Citibank: basic of corporate finance

Подождите немного. Документ загружается.

9-40 FIXED INCOME SECURITIES

v-1.1 v.05/13/94

p.01/14/00

Please complete Practice Exercise 9.4, which will give your experience with calculating

the duration of a bond. When you have checked your answers, continue on to the Unit

Summary that follows.

www.LisAri.com

FIXED INCOME SECURITIES 9-41

v.05/13/94 v-1.1

p.01/14/00

PRACTICE EXERCISE 9.4

Directions: Calculate the correct answer(s) for each question. Check your solutions

with the Answer Key on the next page.

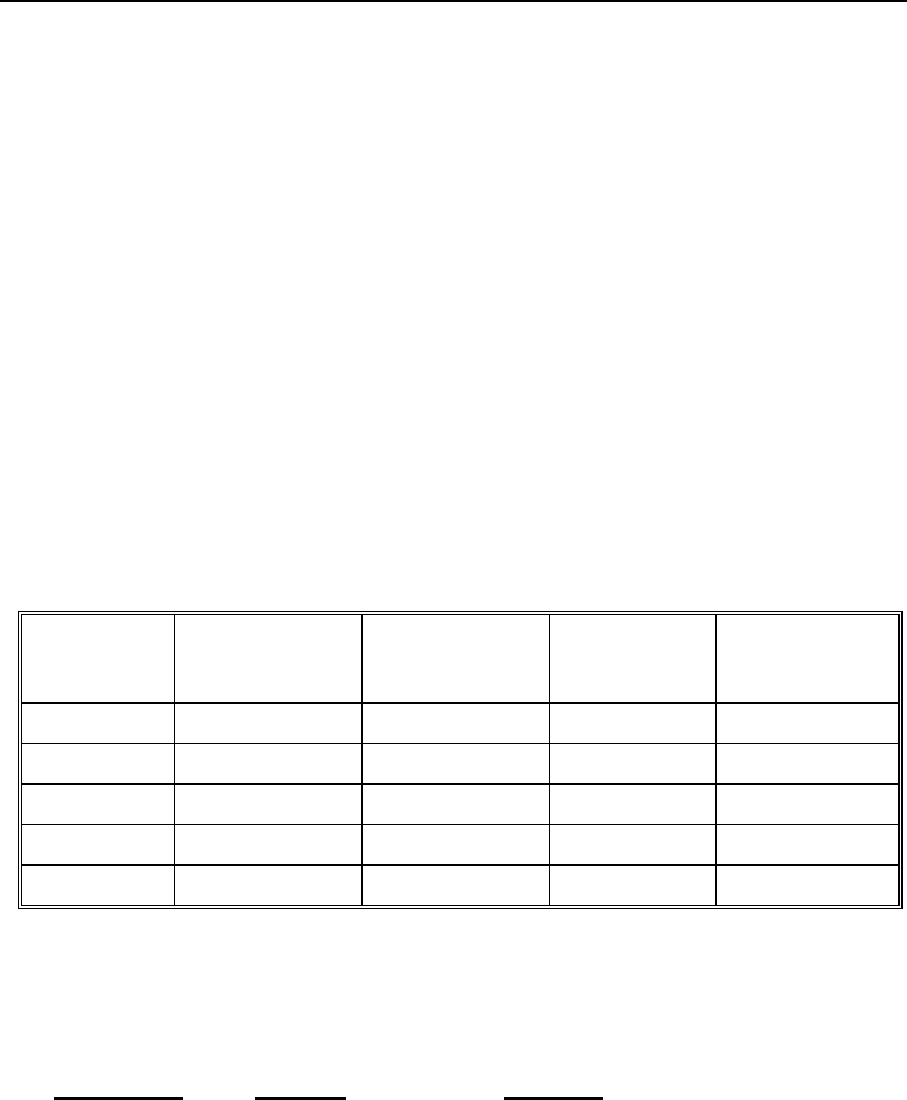

12. A 2-year Treasury note with a coupon rate of 6.5% has a percentage issue price of

98.50. What is the duration of the instrument?

Duration = _____________ years

Use this table to help with your calculation.

Price: _________ BEY: _________

Coupon: _________ Discount Rate: _________

Maturity: _________

Time Cash Flow

Present

Value at Semi-

annual Rate

Present

Value /

Bond Price

Time-

weighted

Value

______________ _____________ ______________

TOTAL

13. What is the duration of the following portfolio?

Percentage

of Portfolio Security Duration

42.5% 2-year notes 1.8654

37.8% 5-year notes 4.7333

19.7% 10-year bonds 9.6655

www.LisAri.com

9-42 FIXED INCOME SECURITIES

v-1.1 v.05/13/94

p.01/14/00

ANSWER KEY

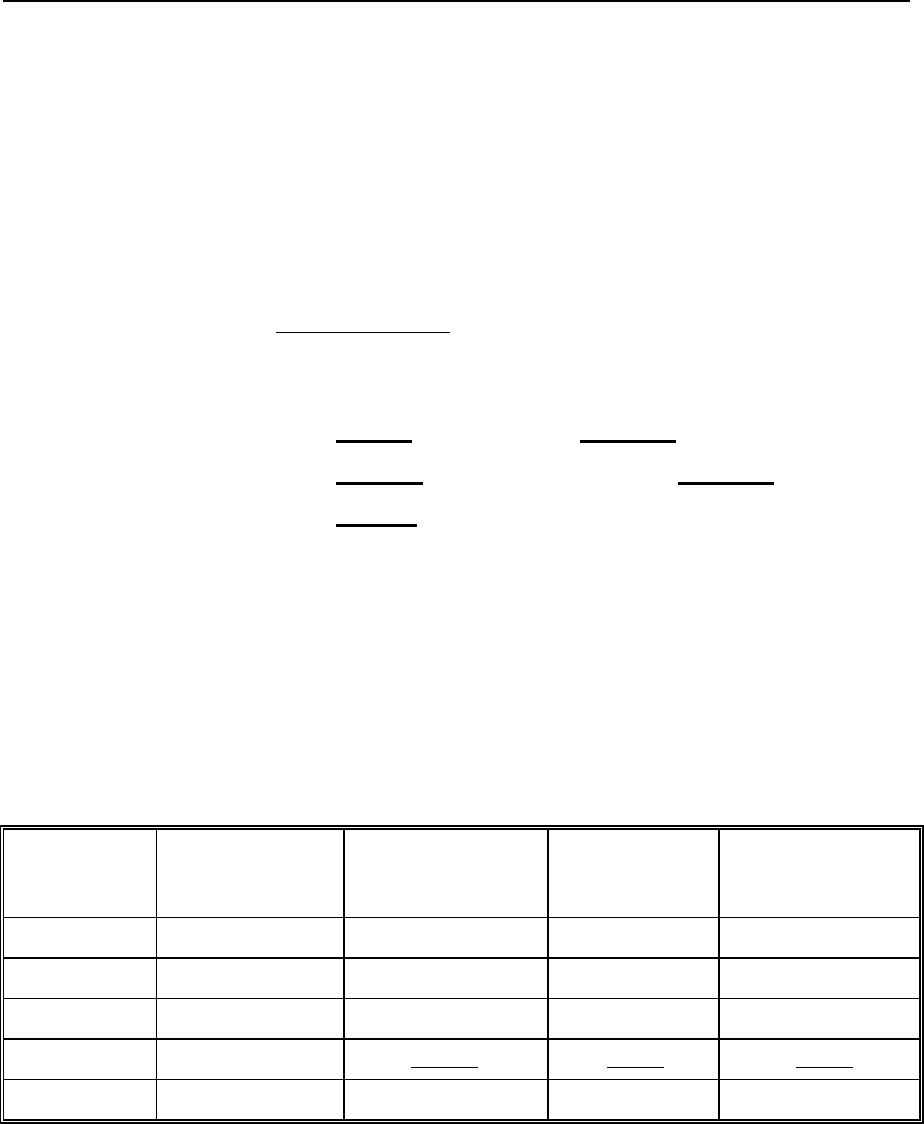

12. A 2-year Treasury note with a coupon rate of 6.5% has a percentage issue price of

98.50. What is the duration of the instrument?

Duration = 1.9067 years

Use this table to help with your calculation.

Price: 98.50 BEY: 7.3199%

Coupon: 6.50% Discount Rate: 7.4538%

Maturity: 2 years

Make sure that you have calculated the correct discount rate.

Find the yield to maturity of the note using the bond features on your calculator.

That rate should be 7.3199%.

Convert this to an equivalent semi-annual discount rate.

Divide 0.073199 by 2, add 1, square this result, and subtract 1.

You should get 0.074538.

Use this rate to discount the cash flows and your table should look like this.

Time Cash Flow

Present

Value at Semi-

annual Rate

Present

Value /

Bond Price

Time-

weighted

Value

0.5 3.25 3.1353 0.0318 0.0159

1.0 3.25 3.0246 0.0307 0.0307

1.5 3.25 2.9178 0.0296 0.0444

2.0 103.25 89.4224 0.9078 1.8157

TOTAL 98.5001 0.9999 1.9067

13. What is the duration of the following portfolio?

(0.425) (1.8654) + (0.378) (4.7333) + (0.197) (9.6655) = 4.4861 years

www.LisAri.com

FIXED INCOME SECURITIES 9-43

v.05/13/94 v-1.1

p.01/14/00

UNIT SUMMARY

In this unit, we introduced the basic methodologies for pricing and

calculating yield on debt securities that trade in the secondary

markets. Specifically, we discussed U.S.Treasury bills, notes, bonds,

and Eurobonds.

Treasury bills are short-term, zero-coupon (non-interest bearing)

securities. The quoted price of a Treasury bill is discounted from the

face value at a discount rate that is often referred to as the yield to

maturity of the security. The discount rate is based on the face value

of the security; the rate of return to the investor or true yield of the

bill is based on the difference between the purchase price and the

sale price.

Treasury notes are bonds with maturities ranging from one to ten years

that make semi-annual interest payments. Since all Treasuries are

quoted in terms of annual discount rates and annual coupon payments,

the price of Treasury notes is adjusted for the semi-annual interest

payments. You learned how to calculate the price of a note and the

yield to maturity.

Treasury bonds are securities with maturities greater than ten years.

The most common maturities are 20 to 30 years. Since bonds make

semi-annual coupon payments to investors, the price and yield

calculations are the same as they are for Treasury notes.

A Eurobond is a debt instrument issued by a company in an

international market that is outside any domestic regulations. They

typically make annual coupon payments to the investor.

The true selling price of a security that makes periodic interest

payments includes an adjustment for accrued interest which is owed

to the seller by the buyer. The convention is to adjust the payment by

the number of days in the coupon period that the security is actually

held by the seller.

www.LisAri.com

9-44 FIXED INCOME SECURITIES

v-1.1 v.05/13/94

p.01/14/00

Bond prices are affected by their sensitivity to market interest rates,

the maturity of the bond, and the effective life of the bond. Duration

is the measure we use to estimate the average maturity of a bond's

cash flows.

You have demonstrated your understanding of each of these key concepts in the four

practice exercises; therefore, this unit has no Progress Check. Please continue your study

of securities with Unit Ten: Derivative Securities, which follows.

www.LisAri.com

Unit 10

www.LisAri.com

www.LisAri.com

v.05/13/94 v-1.1

p.01/14/00

UNIT 10: DERIVATIVE SECURITIES

INTRODUCTION

In Unit Two, we introduced the three general subsets of capital markets: bond (debt)

markets, equity markets, and derivative markets. In this unit we will focus on the

derivative markets.

There are three basic forms of derivative products: forwards, options, and swaps. These

instruments are often referred to as derivative securities because their values are derived

from the value of the underlying security. In this unit you will be introduced to some of

the derivative instruments that investors use to manage exposure to risk.

We will focus on the characteristics of options and swaps and how the payoffs are

calculated for both types of instruments.

UNIT OBJECTIVES

After you successfully complete this unit, you will be able to:

• Recognize terminology that is associated with options trading

• Recognize the payoff profiles for call options and put options

• Identify the characteristics of interest rate swaps and currency swaps

OPTIONS

An option contract between a buyer (holder) and a seller (writer)

describes the rights of the option holder and the obligations of the

option writer.

www.LisAri.com

10-2 DERIVATIVE SECURITIES

v-1.1 v.05/13/94

p.01/14/00

The purchase price of an option is called the premium. This is the

compensation that the holder of the option pays to the writer for the

rights described in the option contract.

Calls and puts

There are two types of options: call options and put options.

Call options - give the holder the right to buy an asset for a

specified price on or before a given expiration

(maturity) date.

Put options - give the holder the right to sell an asset for a

specified price on or before a given expiration

(maturity) date.

The specific asset named in the option contract is called the

underlying asset. The price at which the underlying asset may be

bought is called the exercise or strike or contract price. Purchasing

(or selling) the underlying asset of an option contract is referred to

as exercising the option.

The key thing to remember is that the holder of the option has the

right (but not the obligation) to exercise the option.

In the money /

Out of the

money

An option is "in the money" when its exercise would produce profits

for its holder. An option is "out of the money" during the time when

its exercise would not be profitable for its holder. This means that a

call option on a stock is in the money when the exercise price is

below the market price of the stock; a put option is profitable when

the exercise price is above the market price of the stock.

American /

European

Options may be either American or European. American options give

the holder the right to exercise the option at any time up to the

expiration date. European options give the holder the right to

exercise the option only on the expiration date.

www.LisAri.com

DERIVATIVE SECURITIES 10-3

v.05/13/94 v-1.1

p.01/14/00

Background and Markets

When options were first traded, contracts were arranged between pairs

of investors and customized to meet specific needs. These customized

contracts could vary according to exercise price, expiration date, and

underlying asset. Because of these infinite possibilities, it was nearly

impossible for a secondary options trading market to exist. Investors

would enter into customized agreements according to their investment

needs; if their needs changed, it was difficult to find another investor

to buy the option contract.

Secondary

markets

This lack of liquidity and standardization was one of the driving

forces behind the creation of the Chicago Board Options Exchange

(CBOE) in 1973. The CBOE enacted rules to standardize option

contracts in order to restrict the number of contract types that would

trade on the exchange. Soon, other option exchanges were created.

This led to a broader standardization of option contracts and was the

key to creating a secondary market for options and increasing the

liquidity of option contracts.

Customized option contracts are still available to investors — they

are traded in over-the-counter (OTC) markets. These customized

options are usually considerably more expensive than the standard

option contracts because of the lack of liquidity.

Standardized

contracts

The first standardized contracts were for the purchase or sale of

common stock. However, investors soon created demand for options

on a variety of financial and physical assets, including options on:

• Common stock

• Stock indices

• Debt instruments

• Interest rate futures

• Foreign currency futures

• Agricultural commodities

• Precious metals

www.LisAri.com