Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

1. Amount of the expense (entertainment and gifts),

2. Time and place (entertainment) or date and description (gifts),

3. Business purpose (entertainment and gifts), and

4. Business relationship (entertainment and gifts)

If any of the above information is not available, the IRS will disallow the deduction for

entertainment expenses or gifts.

SECTION 4.10

SCHEDULE C

A taxpayer who operates a business or practices a profession as a sole proprietorship must

file a tax return reporting his or her taxable income or loss from the activity. Taxable

income from a business or profession is repor ted on either Schedule C-EZ (shor t form),

Schedule C (long form), or Schedule F (a specialized version of Schedule C for farmers

and ranchers). When a taxpayer has more than one business or profession, he or she

must complete a separate Schedule C for each business or profession.

EXAMPLE Georgia and Chuck are married. Chuck runs a small retail pet shop

and practices as a CPA. Georgia is a self-employed dentist. Georgia

and Chuck must file three separate Schedule Cs, one for the pet shop,

one for the CPA practice, and one for the dental practice. N

Schedule C-EZ

Taxpayers must file Schedule C unless they qualify to file Schedule C-EZ. To use the short

form, Schedule C-EZ, the taxpayer must meet the following requirements:

1. Business expenses must be $5,000 or less,

2. There must be no inventory during the year,

3. The business must not have had a net loss for the year,

Self-Study Problem 4.9

Carol, an employee of Jacaranda, Inc., makes the following business gifts

during 2010:

Donee Amount Deduction

1. Mr. Jones (a client) $ 20 $ _____________

2. Mr. Brown (a client) 32 _____________

3. Mrs. Green (a client) 15 _____________

4. Mr. Green (the nonclient husban d of Mrs. Green) 18 _____________

5. Ms. Gray (Carol’s supervisor) 45 _____________

6. Mr. Edwards (a client receiving a display rack

with Carol’s company name on it)

75 _____________

7. Various customers (receiving ball point pens with

the company name on them)

140 _____________

Total Business Gift Deduction

$

Calculate Carol’s allowed deduction for each busine ss gift and her total

allowed deduction (before the 2 percent of adjusted gross income limitation).

Section 4.10

Schedule C 4-19

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

4. The taxpayer must have only one business as a sole proprietor,

5. The business must have had no employees during the year,

6. The taxpayer must not be required to complete Form 4562 to repor t depreciation,

7. The business must not include a home office deduction,

8. The business must not have had disallowed passive losses in a prior year(s), and

9. The business must use the cash method of accounting.

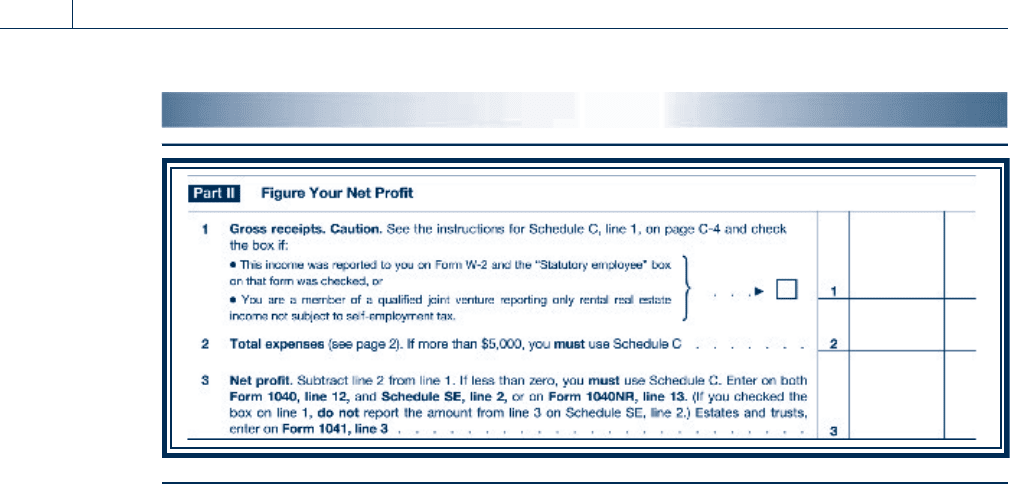

Schedule C-EZ of Form 1040 is straightforward. It is one page long and consists of three

parts. The three parts are General Information (Part I), Net Profit (Part II), and Vehicle

Information (Part III). The general inform ation section includes information such as the

business n ame and address. The net profit section of Schedule C-EZ (see Figure 4.1) is

only three lines long: gross receipts (line 1), total expenses (line 2), and net profit (line 3).

Taxpayers claiming car or truck expenses must also complete Part III of Schedule C-EZ,

giving information about the vehicle used in the business or profession.

Schedule C

Schedule C is required for more complex businesses and requires a taxpayer to provide

more information. The first section (lines A to H) of Schedule C requires disclosure of

basic information such as the business name and l ocation, the accounting m ethod (cash,

accrual, or other, as covered in Chapter 7), material participation in the business (for pas-

sive activity loss classification purposes), and whether the business was started or acquired

during the year.

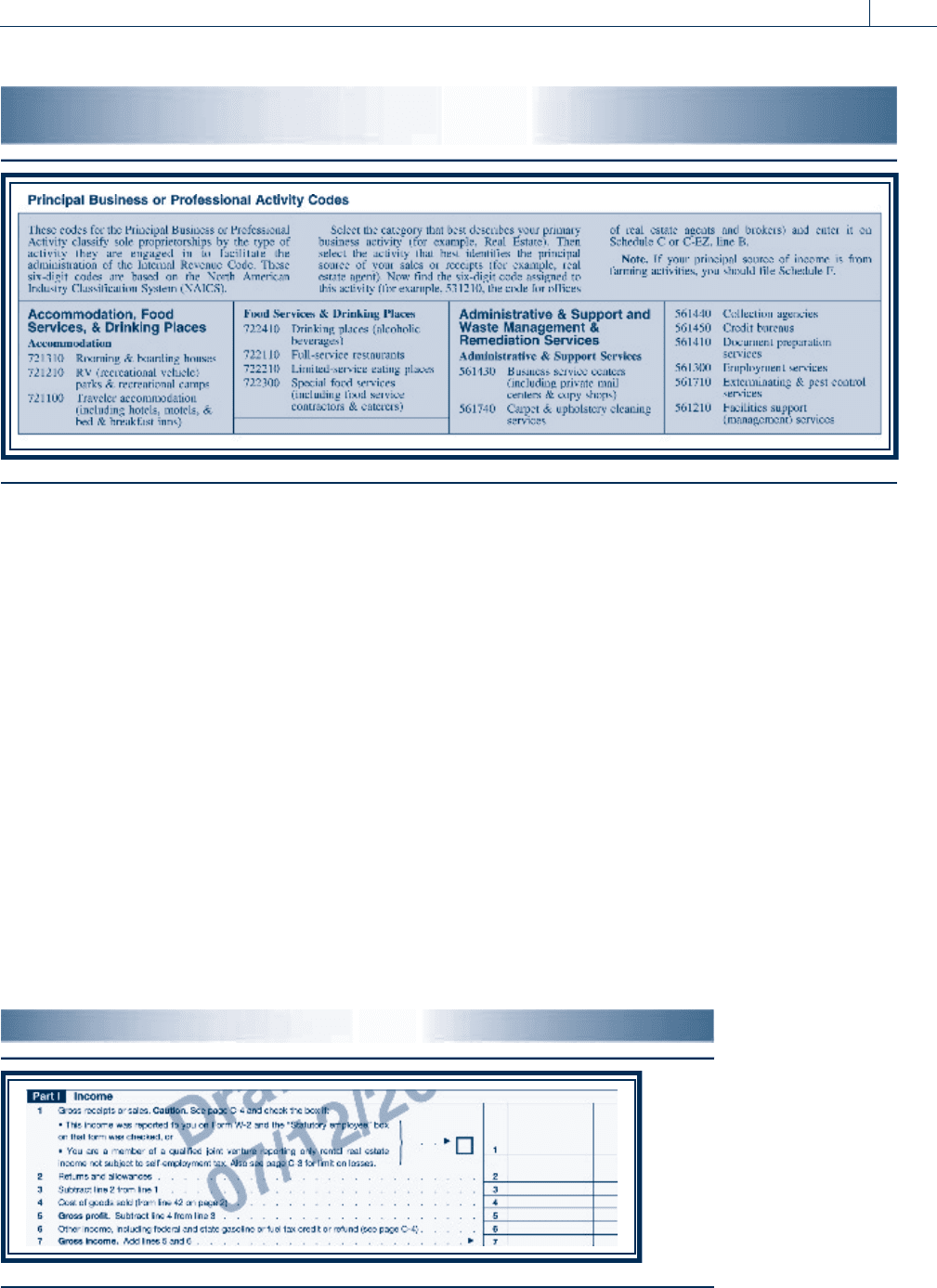

Both Schedule C and Schedule C-EZ ask that the taxpayer supply a principal business or

professional activity code (see Figure 4.2). These codes are used to classify sole proprietor-

ships by the type of business activity. For example, a full-service restaurant is code 722110,

as shown on the next page.

Schedule C Income (Part I)

Part I of Schedule C (Figure 4.3) contains the calculation of the taxpayer’s gross income from

the business or profession. The calculation starts with gross receipts and sales (line 1).

Returns and allowances (line 2) and cost of goods sold (line 4) are subtracted to arrive at

the gross profit from the activity. Other related income from the business (line 6) is added

to the gross profit to produce the Schedule C gross income (line 7).

FIGURE 4.1 SCHEDULE C-EZ PART II

4-20 Chapter 4

Business Income and Expenses, Part II

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Schedule C Expenses (Part II)

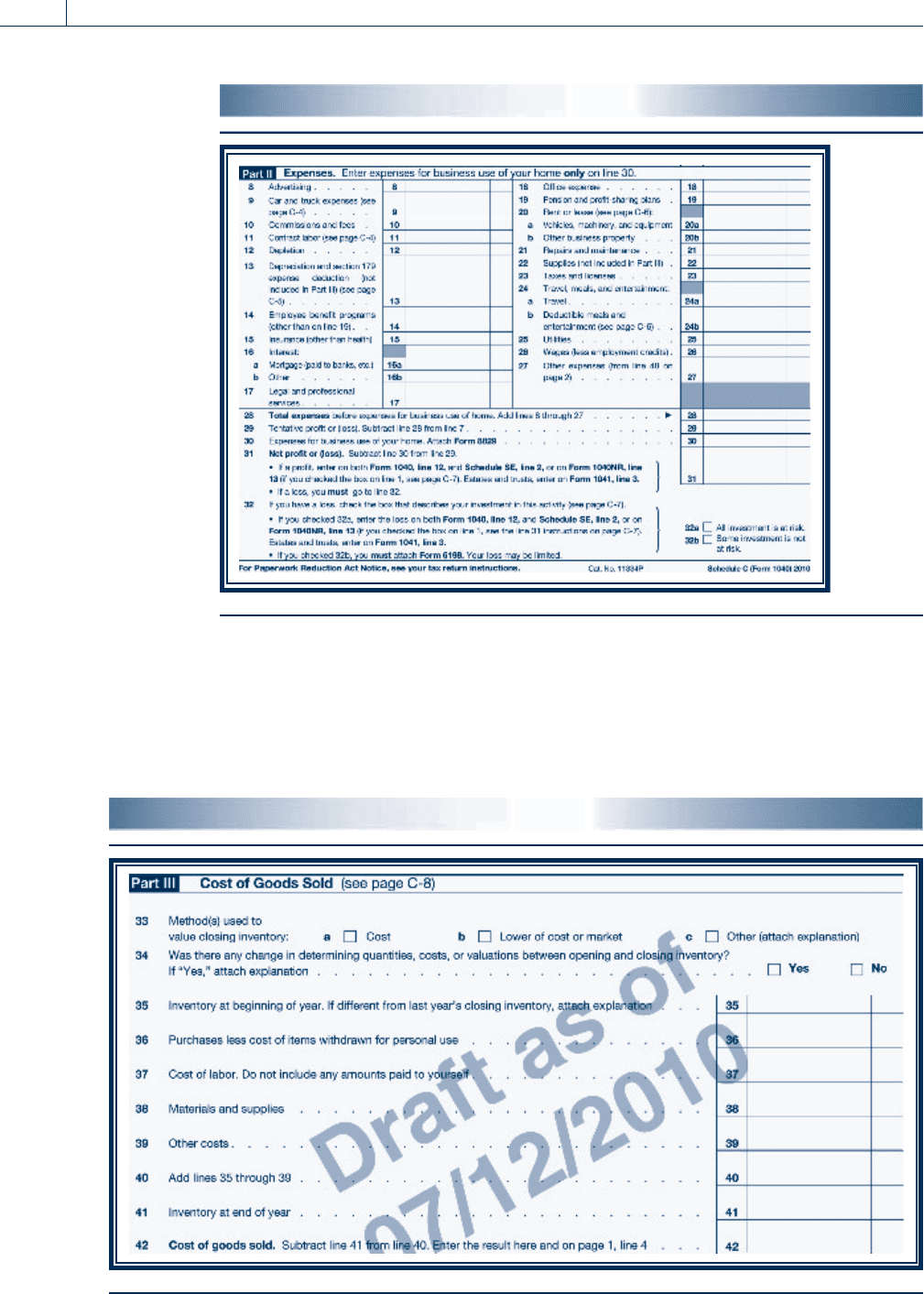

The taxpayer reports the expenses from his or her business or profession in Part II of

Schedule C (Figure 4.4). Expenses such as adver tising, insurance, interest, rent, travel,

transportation, wages, and utilities are reported on lines 8 through 27. Some of these

expenses such as depreciation may requ ire additional supporting information from another

schedule. The expenses are totaled on line 28 and subtracted from gross income (line 7) to

arrive at the tentative profit from the activity. An expense for business use of a taxpayer’s

home (Section 4.4 of this text) is computed on Form 8829. The deductible portion of home

office expenses is entered on line 30 and subtracted from tentative profit, resulting in the

net profit or loss (line 31) from the activity.

Schedule C Cost of Goods Sold (Part III)

The calculation of cost of goods sold is reported in Part III (Figure 4.5) of Schedule C. In

Part III lines 33 and 34, taxpayers must answer questions about the methods used to calcu-

late inventory. Cost of goods sold is equal to the beginning inventory (line 35) plus purchases

(line 36), labor (line 37), materials and supplies (line 38), and other costs (line 39) less ending

inventory (line 41). Please see Section 3.4 for a more detailed discussion of inventories.

FIGURE 4.3 SCHEDULE C INCOME (PART I)

FIGURE 4.2 PRINCIPAL BUSINESS OR PROFESSIONAL

ACTIVITY CODES EXCERPT

Section 4.10

Schedule C 4-21

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

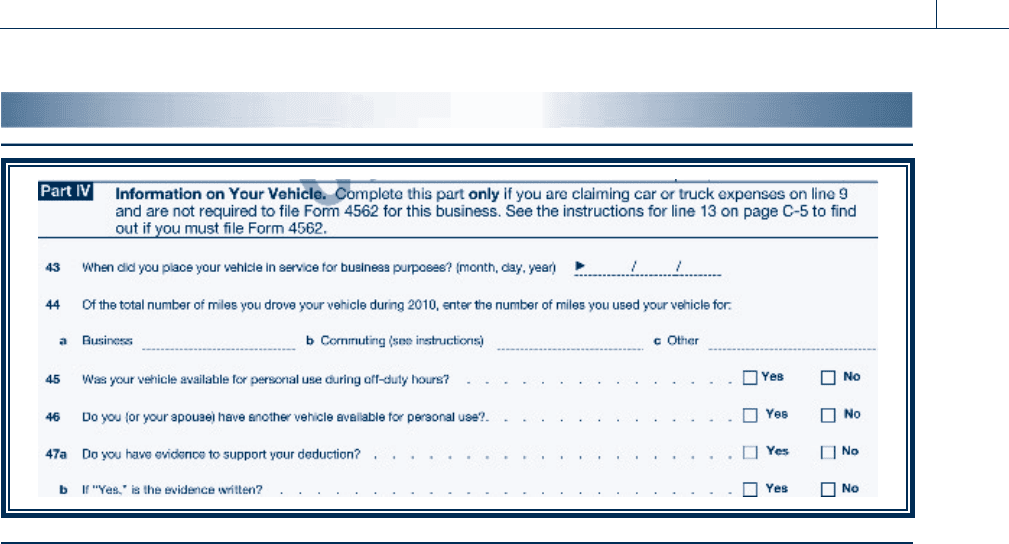

Schedule C Vehicle Information (Part IV)

If a taxpayer uses a car or truck in his or her business or professi on, then Part IV of Sched-

ule C (Figure 4.6) must be completed to provide the IRS with supplemental vehicle infor-

mation. In Part IV, a taxpayer should provide the date the vehicle was placed in business

FIGURE 4.5 COST OF GOODS SOLD (PART III)

FIGURE 4.4 SCHEDULE C EXPENSES (PART II)

4-22 Chapter 4

Business Income and Expenses, Part II

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

service (line 43), the business miles driven (line 44a), the commuting miles driven (line

44b), and other miles driven (line 44c). On lines 45 to 47 of Part IV, taxpayers must answer

questions relevant to obtaining a deduction for business use of a vehicle.

Schedule C Other Expenses (Part V)

In the expense section of Schedule C (Part II), line 27 contains an entry for other miscel-

laneous expenses. These o ther expenses must be itemized in Part V of Schedule C and

would include deductible items which do not have specific lines already assigned in the

expenses section (Part II). Expenses for business gifts, education, professional dues, and

consulting fees are commonly listed.

Gambling Winnings

Gambling winnings are not reported on Schedule C unless the taxpayer is a professional

gambler. Net casual gambling winnings are reported as ‘‘other income’’ on Form 1040.

Gambling losses, limited to the amount of winnings, are deducted as a miscellaneous item-

ized deduction (see Chapter 5).

Self-Employment Tax

Self-employed taxpayers, sole proprietors, and independent contractors with net earnings of

$400 or more, many of whom report income on Schedule C, must pay a self-employment

tax calculated on Schedule SE with their Form 1040. For new business owners, the self-

employment tax may come as a particularly unpleasant and costly surprise if they are

not aware of its existence.

The self-employment tax is made up of two taxes, the Social Security tax, which is meant

to fund old age and disability insurance payments, and the Medicare tax. For 2010, the Social

Security tax rate of 12.4 percent applies to the first $106,800 of net self-employment income,

while the Medicare tax rate of 2.9 percent applies to all net self-employment income, with no

ceiling. Half of the self-employment tax is allowed as a deduction on the front page of Form

1040 in arriving at adjusted gross income. A similar tax is levied on employees partly through

payroll withholding and partly through employer contributions, so it is not actually paid with

Form 1040 as it is for self-employed taxpayers. Both self-employed and employee Social

Security and Medicare taxes are covered in detail in Chapter 9.

FIGURE 4.6 VEHICLE INFORMATION (PART IV)

Section 4.10

Schedule C 4-23

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Self-employed taxpayers are subject to higher risk of IRS audit than wage earners

and must be able to substantiate income and expenses reported on Schedule C if

audited. A good accounting and record-keeping system is recommended for all

self-employed taxpayers, no matter how small the business. The high audit rate is

due to government reports showing high levels of underreporting of net business

income among sole proprietors.

Manufacturers’ Deduction

In 2010, taxpayers are allowed a manufacturers’ deduction calculated as 9 percent of the

lesser of (1) qualified production income or (2) taxable (or adjusted gross) income. How-

ever, the maximum deduction cannot exceed 50 percent of the employer’s W-2 wage

expense. The deduction is available to individuals, partnerships, S corporations, C corpo-

rations, cooperatives, estates, and trusts.

Qualified production receipts do not include proceeds from the sale of food and bever-

ages prepared at a retail establishment.

EXAMPLE Ian, a calendar year taxpayer, owns and operates a shop that manu-

factures racing headers for classic Mustangs. He has AGI of $400,000

and qualified production income of $420,000. If he pays $225,000 in

W-2 wages to his employees, lan’s manufacturers’ deduction for 2010

is $36,000 [9 percent (lesser of $400,000 or $420,000), not to exceed

50 percent of $225,000]. N

Self-Study Problem 4.10

Teri Kataoka is self-employed as a professional golf teacher. She uses the

cash method of accounting and her Social Security number is 466-47-8833.

Her principal business code is 812990. Teri’s business is located at 1234

Golfcrest Dr., Palm Springs, CA 92262. During 2010, Teri had the following

income and expenses:

Fees from golf lessons $ 39,250

Expenses:

Car mileage (6,056 business miles) 3,028

Business liability insurance 450

Life insurance on Teri ($250,000) 325

Office expense 640

Rent on office space 2,700

City busi ness license 250

Travel expense 3,100

Meals and entertainment 1,790

Utilities 975

Teri bought her car on January 1, 2010. She used it to commute 3,000 miles

and she drove 6,000 miles for nonbusiness purposes.

Complete Schedule C on pages 4-35 and 4-36 for Teri showing her net

income from self-employment.

4-24 Chapter 4

Business Income and Expenses, Part II

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 4.11

MOVING EXPENSES

Congress, recognizing the importance of having a mobile work force, felt taxpayers should

not be penalized if forced to move to cities where better employment opportunities exist.

Thus, the tax law provides a deduction for moving expenses to help relieve taxpayers of a

portion of the financial burden of moving from one job location to another. Moving

expenses are deductible in arriving at adjusted gross income.

To qualify fo r the moving expense deduction, three general tests must be m et. These

tests are:

1. The taxpayer must change job sites. The taxpayer does not have to change employers.

A job transfer with the same employer meets this test.

2. The taxpayer must move a certain minimum distance. The distance from the tax-

payer’s former residence to the new job location must be at least 50 miles or more

than the distance from the former residence to the former job location.

3. The taxpayer must remain at the new job location for a certain period of time. Gen-

erally, employees must work at least 39 weeks at the new job location during the

12 months following the move. Taxpayers who are self-employed must work at least

78 weeks at the new location during the 24 months after the move.

Taxpayers who are in the military or employees who are involuntarily transfe rred are

still allowed the moving expense deduction even if the time or distance test is not met.

EXAMPLE Daniel works in San Diego and lives in Del Mar, a distance of

20 miles. He accepts a new position with his current firm in Rancho

Mark (age 44) and Mary (age 41) Mower are your tax clients. They have two

children, Matthew (age 20) and Mindy (age 17), who live at home. Mindy is

a senior in high school and Matthew commutes to a local college where he

is studyin g soil management. Mark owns and operates a successful lawn

maintenance and landscaping business. He has six employees and three pick-

up trucks used for transportation to the job sites. The business has a credit

card in its name for use by the employees and Mark, who fills the trucks

with gas almost daily. Mark gave a business credit card to Mary, Matthew,

and Mindy and told them to use it to buy gas for their automobiles used for

shopping, going to school, and short trips. In the current year, his wife and

children put $5,210 of gasoline in their automobiles using the business

credit card. Mark is adamant that the $5,210 be deducted on his Schedule C.

He feels the amount is small compared to the business gas purchases of

approximately $28,000. Mark says the amounts charged are spread through-

out the credit card statements and would be very difficult for the IRS to

detect on audit. Would you sign the Paid Preparer’s declaration (see exam-

ple above) on this return? Why or why not?

Section 4.11

Moving Expenses 4-25

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Cucamonga and moves there. Rancho Cucamonga is 110 miles from

Del Mar. Daniel meets the distance test because the distance from

his new place of employment, Rancho Cucamonga, to his former

residence, Del Mar (110 miles), less the distance from his former

place of employment to his former residence, Del Mar (20 miles), is

at least 50 miles. N

Qualified moving expenses fall into two categories. These two categories are:

1. Moving household goods and personal effects.

2. Traveling from the former residence to the new place of residence. For purposes of

the moving expense deduction, traveling includes lodging, but not meals, for the tax-

payer and household members.

Moving expenses must be reasonable to be deductible. For example, traveling expenses

of going through Seattle on a move from Los Angeles to Miami would not be allowed.

Qualified moving expenses reimbursed by an employer are not reported as part of the

gross income of the employee. However, nonqualified moving expense reimbursements

(e.g., employer reimbursement for meals during a move) are included in the gross income

of an employee.

EXAMPLE John, an employee of Pine Corporation, is hired by Oak Corporation.

His new job requires that he move from Denver to Houston. During

the move, John incurs the following expenses:

Cost of moving furniture $3,6 00

Transportation 500

Meals 200

Lodging

300

Total

$4,600

John’s total qualified moving expense is $4,400 ($3,600 þ $500 þ

$300). N

Self-Study Problem 4.11

During May 2010, Maureen Motsinger is transferred to a new job by her

employer. The transfer requires her to move from Phoenix to New York. The

distance from her former residence to her new job location is 3,030 miles,

and the distance from her former residence to her former job location is

20 miles. She incurs packing and moving expenses of $4,100. The cost of her

lodging during the move is $650. Also, she spends $200 for meals during

the move. She drives the 3,030 miles to New Y ork in her automobile (the

moving expense mileage rate for 2010 is 16.5 cents per mile). After her

arrival in New York, Maureen’s employer reimburses her $5,250 for the mov-

ing expenses. Calculate Maureen’s moving expense deduction using Form

3903 on page 4-27.

4-26 Chapter 4

Business Income and Expenses, Part II

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 4.11

Moving Expenses 4-27

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

4-28 Chapter 4

Business Income and Expenses, Part II

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.