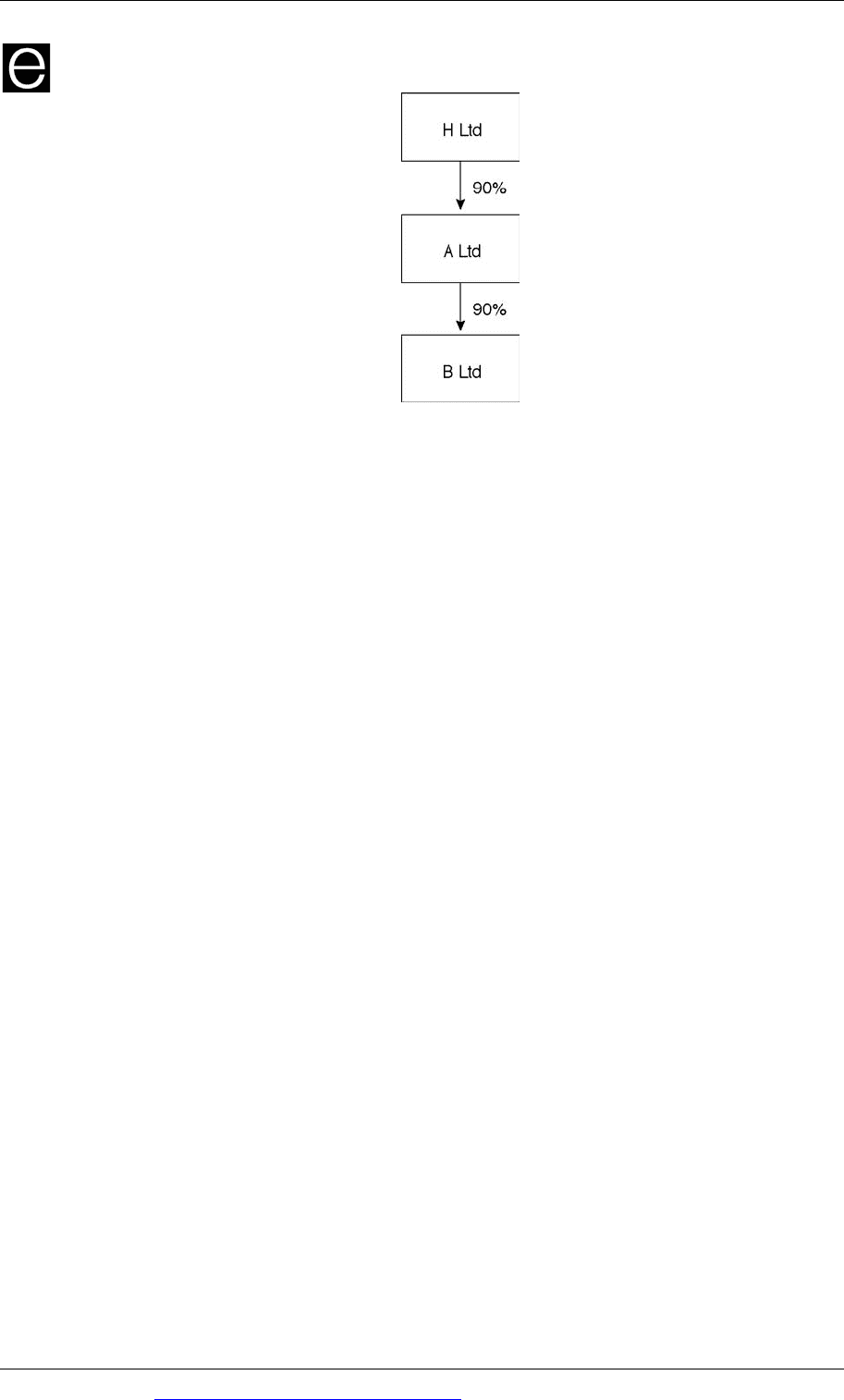

Directly-owned 75% subsidiaries will be part of a loss relief group. For example:

Both A Ltd and B Ltd are directly owned 75% subsidiaries of H Ltd for group loss

purposes.

Indirect subsidiaries (sub-subsidiaries)

An indirect subsidiary is the term used to refer to the situation where the holding

company of a group owns shares in a subsidiary via another company (often

referred to as a sub-subsidiary).

Chapter 21: Group corporation tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 371

Example

In this situation, the sub-subsidiary (B Ltd) can only be part of the holding

company’s loss relief group if the holding company (H Ltd) has an effective interest

of at least 75% in the sub-subsidiary (B Ltd).

The size of the effective interest is calculated by multiplying together:

the percentage of the subsidiary owned by the holding company, and

the percentage of the sub-subsidiary owned by the subsidiary.

In the above example, the effective interest of H Ltd in the sub-subsidiary B Ltd is

81% (= 90% × 90%). Both A Ltd and B Ltd are therefore 75% subsidiaries of H Ltd

for group loss relief purposes.

The composition of a loss relief group

To determine the composition of a loss relief group, both UK and overseas

companies in the group are considered. For example, an overseas holding company

with two UK 75% subsidiaries would form a loss relief group.

However, under the group loss relief provisions, it is only possible to move losses

between the UK companies in the group.

A company can be the member of more than one loss relief group.

Paper F6 (UK): Taxation FA2009

372 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

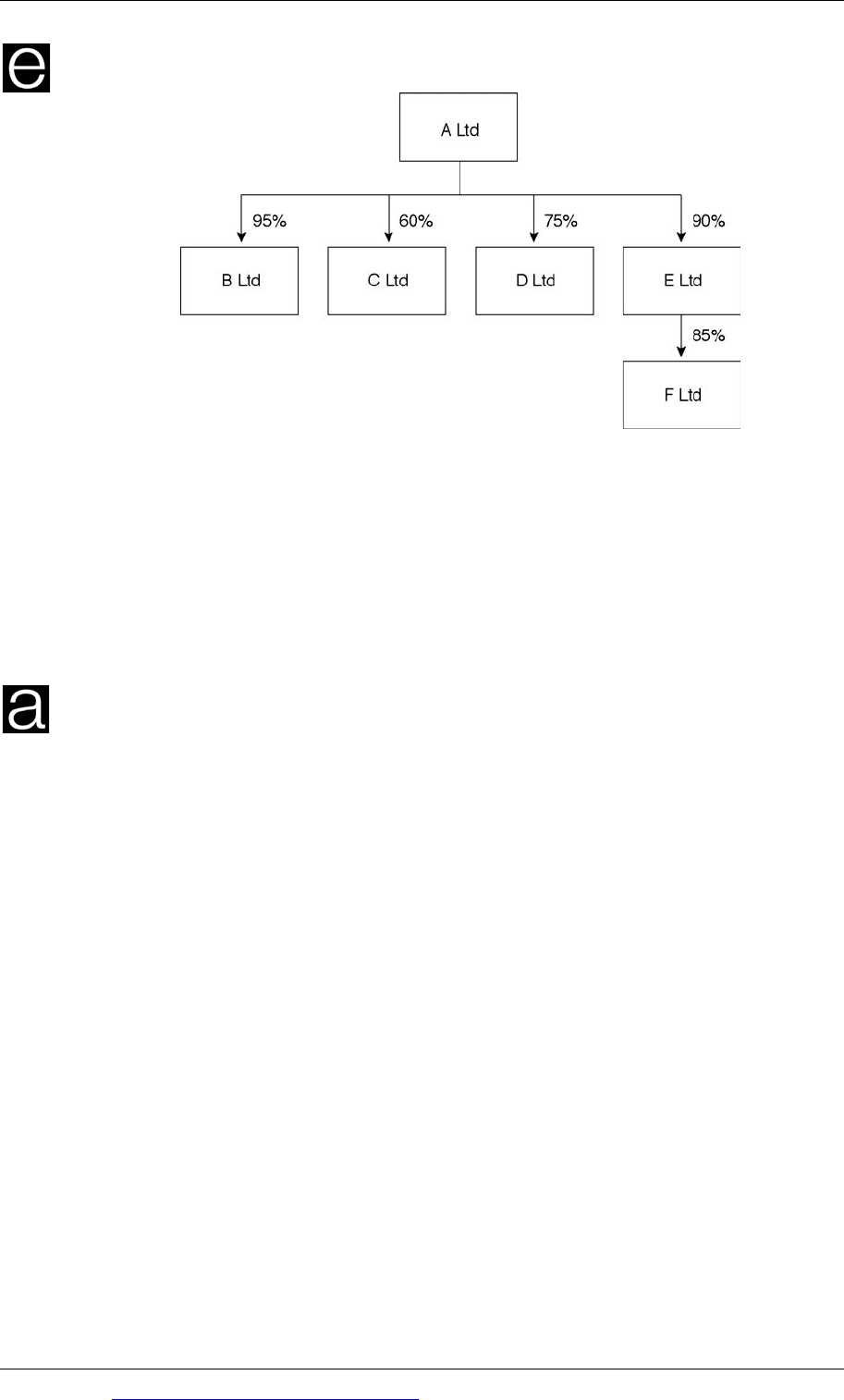

Example

Required

Calculate the number of associated companies and state which companies form a

loss relief group making each of the following alternative assumptions:

(a) All companies are UK companies

(b) A Ltd is an overseas company.

Answer

(a) Assuming all companies are UK companies

Number of associated companies = 6

All the companies are associated as A Ltd has an interest of more than 50% in

each.

Loss relief group = A Ltd, B Ltd, D Ltd, E Ltd and F Ltd

Notes

(1) C Ltd is not included as A Ltd owns less than 75%.

(2) F Ltd is included as A Ltd has an effective interest of at least 75% (90% ×

85% = 76.5%).

(b) Assuming A Ltd is an overseas company:

The answer is the same as above in (a):

Overseas companies are associates; therefore there are still 6 associated

companies.

The composition of a loss relief group includes overseas companies; the

group is therefore defined as above.

However, group losses may only move between the UK-resident companies

(i.e. between B Ltd, D Ltd, E Ltd and F Ltd).

Chapter 21: Group corporation tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 373

2.2 An outline of how group loss relief works

The group relief provisions allow losses to be transferred in any direction between

UK companies within a loss relief group.

The loss relief is deducted from the PCTCT of the recipient company and therefore

reduces its corporation tax liability.

Group relief is not automatic. It must be claimed within two years of the end of the

CAP of the company receiving the group relief.

2.3 The rules for group relief from the surrendering company’s point of view

The following losses can be surrendered:

trading losses

unrelieved UK property business losses (i.e. losses left unrelieved after making a

the claim against total profits for the current period)

unrelieved Gift Aid donations.

It is important to note that capital losses cannot be surrendered (but see below).

Only current period losses can be surrendered. It is not possible to surrender losses

brought forward from a previous CAP or carried back from a later CAP.

The surrendering company can give away any amount of its current period losses to

one or several other group companies.

The surrendering company can utilise its own losses against its own profits (for

example, with a s393A claim) before surrender, if it wishes to do so. However, it is

not obliged to utilise its own losses first. It can transfer all its losses, and pay tax

itself, if it wishes to do so for tax planning reasons or other commercial reasons.

However, it cannot surrender all its losses if the recipient company can not utilise

them all against its own available profits.

2.4 The rules for group relief from the recipient company’s point of view

The recipient company can only accept losses up to the amount of its available

profits.

Available profits are defined as PCTCT after deducting the following amounts

relating to the recipient company:

any trading losses brought forward

a current period loss relief claim under s393A (see below), and

current period Gift Aid donations.

Paper F6 (UK): Taxation FA2009

374 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

In calculating the available profits, a current period s393A claim must be deducted

even if a claim is not actually made. However, there is no requirement to take

account of a carry back claim under s393A.

Losses can only be matched against profits of a corresponding accounting period.

(i.e. the period when both the surrendering and recipient company were part of the

same group).

If both companies have the same CAPs and are part of the group for the whole CAP

the position is straightforward. The maximum group relief claim = Lower of:

the loss of the surrendering company, or

the available profits of the recipient company.

Year ends that are not coterminous

Where the two companies have non-coterminous year ends (i.e. they do not have

the same year end dates) or where a company joins or leaves a group during the

CAP, the maximum group relief available is calculated by time-apportionment of:

the surrendering company’s losses, and

the recipient company’s available profits.

In effect, this means that the available profits are matched with the available losses

in the common CAPs.

Example

G Ltd owns a 100% subsidiary, K Ltd. In the year ended 30 September 2009 the two

companies had the following results:

G Ltd K Ltd

£ £

Trading profit / (loss) (125,000) 28,000

Interest income

20,000 20,000

Net chargeable gain

Nil 135,000

Gift Aid payment

(2,000) (5,000)

Trading loss brought forward

(10,000) (50,000)

Required

Calculate the maximum group relief surrender for the year ended 30 September

2009.