CIMA - C2 Fundamentals of Financial Accounting

Подождите немного. Документ загружается.

130 9: Non-current assets – depreciation, revaluation and disposal ⏐ Part B Accounting systems and accounts preparation

If the original estimate of an asset's useful life is incorrect, it should be revised. Normally, no adjustment is made in

respect of the depreciation charged in previous years; but the remaining NBV of the asset should be depreciated over the

new estimate of its remaining useful life. However, if future results could be

materially

distorted, the adjustment to

accumulated depreciation should be recognised in the accounts.

1.5 Examples: depreciation

(a) A non-current asset costing $20,000, with an expected life of five years and an expected residual value of nil, will

be depreciated by $20,000 in total over the five year period.

(b) A non-current asset costing $20,000, with an expected life of five years and an expected residual value of $3,000,

will be depreciated by $17,000 in total over the five years.

(a) A depreciation charge (provision) is made in the income statement in each accounting period for every

depreciable non-current asset. Nearly all non-current assets are depreciable, the most important exceptions being

freehold land and long-term investments.

(b) The total accumulated depreciation builds up as the asset gets older. Therefore, for an asset with no residual

value, the total provision for depreciation increases until the non-current asset is fully depreciated (NBV is nil).

1.6 The ledger accounting entries for depreciation

(a) There is a provision for depreciation account for each separate category of non-current assets, eg plant

and machinery, land and buildings, fixtures and fittings.

(b) The depreciation charge for an accounting period is a charge against profit and is recorded as:

DEBIT Depreciation expense account

CREDIT Provision for depreciation account

(c) The balance on the provision for depreciation account is the total accumulated depreciation. This is always

a credit balance.

(d) The non-current asset accounts are unaffected by depreciation. Non-current assets are recorded in these

accounts at cost (or, if they are revalued, at their revalued amount).

(e) In the statement of financial position of the business, the accumulated depreciation is deducted from the

cost of non-current assets (or revalued amount) to arrive at the net book value of the non-current assets.

1.7 Example: accounting for depreciation

Using the information in Question 1 (Depreciation), write up the depreciation expense and provision for depreciation

accounts for 20X2, 20X3, 20X4 and 20X5.

Solution

DEPRECIATION EXPENSE ACCOUNT

$

$

31.12.X2

Provision

2,000

31.12.X2

I/S

2,000

31.12.X3

Provision

2,000

31.12.X3

I/S

2,000

31.12.X4

Provision

2,000

31.12.X4

I/S

2,000

31.12.X5

Provision

2,000

31.12.X5

I/S

2,000

Assessment

focus points

151465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 9: Non-current assets – depreciation, revaluation and disposal 131

DEPRECIATION PROVISION ACCOUNT

$

$

31.12.X2

Balance c/d

2,000

31.12.X2

Depreciation expense a/c

2,000

2,000

2,000

1.1.X3

Balance b/d

2,000

31.12.X3

Balance c/d

4,000

31.12.X3

Depreciation expense a/c

2,000

4,000

4,000

1.1.X4

Balance b/d

4,000

31.12.X4

Balance c/d

6,000

31.12.X4

Depreciation expense a/c

2,000

6,000

6,000

1.1.X5

Balance b/d

6,000

31.12.X5

Balance c/d

8,000

31.12.X5

Depreciation expense a/c

2,000

8,000

8,000

1.8 Methods of depreciation

There are several different methods of depreciation but the straight line method and the reducing balance method are

most commonly used in practice.

There are several different methods of depreciation. The ones you need to know about are:

•

Straight-line method

•

Reducing balance method

Another method is the revaluation method, but we will look at this in Section 2.

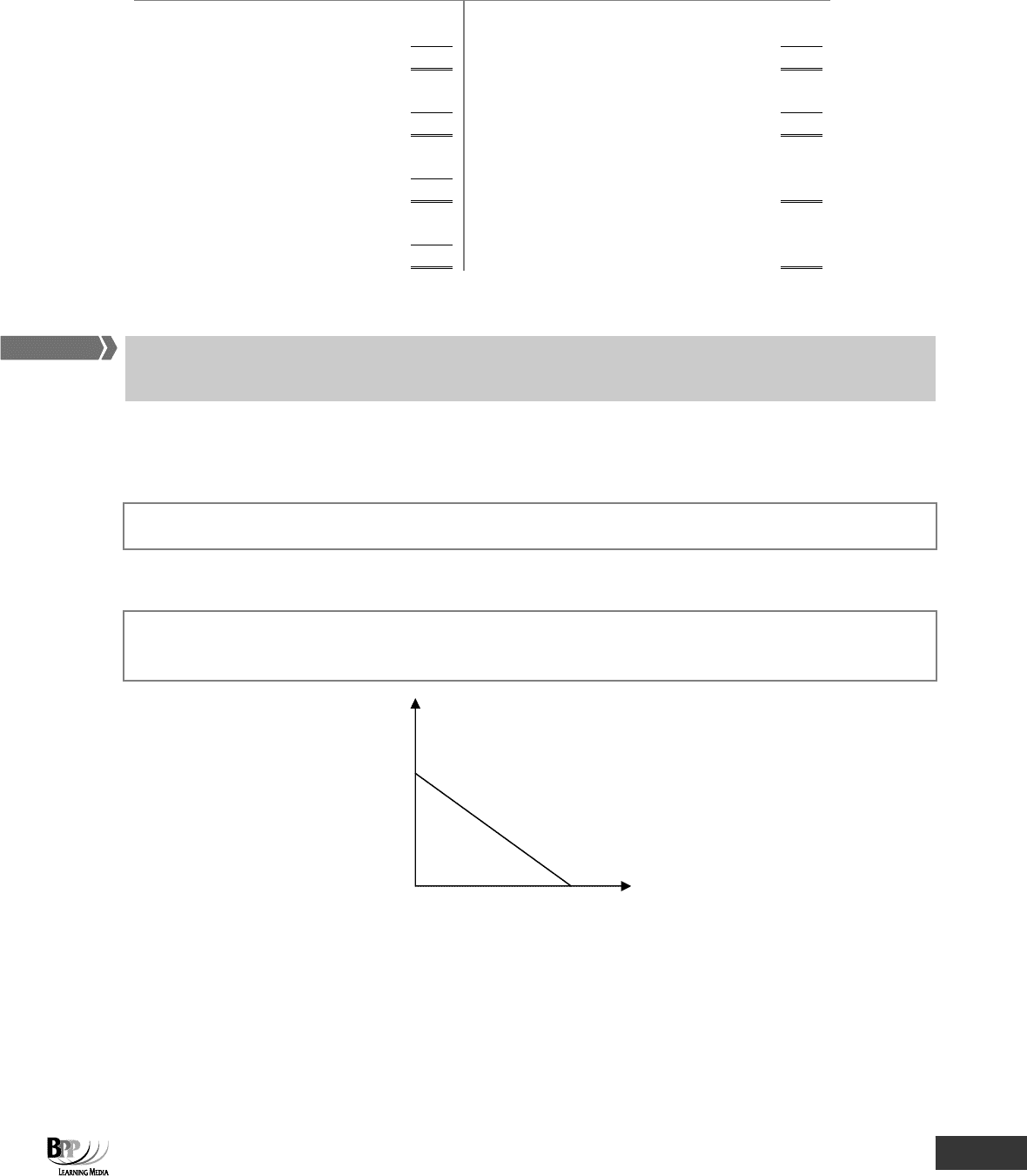

1.8.1 Straight line method

The

straight line method

means that the total depreciable amount is charged in equal instalments to each accounting

period over the expected useful life of the asset

The straight line method is a fair allocation of the total depreciable amount, if it is reasonable to assume that the

business enjoys equal benefits from the use of the asset throughout its life.

NBV

TIME

Key term

FA

S

T F

O

RWAR

D

Assessment

focus point

152465 www.ebooks2000.blogspot.com

132 9: Non-current assets – depreciation, revaluation and disposal ⏐ Part B Accounting systems and accounts preparation

The annual depreciation charge is calculated as:

Cost of asset minus residual value

Expected useful life of the asset

1.8.2 Example: straight line depreciation

(a) A non-current asset costs $20,000 with an estimated life of 10 years and no residual value.

Depreciation =

years10

000,20$

= $2,000 per annum

(b) A fixed asset costs $60,000 with an estimated life of 5 years and a residual value of $7,000.

Depreciation =

years5

)000,7000,60$( −

= $10,600 per annum

The net book value of the fixed asset is calculated as follows.

After 1

year

After 2

years

After 3

years

After 4

years

After 5

years

$

$

$

$

$

Cost of the asset

60,000

60,000

60,000

60,000

60,000

Accumulated depreciation

10,600

21,200

31,800

42,400

53,000

Net book value

49,400

38,800

28,200

17,600

7,000

*

* ie its estimated residual value.

Since the depreciation charge per annum is the same amount every year, it is often stated that depreciation is charged at

the rate of x per cent per annum on the cost of the asset. In the example above, the depreciation charge per annum is

10% of cost (ie 10% of $20,000 = $2,000).

Assessment questions

often describe straight line depreciation in this way.

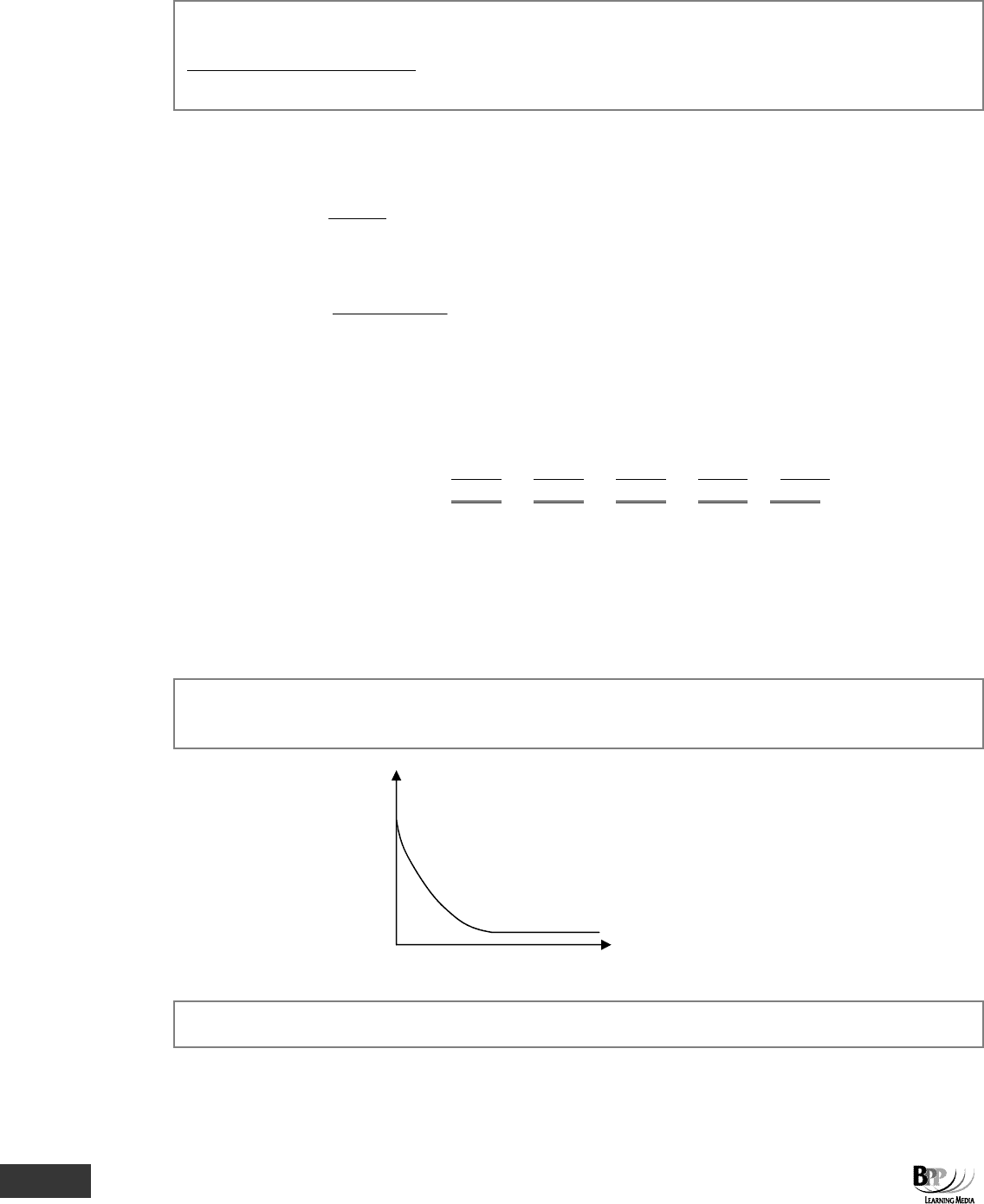

1.8.3 Reducing balance method

The

reducing balance method

of depreciation calculates the annual charge as a fixed percentage of the

net book value

of the asset, as at the end of the previous accounting period.

Reducing balance method = Net book value × X%.

NBV

TIME

Formula to

learn

Key term

Formula to

learn

153465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 9: Non-current assets – depreciation, revaluation and disposal 133

1.8.4 Example: reducing balance depreciation

A business purchases a non-current asset at a cost of $10,000. Its expected useful life is 3 years and its estimated

residual value is $2,160. The business uses the reducing balance method and calculates that the rate of depreciation

should be 40% of the reducing (net book) value of the asset. (The method of deciding that 40% is a suitable annual

percentage is outside of the scope of your syllabus.)

Calculate the depreciation charge per annum and the net book value of the asset as at the end of each year.

Solution

Accumulated

depreciation

$

$

Asset at cost

10,000

Depreciation in year 1 (40%)

4,000

4,000

Net book value at end of year 1

6,000

Depreciation in year 2

(40% of reducing balance)

2,400

6,400

(4,000 + 2,400)

Net book value at end of year 2

3,600

Depreciation in year 3 (40%)

1,440

7,840

(6,400 + 1,440)

Net book value at end of year 3

2,160

With the reducing balance method, the annual charge for depreciation is higher in the earlier years of the asset

'

s life, and

lower in the later years. Therefore, it is used when it is considered fair to allocate a greater proportion of the total

depreciable amount to the earlier years. The assumption is that the benefits obtained by the business from using the

asset decline over time.

Question

Straight line and reducing balance methods

A lorry bought for a business cost $17,000. It is expected to last for five years and then be sold for scrap for $2,000.

Required

Work out the depreciation to be charged each year under the following methods.

(a) The straight line method

(b) The reducing balance method (using a rate of 35%)

Answer

(a) Under the straight line method, depreciation for each of the five years is:

Annual depreciation =

5

2,000$17,000

−

= $3,000

(b) Under the reducing balance method, depreciation for each of the five years is:

Year Depreciation

1 35% × $17,000 = $5,950

2 35% × ($17,000 – $5,950) = 35% × $11,050 = $3,868

3 35% × ($11,050 – $3,868) = 35% × $7,182 = $2,514

4 35% × ($7,182 – $2,514) = 35% × $4,668 = $1,634

5 Balance to bring book value down to $2,000 = $4,668 – $1,634 – $2,000 = $1,034

154465 www.ebooks2000.blogspot.com

134 9: Non-current assets – depreciation, revaluation and disposal ⏐ Part B Accounting systems and accounts preparation

1.9 Choice of method

Neither the CA 2006 nor IAS 16 states which method should be used. Management must exercise its judgement and IAS

16 states that:

'The depreciable amount of a tangible non-current asset should be allocated on a

systematic

basis over its useful

economic life. The depreciation method used should reflect as fairly as possible the pattern in which the asset's

economic benefits are consumed by the entity. The depreciation charge for each period should be recognised as an

expense in the income statement unless it is permitted to be included in the carrying amount of another asset.'

'A variety of methods can be used to allocate the depreciable amount of a tangible non-current asset on a systematic

basis over its useful life. The method chosen should result in a

depreciation charge throughout the asset's useful

economic life and not just towards the end of its useful life or when the asset is falling in value.'

IAS 16 also states that a change from one method of providing depreciation to another is allowed only if the new method

will give a fairer presentation of the company

'

s results and financial position. Such a change is not a change of

accounting policy and so no disclosure of a prior year adjustment is needed. Instead, the asset

'

s net book amount is

written off over its remaining useful life. The change of method, the reason for the change, and its quantitative effect, is

disclosed by note to the accounts.

Many companies carry non-current assets in their statements of financial position at revalued amounts, particularly in

the case of freehold buildings. When this is done, the depreciation charge is calculated on the basis of the revalued

amount (not the original cost).

1.10 Disclosure requirements of IAS 16

The following information should be disclosed separately in the financial statements for each class of tangible non-

current assets.

•

Depreciation methods used

•

Useful lives or the depreciation rates used

•

Total depreciation charged for the period

•

Where material, the financial effect of a change during the period in either the estimate of useful economic

lives or the estimate of residual values

•

The cost or revalued amount at the beginning and end of the financial period

•

The cumulative amount of depreciation at the beginning of and end the financial period

•

A reconciliation of the movements (separately disclosing additions, disposals, revaluations, transfers,

depreciation, impairment losses, and reversals of past impairment losses written back in the financial

period)

•

The NBV at the beginning and end of the financial period

Question

Depreciation: ledger accounts

Brian Box set up his own computer software business on 1 March 20X6. He purchased a computer system, at a cost of

$16,000. The system has an expected life of three years and a residual value of $2,500.

Using the straight line method of depreciation, produce the non-current asset account, provision for depreciation

account, income statement (extract) and statement of financial position (extract) for each of the three years, 28 February

20X7, 20X8 and 20X9.

155465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 9: Non-current assets – depreciation, revaluation and disposal 135

Answer

NON-CURRENT ASSET – COMPUTER EQUIPMENT

Date

$

Date

$

(a)

1.3.X6

Payable

16,000

28.2.X7

Balance c/d

16,000

(b)

1.3.X7

Balance b/d

16,000

28.2.X8

Balance c/d

16,000

(c)

1.3.X8

Balance b/d

16,000

28.2.X9

Balance c/d

16,000

(d)

1.3.X9

Balance b/d

16,000

The non-current asset has now lasted its expected useful life. However, until it is sold or scrapped, the asset still appears

in the statement of financial position at cost (less accumulated depreciation) and it remains in the ledger account for

computer equipment until disposal.

PROVISION FOR DEPRECIATION

Date

$

Date

$

(a)

28.2.X7

Balance c/d

4,500

28.2.X7

I/S

4,500

(b)

28.2.X8

Balance c/d

9,000

1.3.X7

Balance b/d

4,500

28.2.X8

I/S

4,500

9,000

9,000

(c)

28.2.X9

Balance c/d

13,500

1.3.X8

Balance b/d

9,000

28.2.X9

I/S

4,500

13,500

13,500

1 Mar 20X9

Balance b/d

13,500

The annual depreciation charge is

years3

)500,2–000,16($

= $4,500 pa

The asset is depreciated to its residual value. If it continues to be used, it will not be depreciated any further (unless its

residual value is reduced).

INCOME STATEMENT (EXTRACT)

Date

$

(a)

28 Feb 20X7

Provision for depreciation

4,500

(b)

28 Feb 20X8

Provision for depreciation

4,500

(c)

28 Feb 20X9

Provision for depreciation

4,500

STATEMENT OF FINANCIAL POSITION (EXTRACT) AS AT 28 FEBRUARY

20X7

20X8

20X9

$

$

$

Computer equipment at cost

16,000

16,000

16,000

Less accumulated depreciation

4,500

9,000

13,500

Net book value

11,500

7,000

2,500

156465 www.ebooks2000.blogspot.com

136 9: Non-current assets – depreciation, revaluation and disposal ⏐ Part B Accounting systems and accounts preparation

1.11 Assets acquired in the middle of an accounting period

A business can purchase new non-current assets at any time during the course of an accounting period. So it may seem

fair to charge depreciation in the period of purchase which reflects the limited amount of use the business has had in

that period.

1.12 Example: depreciation charge

A business, with an accounting year ending on 31 December, purchases a new non-current asset on 1 April 20X1, at a

cost of $24,000. The expected life of the asset is 4 years, and its residual value is nil. What is the depreciation charge for

20X1?

Solution

The annual depreciation charge will be

years4

24,000

= $6,000 per annum

However, since the asset was acquired on 1 April 20X1, the business has only benefited from the use of the asset for 9

months. Therefore it seems fair to charge depreciation in 20X1 for only 9 months.

12

9

× $6,000 = $4,500

In practice, however, many businesses ignore part-year depreciation, and charge a full year

'

s depreciation in the year of

purchase and none in the year of sale.

If a question gives you the purchase date of a non-current asset, which is in the middle of an accounting period, unless

told otherwise, you should assume that depreciation will be calculated on the basis of 'part year' use.

However, be sure to read the question carefully. A question may clearly state that depreciation on office equipment is

charged at 20% per annum on the net book value at the year end. This means that any equipment introduced during the

year will have a

full year's

depreciation charge.

1.13 Example: provision for depreciation with assets acquired part-way through

the year

Brian Box purchases a car for himself and later for his chief assistant Bill Ockhead. Relevant data is as follows.

Date of purchase Cost Estimated life Estimated residual value

Brian Box car 1 June 20X6 $20,000 3 years $2,000

Bill Ockhead car 1 June 20X7 $8,000 3 years $2,000

The straight line method of depreciation is to be used.

Prepare the motor vehicles account and provision for depreciation of motor vehicle account for the years to 28 February

20X7 and 20X8. (You should allow for the part-year

'

s use of a car in computing the annual charge for depreciation.)

Calculate the net book value of the motor vehicles as at 28 February 20X8.

Assessment

focus point

157465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 9: Non-current assets – depreciation, revaluation and disposal 137

Solution

(a) (i) Brian Box car Annual depreciation

years3

2,000)$(20,000

−

= $6,000 pa

Monthly depreciation $500

Depreciation 1 June 20X6 – 28 February 20X7 (9 months) $4,500

1 March 20X7 – 28 February 20X8 $6,000

(ii) Bill Ockhead car Annual depreciation

years3

2,000)$(8,000

−

= $2,000 pa

Depreciation 1 June 20X7 – 28 February 20X8 (9 months) $1,500

(b) MOTOR VEHICLES

Date

$

Date

$

1 Jun 20X6

Payables (or cash)

20,000

28 Feb 20X7

Balance c/d

20,000

1 Mar 20X7

Balance b/d

20,000

1 Jun 20X7

Payables (or cash)

8,000

28 Feb 20X8

Balance c/d

28,000

28,000

28,000

1 Mar 20X8

Balance b/d

28,000

PROVISION FOR DEPRECIATION OF MOTOR VEHICLES

Date

$

Date

$

28 Feb 20X7

Balance c/d

4,500

28 Feb 20X7

I/S

4,500

1 Mar 20X7

Balance b/d

4,500

28 Feb 20X8

Balance c/d

12,000

28 Feb 20X8

I/S

(6,000+1,500)

7,500

12,000

12,000

1 Mar 20X8

Balance b/d

12,000

STATEMENT OF FINANCIAL POSITION WORKINGS AS AT 28 FEBRUARY 20X8

Brian Box car

Bill Ockhead car

Total

$

$

$

$

$

Asset at cost

20,000

8,000

28,000

Accumulated

depreciation: (4,500 + 6,000)

10,500

1,500

12,000

Net book value

9,500

6,500

16,000

1.14 Applying a depreciation method consistently

The business has to decide which method of depreciation to use. Once that decision is made, however, it should not be

changed – the chosen method should be applied consistently from year to year. This is an example of the consistency

concept.

Similarly, the business has to decide a sensible life span for a non-current asset. Once that life span is chosen, it should

not be changed unless something unexpected happens to the non-current asset.

158465 www.ebooks2000.blogspot.com

138 9: Non-current assets – depreciation, revaluation and disposal ⏐ Part B Accounting systems and accounts preparation

However a business can depreciate different categories of non-current assets in different ways. If a business owns three

cars, then each car is depreciated in the same way (eg the straight line method) but another category of non-current

asset (photocopiers) can be depreciated using a different method (eg by the reducing balance).

1.15 Changes in residual value or remaining useful life

If there is a change in residual value or remaining useful life, depreciation is recalculated using the following formula:

life useful Revised

any) (if valueresidual revised valuebook Net

−

(a) Depreciation is a measure of the 'wearing out' of a non-current asset.

(b) The accruals concept requires that depreciation be charged over the useful life of an asset.

(c) Two common methods of calculating depreciation are straight line and reducing balance.

(d) To record depreciation:

DEBIT Depreciation expense account

CREDIT Depreciation provision

Then to get the charge into the income statement

DEBIT Income statement

CREDIT Depreciation expense account

2 Revaluation of non-current assets

When a non-current asset is revalued, depreciation is charged on the revised amount.

2.1 Revaluations

Due to inflation, it is now quite common for the market value of certain non-current assets to go up. The most obvious

example of rising market values is land and buildings.

A business is not obliged to revalue non-current assets. However, in order to give a

'

true and fair view

'

it may decide to

revalue some non-current assets upwards. When non-current assets are revalued, depreciation is charged on the

revalued amount.

2.2 Example: the revaluation of non-current assets

Ira Vann commenced trading on 1 January 20X1 and purchased freehold premises for $50,000.

For the purpose of accounting for depreciation, he decided that

(a) the freehold land part of the business premises was worth $20,000 and would not be depreciated.

(b) the building part of the business premises was worth the remaining $30,000. This would be depreciated by the

straight-line method to a nil residual value over 30 years.

FA

S

T F

O

RWAR

D

Assessment

focus point

159465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 9: Non-current assets – depreciation, revaluation and disposal 139

After five years, on 1 January 20X6, the business premise is now worth $150,000.

$

Land

75,000

Building

75,000

150,000

He estimates that the building still has a further 25 years of useful life remaining.

Calculate the annual charge for depreciation in each of the 30 years of its life, and the statement of financial position

value of the land and building as at the end of each year.

Solution

Before the revaluation

, the annual depreciation charge is $1,000 ($30,000/30) per annum on the building. This charge is

made in each of the first five years of the asset

'

s life.

The net book value of the total asset will decline by $1,000 per annum.

(a) $49,000 as at 31.12.X1

(b) $48,000 as at 31.12.X2

(c) $47,000 as at 31.12.X3

(d) $46,000 as at 31.12.X4

(e) $45,000 as at 31.12.X5

When the revaluation takes place

, the amount of the revaluation is:

$

New asset value

150,000

Net book value as at end of 20X5

45,000

Amount of revaluation

105,000

The asset will be revalued by $105,000 to $150,000. If you remember the accounting equation, you will realise that if

assets go up in value by $105,000, capital or liabilities must increase by the same amount. Since the increased value

benefits the owner of the business, the amount of the revaluation is added to capital, usually as a separate

revaluation

reserve

.

After a revaluation, depreciation is calculated using the following formula:

life useful Remaining

any) (if valueresidual amount Revalued

−

After the revaluation

, depreciation will be charged on the building at a new rate.

years25

$75,000

= $3,000 per annum

The net book value of the property will then fall by $3,000 per annum over 25 years, from $150,000 as at 1 January

20X6 to only $75,000 at the end of the 25 years – ie the building part of the property value will be fully depreciated.

The consequence of an upwards revaluation is therefore a higher annual depreciation charge.

2.3 Revaluation method of depreciation

Under the revaluation method of depreciation, an asset is revalued at the end of every year. The difference between the

two amounts is then taken as depreciation.

160465 www.ebooks2000.blogspot.com