Citibank: basic of corporate finance

Подождите немного. Документ загружается.

2-8 FINANCIAL MARKETS AND INTEREST RATES

v-1.1 v.05/13/94

p.01/14/00

Risk

There are several types of risk that can be included in the risk

premium. Usually, it is difficult to quantify what percentage of the

risk premium is associated with each type of risk. Let's look at three

risks that affect the amount of the risk premium: counterparty risk,

liquidity risk, and interest rate risk.

Counterparty

(default) risk

Counterparty (default) risk is the chance that the borrower will not be

able to pay the interest or pay off the principal of a loan. This risk can

influence the level of interest rates. It is generally considered that

U.S. Treasury securities have no default risk –

the U.S. government will always pay interest and will repay the

principal of its borrowings. Therefore, the difference in price

between a U.S. Treasury security and another corporate bond with

similar maturity, liquidity, etc. may be the risk premium for assuming

counterparty risk.

Several ratings companies identify and classify the creditworthiness of

corporations and governments to determine how large the risk

premium should be. They apply specific ratings such as AAA or BBB

to indicate the likelihood of default by the borrowing entity.

A corporation with a AAA rating will have a smaller default risk than a

firm with a BBB rating and, therefore, will be able to borrow capital at

a lower interest rate (other factors being equal).

www.LisAri.com

FINANCIAL MARKETS AND INTEREST RATES 2-9

v.05/13/94 v-1.1

p.01/14/00

Liquidity risk

Liquidity refers to the marketability of assets – the ease with which

assets can be sold for cash on short notice at a fair price. Investors

may require a premium return on an asset to compensate for a lack of

liquidity. For example, there are active world markets in which

investors holding bonds issued by Ford Motor Company can easily

sell the bonds and receive cash within a matter of seconds. On the

other hand, an investor who has loaned money to a small Honduran

trading company will have a much more difficult time finding another

investor in the secondary market to purchase the loan.

The Honduran trading company pays a higher interest rate for its

borrowings than does Ford (all other factors being equal) because

its securities are harder to sell in the secondary market.

Interest rate

risk

As interest rates fluctuate, so do the prices of bonds in the secondary

markets. We will discuss this relationship between interest rates and

bonds in more detail later in the course. For now, you need to know

how a change in rates affects bond prices.

• As interest rates increase, bond prices

decrease.

• As interest rates decrease, bond prices

increase.

After an interest rate increase, newly issued bonds yield larger

interest payments than older bonds. The price of old bonds falls to

attractive levels so that investors will continue to buy them. Older

bonds are priced in the market so that the rate of return paid on the

investment is approximately the same as other investment

opportunities with similar risk and maturity.

All long-term bonds carry interest rate risk because there is more

opportunity for interest rates to rise. For this reason, investors often

require a risk premium in the stated interest rate. The net effect of

this premium is to raise rates on long-term bonds relative to the

rates on short-term bonds.

www.LisAri.com

2-10 FINANCIAL MARKETS AND INTEREST RATES

v-1.1 v.05/13/94

p.01/14/00

Measuring

risk premium

The risk premium is difficult to measure, but researchers have

identified two characteristics that serve as a reference:

1. Rate volatility – Premiums are higher when interest rates

are volatile and uncertain.

2. Historical data – The premium on 30-year U.S. Treasury

bonds generally has fluctuated between 1% and 2%, with an

average of about 1.7% for the last 60 years.

Short-term bonds are also subject to risk as a result of changing

interest rates. Most investors reinvest their funds as short-term

bonds mature and are paid off. If interest rates are falling, the new

bonds will pay less interest than the previously held bonds. This

reinvestment risk is of particular concern to investors living off the

proceeds of their investment.

Term Structure of Interest Rates

Relationship

between long-

and short-term

rates

The term structure of interest rates refers to the relationship between

long-term and short-term interest rates. Investors are concerned with

the term structure because it affects their investment preferences for

long- or short-term bonds. Corporate treasurers also must decide

whether to borrow by issuing long- or short-term bonds. We will

discuss how long- and short-term rates are related and what causes

changes in their relative values.

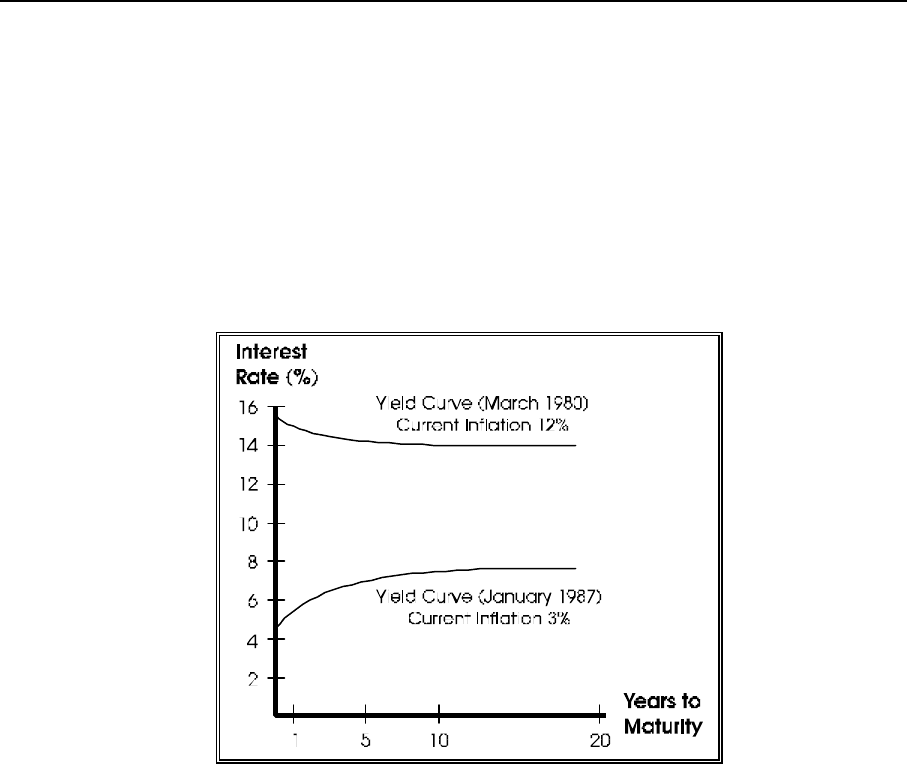

Yield Curve

Rates of return

plotted on a

graph

Interest rates on bonds of differing maturities are plotted on a graph to

illustrate their relationship. A graphic representation of the term

structure of interest rates is called a yield curve. "Yield" refers to the

rate of return on an investment. For our term structure study, the yield

of a security is the rate of interest paid on the security. The graph in

Figure 2.1 shows yield curves for two different U.S. Treasury

securities for two different dates. Remember, interest

rates are always changing.

www.LisAri.com

FINANCIAL MARKETS AND INTEREST RATES 2-11

v.05/13/94 v-1.1

p.01/14/00

The vertical axis represents the interest rate; the horizontal axis

represents the number of years to maturity for the security. For

instance, the interest rate paid to an investor on a one-year security

in March of 1980 is 14% and the rate for a 20-year bond in January

of 1987 is 7.6%. We have not plotted every point exactly, but we

have plotted several common maturities and smoothed the curves to

illustrate the trends.

Fig. 2.1: Yield Curves for Two Different Maturities

Normal /

abnormal yield

curves

Let's examine the characteristics of the two curves. In March of 1980,

all interest rates were at relatively high levels — with long-

term rates lower than short-term rates. The January 1987 curve has

overall lower rates, with long-term rates slightly higher than short-

term rates. An upward sloping yield curve is often called a normal

yield curve, whereas a downward sloping yield curve is called an

abnormal (inverted) yield curve.

www.LisAri.com

2-12 FINANCIAL MARKETS AND INTEREST RATES

v-1.1 v.05/13/94

p.01/14/00

Normal Yield Curve Theories

Upward curve

considered

normal

There are three prevailing theories that explain why the upward sloping

yield curve is considered normal. These three theories are: the

expectations theory, the market segmentation theory, and the liquidity

preference theory.

1. Expectations Theory

The basis of the expectations theory is that the yield curve

reflects lenders' and borrowers' expectations of inflation.

Changes in these expectations cause changes in the shape of

the yield curve. Remember, the inflation premium is a major

component of interest rates.

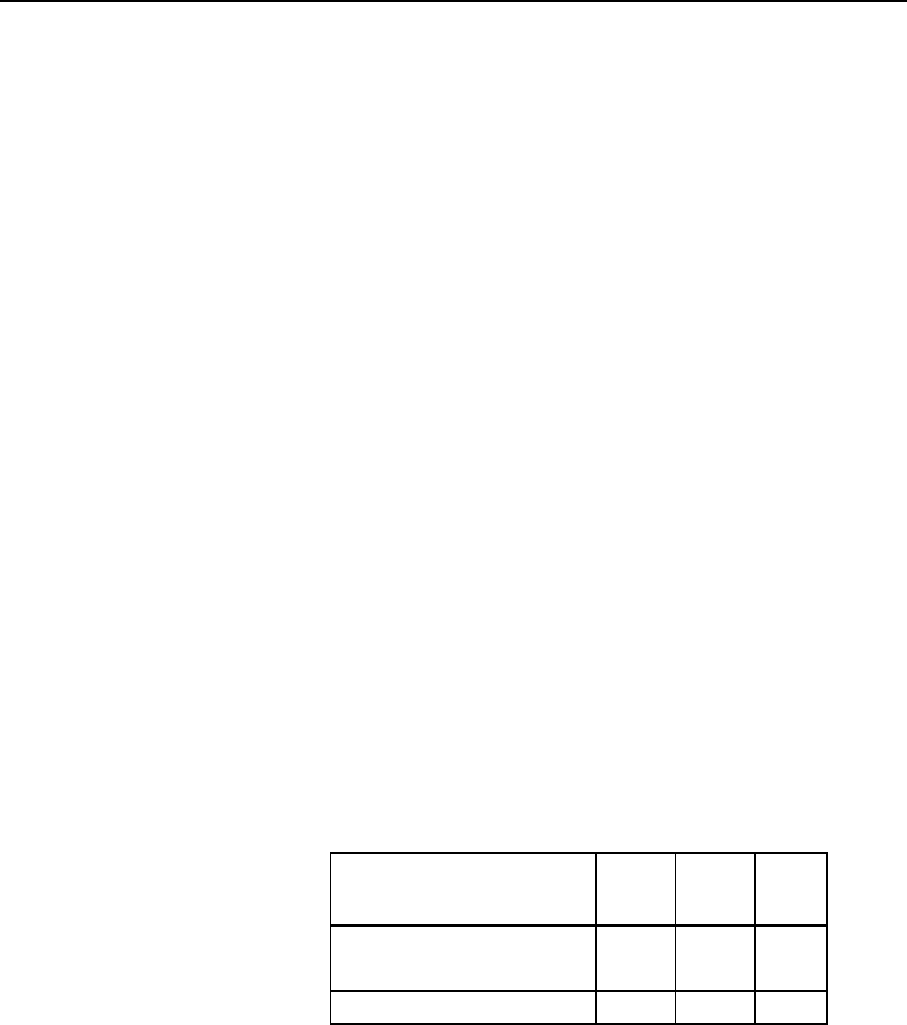

To illustrate the expectations theory, suppose that inflation is

expected to be 4% this coming year, 6% in the year

following, and 8% in the third year. The inflation premium

(average expected yearly inflation) will be 4% for the first

year, 5% for the second year, and 6% for the third year. If the

real, risk-free rate is 3%, then the resulting Treasury Bill

interest rates (risk-free rate plus inflation premium) will be

7% for a one-year T-bill, 8% for a two-year T-Bill, and 9%

for a three-year T-bill. A change in these expectations will

cause a shift in the yield curve for the T-Bills.

1st yr 2nd yr 3rd yr

Expected inflation 4% 6% 8%

Average inflation premium 4% 5% 6%

+ Real risk-free interest rate 3% 3% 3%

= T-bill interest rate 7% 8% 9%

2. Market Segmentation Theory

Each lender and each borrower has a preferred maturity. Some

lend / borrow for long-term needs and others lend / borrow for

short-term needs. The market segmentation theory states that

the slope of the yield curve depends on supply / demand

conditions in the short-term and long-term markets.

www.LisAri.com

FINANCIAL MARKETS AND INTEREST RATES 2-13

v.05/13/94 v-1.1

p.01/14/00

An upward sloping curve results from a large supply of funds

in the short-term market relative to demand and a shortage of

long-term funds. A downward sloping curve indicates strong

demand in the short-term market relative to the long-term

market. A fairly horizontal yield curve indicates that supply

and demand for funds is roughly balanced both in the short-

term and long-term markets.

3. Liquidity Preference Theory

The liquidity preference theory is based on the observation

that long-term securities often yield more than short-term

securities. Two reasons are given to explain this:

• Investors generally prefer short-term securities, which

are more liquid and less expensive to buy and sell.

Investors require higher yield on long-term instruments

to compensate for the higher cost.

• Borrowers dislike short-term debt because it exposes

them to the risk of having to roll over the debt or raise

new principal under adverse conditions (such as a rise in

rates). Borrowers will pay a higher rate for long-term

debt than for short-term debt, all other factors being

held constant.

Under these "normal" conditions, there is a positive correlation

between risk premium increases and maturity. Therefore, the "normal"

yield curve slopes upward.

There is no evidence that any of these theories clearly explains the

shape of the yield curve and its changes. However, each theory has

some merit, and all three theories are discussed by participants in

the markets as if they were valid.

www.LisAri.com

2-14 FINANCIAL MARKETS AND INTEREST RATES

v-1.1 v.05/13/94

p.01/14/00

Effect on Stock Prices

Impact on

corporate

profits

Interest rates indirectly impact stock prices through their effect on

corporate profits. The payment of interest is a cost to companies – the

higher the level of interest rates, the lower the level of corporate

profits (other factors held constant). Interest rates affect the level of

economic activity which, in turn, affects corporate profits.

Even more directly, interest rates affect the competition for funds

(capital) between stocks and bonds. Higher interest rates mean that

investors receive a higher return on their bond investments. High

bond yields induce investors to sell their stock holdings and invest in

more bonds. The reverse occurs when interest rates fall.

The effect of interest rates on corporate profits is more important

for individual companies, especially those with high debt levels. The

direct competition for capital has a more widespread effect on the

general stock price level for the entire economy.

UNIT SUMMARY

In this unit, we discussed the types of financial markets — money

markets and capital markets. There are two subsets of capital

markets — bond (debt) and equity markets. Players in the markets

include investors / lenders, issuers / borrowers, brokers, and dealers.

We said that investors' expectations of return on investment and

consumers' preferences for saving versus spending are two market

characteristics that affect the level of interest rates.

Interest rates required by investors are the sum of three factors:

Risk-free real rate (r

*

)

+ Premium for inflation (IP)

+ Premium for risk (RP)

= Interest rate (r)

r = r

*

+ IP + RP

www.LisAri.com

FINANCIAL MARKETS AND INTEREST RATES 2-15

v.05/13/94 v-1.1

p.01/14/00

Each of these factors fluctuates, given current and expected conditions

of the economy, the company, and the market in which the company

conducts business. Interest rates compensate investors for loaning

money, for anticipated inflation, and for assuming counterparty,

liquidity, and interest rate risk.

The term structure of interest rates is represented by a yield curve

and refers to the relationship between long-term and short-term

interest rates.

You have completed Unit Two: Financial Markets and Interest Rates. Please complete

Progress Check 2 and then continue to Unit Three: Time Value of Money. If you answer

any questions incorrectly, we suggest that you review the appropriate text.

www.LisAri.com

2-16 FINANCIAL MARKETS AND INTEREST RATES

v-1.1 v.05/13/94

p.01/14/00

(This page is intentionally blank)

www.LisAri.com

FINANCIAL MARKETS AND INTEREST RATES 2-17

v.05/13/94 v-1.1

p.01/14/00

4 PROGRESS CHECK 2

Directions: Select the one best answer for each question, unless otherwise indicated.

Check your responses with the Answer Key on the next page.

1. Match each market player with a description of his/her role. Write the letter of the

role next to the title of the market player.

Market Players Roles

____ Investor

____ Issuer

a) Financial intermediary that buys and sells

securities

____ Broker

b) Entity with more money than it needs

____ Dealer c) Entity in need of money

d) Financial intermediary that facilitates the

buying and selling of securities

2. The most liquid, lower-risk securities are traded in the:

_____a) bond market.

_____b) equity market.

_____c) money market.

_____d) derivative market.

3. QRS Manufacturing Company decides to "take the company public." This means

it will:

_____a) sell bonds to the public through the debt market.

_____b) issue stock in the primary equity market.

_____c) offer certificates of deposit in the money markets.

_____d) derive its funding from the derivatives market.

www.LisAri.com