CIMA - C2 Fundamentals of Financial Accounting

Подождите немного. Документ загружается.

80 5: Ledger accounting and double entry ⏐ Part B Accounting systems and accounts preparation

Required

(a) Open accounts for Omega's customers and suppliers and record therein the 1 May balances.

(b) Record the transactions in the appropriate personal account and nominal ledger accounts.

(c) Balance the personal accounts where necessary.

(d) Extract a list of receivables at 31 May.

Answer

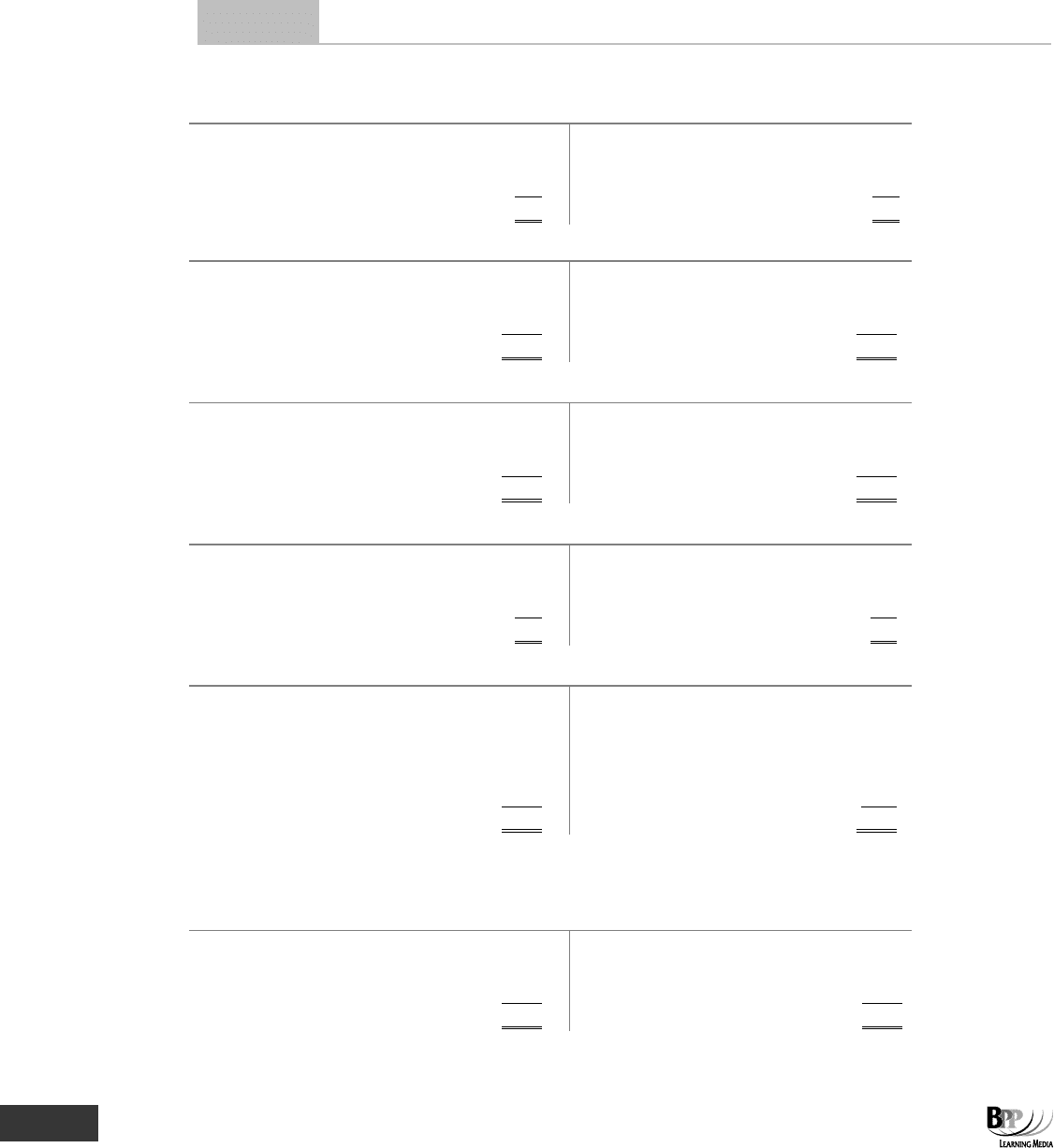

SALES LEDGER

(a),(b),(c) ALPHA

$

$

Opening balance

210

May sales

88

Balance c/d

298

298

298

BETA

$

$

Opening balance

1,040

Cash

1,040

May sales

314

Balance c/d

314

1,354

1,354

GAMMA

$

$

Opening balance

1,286

Cash

826

May sales

432

Balance c/d

892

1,718

1,718

DELTA

$

$

Opening balance

279

Cash

279

May sales

417

Balance c/d

417

696

696

EPSILON

$

$

Opening balance

823

Cash

823

May sales

129

Returns

88

May sales

269

Balance c/d

538

May sales

228

1,449

1,449

PURCHASES LEDGER

ZETA

$

$

Cash

1,000

Opening balance

2,173

Balance c/d

1,441

May purchases

268

2,441

2,441

101465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 5: Ledger accounting and double entry 81

ETA

$

$

Cash

187

Opening balance

187

Balance c/d

1,164

May purchases

423

May purchases

741

1,351

1,351

THETA

$

$

Cash

318

Opening balance

318

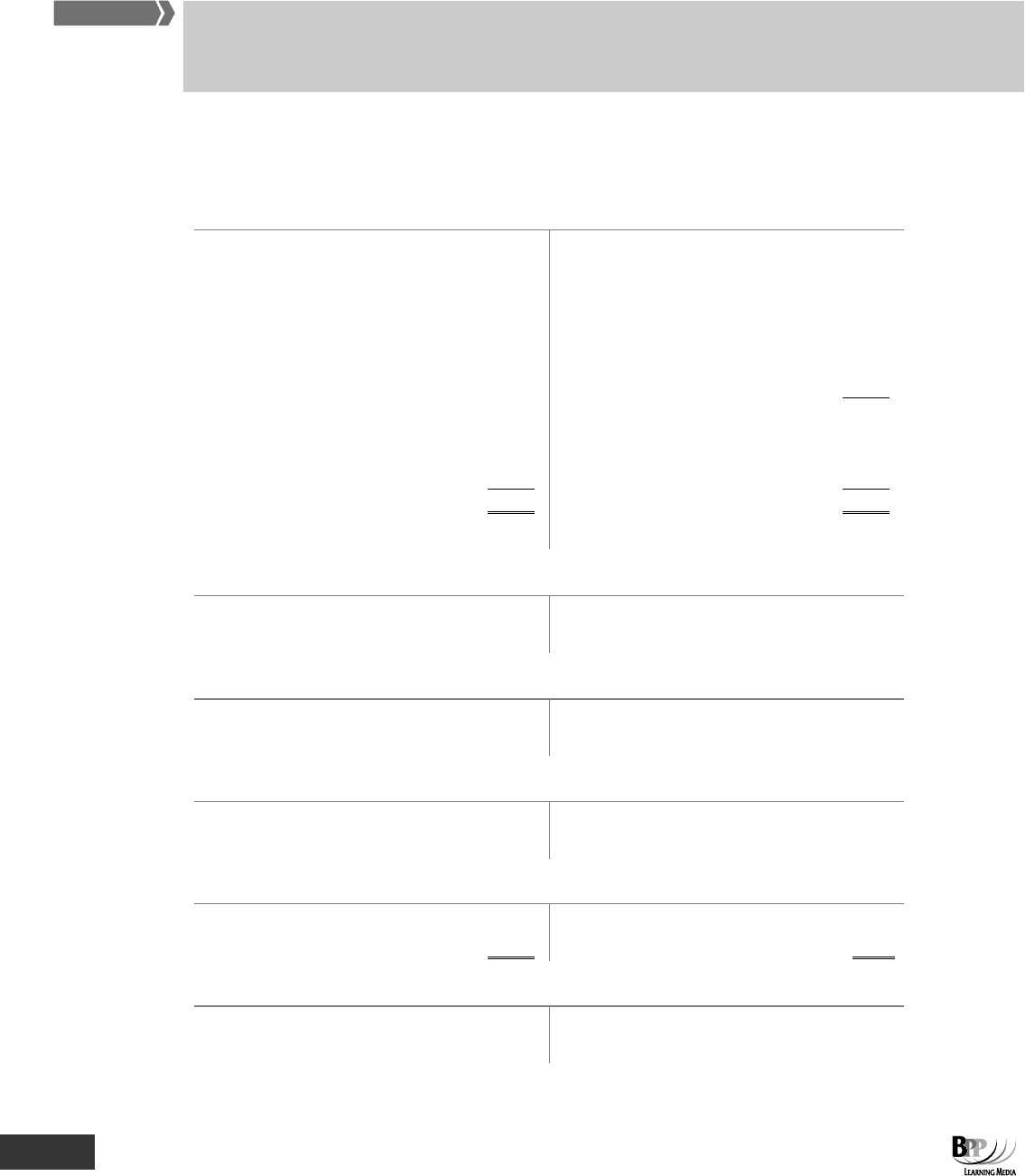

NOMINAL LEDGER

SALES ACCOUNT

$

$

May sales

1,877

PURCHASES ACCOUNT

$

$

May purchases

1,432

SALES RETURNS ACCOUNT

$

$

May returns

88

RECEIVABLES ACCOUNT

$

$

Opening balance

3,638

May returns

88

May sales

1,877

May receipts

2,968

Balance c/d

2,459

5,515

5,515

PAYABLES ACCOUNT

$ $

May payments 1,505 Opening balance 2,678

May purchases 1,432

CASH ACCOUNT

$

$

May receipts

2,968

May payments

1,505

(d) RECEIVABLES AS AT 31 MAY

May

$

Alpha

298

Beta

–

314

Gamma

892

Delta

–

417

Epsilon

538

2,459

102465 www.ebooks2000.blogspot.com

82 5: Ledger accounting and double entry ⏐ Part B Accounting systems and accounts preparation

Note. Compare this total to the balance on the receivables account! We will return to this in Chapter 13 on control

accounts. However you should not be surprised that the total of the individual customer accounts in the sales ledger

agrees to the balance on the receivables account.

6.6 Summary

(a) Business transactions are recorded on source documents.

(b) Source documents are recorded in day books.

(c) Totals of day books are recorded by double entry in nominal ledger accounts.

(d) Single transactions are recorded from day books to individual customer and supplier accounts by single entry.

(e) Customer accounts are in the sales ledger

(f) Supplier accounts are in the purchase ledger

(g) The sales and purchase ledger are not part of the double entry system

(h) The nominal ledger contains one account for each item in the statement of financial position and income

statement.

Chapter roundup

• The nominal ledger contains a separate account for each item which appears in a statement of financial position or

income statement.

• The double entry system of bookkeeping means that for every debit there is an equal credit. This is sometimes referred

to as the concept of duality.

• Cash transactions are settled immediately. Credit transactions give rise to receivables and payables.

• The journal is commonly used to record corrections of errors that have been made in writing up the nominal ledger accounts.

• Individual transactions are recorded in day books. Day book totals are recorded in double entry in the nominal ledger.

• Personal accounts are not part of the double entry system. They record how much is owed by a customer or to a

supplier. They are memorandum accounts only.

• The sales ledger contains separate accounts for each credit customer so that, at any time, a business knows how much

it is owed by each customer.

• The purchase ledger contains separate accounts for each credit supplier, so that, at any time a business knows how

much it owes to each supplier.

103465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 5: Ledger accounting and double entry 83

Quick quiz

1 The suppliers personal accounts will appear in which of the following business records?

A The nominal ledger

B The sales ledger

C The purchase day book

D The purchase ledger

2 The double entry to record a cash sale of $50 is:

DEBIT ___________________________ $50

CREDIT ___________________________ $50

3 The double entry to record a purchase of office chairs for $1,000 is:

DEBIT ___________________________ $1,000

CREDIT ___________________________ $1,000

4 The double entry to record a credit sale is:

DEBIT ___________________________

CREDIT ___________________________

5 Which of these statements are correct?

(i) The purchase day book is part of a double entry system.

(ii) The purchase ledger is part of a double entry system.

A (i) only

B (i) and (ii)

C (ii) only

D Both are false

6 Personal accounts contain records of

A Receivables and payables

B Assets and liabilities

C Income and expenditure

D Transactions with the proprietor of the business

7 A credit sale of $2,000 would be recorded using which of the following journals?

A DEBIT sales $2,000

CREDIT receivables $2,000

B DEBIT receivables $2,000

CREDIT sales $2,000

C DEBIT sales ledger $2,000

CREDIT sales $2,000

D DEBIT sales $2,000

CREDIT sales ledger $2,000

104465 www.ebooks2000.blogspot.com

84 5: Ledger accounting and double entry ⏐ Part B Accounting systems and accounts preparation

Answers to quick quiz

1 D This is correct

A This ledgers is used to record impersonal accounts.

B Customers accounts are kept in the sales ledger.

C This is simply a record of purchase invoices received.

2 DEBIT: CASH $50; CREDIT: SALES $50

3 DEBIT: NON-CURRENT ASSETS $1,000; CREDIT: CASH $1,000

4 DEBIT: RECEIVABLES; CREDIT: SALES

5 D is correct. The purchase day book is a book of prime entry, and the purchase ledger shows balances on suppliers

accounts. Neither are part of the double entry in the nominal ledger.

6 A Correct.

B These would be in the nominal ledger.

C These would be in the nominal ledger.

D These would be in either the nominal ledger or a 'private ledger' not accessible by accounting staff.

7 B Correct.

A This is a reversal of the correct entries.

C&D Remember that the sales ledger is not usually part of the double entry system.

Now try the questions below from the Question Bank

Question numbers Page

13–19 394

105465 www.ebooks2000.blogspot.com

85

From trial balance to

financial statements

Introduction

In the previous chapters you learned the principles of double entry and how to post to the

ledger accounts. The next step in our progress towards the financial statements is the trial

balance.

Before transferring the relevant balances at the year end to the income statement and putting

closing balances carried forward into the statement of financial position, it is usual to test the

accuracy of the double entry bookkeeping records by preparing a trial balance. This is done

by taking all the balances on every account. Due to the nature of double entry, the total of the

debit balances will be exactly equal to the total of the credit balances.

In very straightforward circumstances, it is possible to prepare accounts directly from a trial

balance. This is covered in Section 4.

Topic list S yllabus references

1 The trial balance B (7)

2 The income statement D (6)

3 The statement of financial position D (6)

4 Balancing accounts and preparing financial statements D (6)

106465 www.ebooks2000.blogspot.com

86 6: From trial balance to financial statements ⏐ Part B Accounting systems and accounts preparation

1 The trial balance

A trial balance is a list of nominal ledger account balances. It is prepared to check that the total of debit balances is the

same as the total of credit balances and offer reassurance that the double entry recording from day books has been done

correctly.

1.1 Example: trial balance

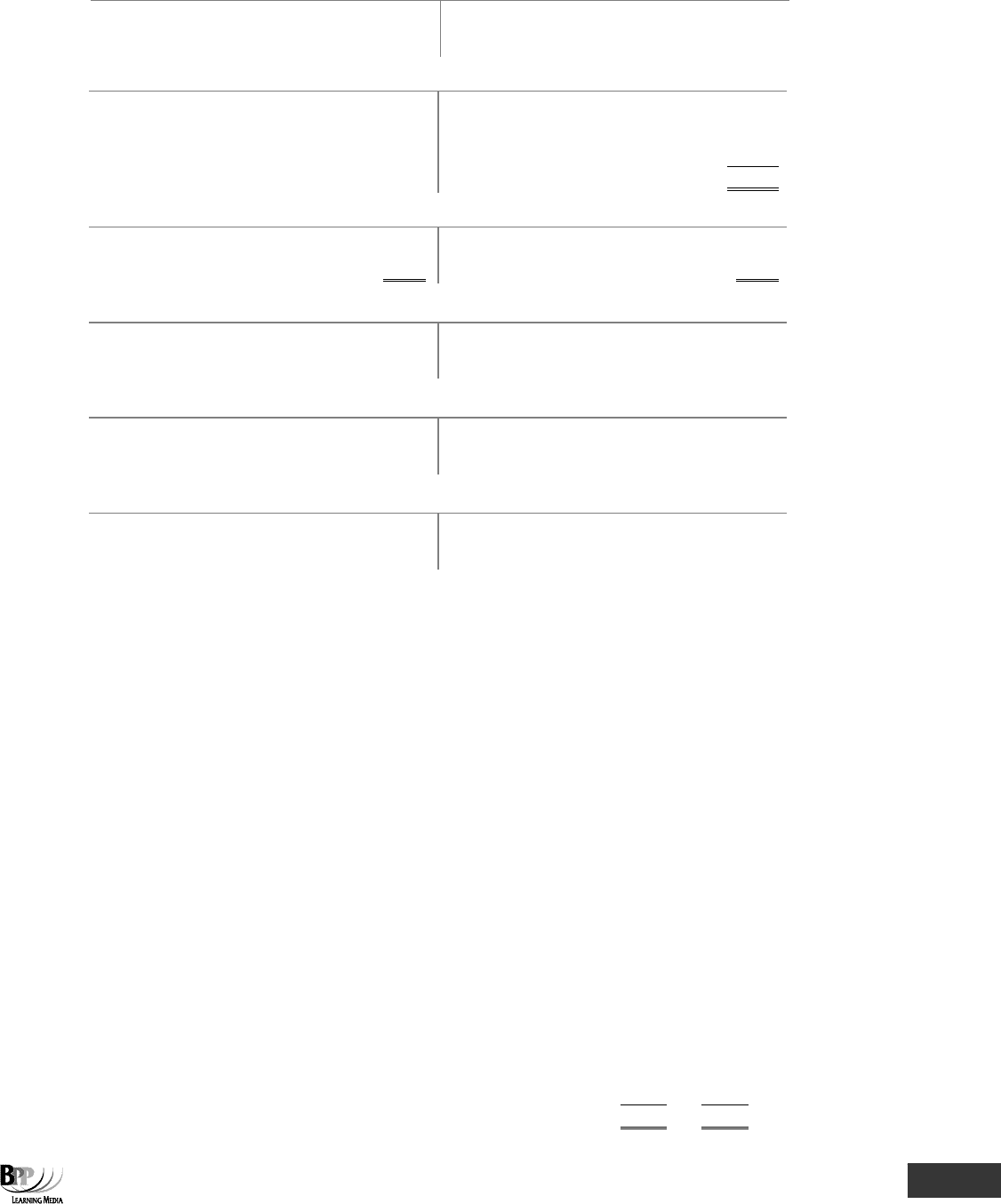

Here are the accounts of Ron Knuckle from the last chapter.

CASH

$

$

Capital – Ron Knuckle

7,000

Rent

3,500

Bank loan

1,000

Shop fittings

2,000

Sales

10,000

Trade payables

5,000

Receivables

2,500

Bank loan interest

100

Incidental expenses

1,900

Drawings

1,500

14,000

(Balancing figure – the amount of

cash left over after payments have

been made) Balance c/d

6,500

20,500

20,500

Balance b/d

6,500

CAPITAL (RON KNUCKLE)

$

$

Cash 7,000

BANK LOAN

$ $

Cash 1,000

PURCHASES

$ $

Trade payables 5,000

TRADE PAYABLES

$

$

Cash

5,000

Purchases

5,000

RENT

$ $

Cash 3,500

FA

S

T F

O

RWAR

D

107465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 6: From trial balance to financial statements 87

SHOP FITTINGS

$ $

Cash 2,000

SALES

$

$

Cash

10,000

Receivables

2,500

12,500

RECEIVABLES

$

$

Sales

2,500

Cash

2,500

BANK LOAN INTEREST

$ $

Cash 100

OTHER EXPENSES

$ $

Cash 1,900

DRAWINGS ACCOUNT

$ $

Cash 1,500

At the end of an accounting period, a balance is struck on each account in turn. This means that all the debits on the

account are totalled and so are all the credits. If the total debits exceed the total credits there is said to be a debit balance

on the account. If the credits exceed the debits, then the account has a credit balance.

In our example, there is very little balancing to do. Both the trade payables account and the receivables account balance

off to zero. The cash account has a debit balance of $6,500 and the total on the sales account is $12,500, which is a

credit balance. Otherwise, the accounts have only one entry each, so there is no totalling to do to arrive at the balance on

each account.

If the basic principle of double entry has been correctly applied throughout the period, the credit balances equal the debit

balances in total.

Debit

Credit

$

$

Cash

6,500

Capital

7,000

Bank loan

1,000

Purchases

5,000

Trade payables

–

Rent

3,500

Shop fittings

2,000

Sales

12,500

Receivables

–

–

Bank loan interest

100

Other expenses

1,900

Drawings

1,500

20,500

20,500

108465 www.ebooks2000.blogspot.com

88 6: From trial balance to financial statements ⏐ Part B Accounting systems and accounts preparation

It does not matter in what order the various accounts are listed, because the trial balance is not a document that a

business has to prepare. It is just a method used to test the accuracy of the double entry bookkeeping.

1.2 What if the trial balance shows unequal debit and credit balances?

If the two columns of the trial balance are not equal, there must be an error in recording the transaction. However, a trial

balance will not disclose the following types of errors.

• Complete omission of a transaction, because neither a debit nor a credit is made. This is called an error of

omission.

• Posting of a transaction to the wrong account, although the right type of account, is called an error of

commission (eg a petrol purchase debited to heat and light expense account rather than motor expenses:

both are revenue expense accounts).

• Compensating errors (eg an error of $100 is exactly cancelled by another $100 error elsewhere).

• Errors of principle occur when the wrong type of account has been used (eg the purchase of a motor van

is debited to a revenue expense account, such as motor expenses, rather than a non-current asset

account).

• Errors of original entry, when the wrong amount is debited and credited to the correct accounts.

We will look at errors in detail at a later date.

Question

Trial balance

As at 30.3.20X7, your business has the following balances on its ledger accounts.

Accounts Balance

$

Bank loan 12,000

Cash 11,700

Capital 13,000

Rent 1,880

Trade payables 11,200

Purchases 12,400

Sales 14,600

Sundry payables 1,620

Receivables 12,000

Bank loan interest 1,400

Other expenses 11,020

Vehicles 2,020

On 31.3.X7 the business made the following transactions.

(a) Bought materials for $1,000, half for cash and half on credit.

(b) Made $1,040 sales, $800 of which was for credit.

(c) Paid wages to shop assistants of $260 in cash.

Required

Draw up a trial balance showing the balances as at the end of 31.3.X7.

109465 www.ebooks2000.blogspot.com

Part B Accounting systems and accounts preparation ⏐ 6: From trial balance to financial statements 89

Answer

First you must put the original balances into a trial balance – ie decide which are debit and which are credit balances.

Account

Dr

Cr

$

$

Bank loan

12,000

Cash

11,700

Capital

13,000

Rent

1,880

Trade payables

11,200

Purchases

12,400

Sales

14,600

Sundry payables

1,620

Receivables

12,000

Bank loan interest

1,400

Other expenses

11,020

Vehicles

2,020

52,420

52,420

Now we must take account of the effects of the three transactions which took place on 31.3.X7.

$ $

(a) DEBIT Purchases 1,000

CREDIT Cash 500

Trade payables 500

(b) DEBIT Cash 240

Receivables 800

CREDIT Sales 1,040

(c) DEBIT Other expenses 260

CREDIT Cash 260

When these figures are included in the trial balance, it becomes:

Account

Dr

Cr

$

$

Bank loan

12,000

Cash (11,700 – 500 + 240 – 260)

11,180

Capital

13,000

Rent

1,880

Trade payables (11,200 + 500)

11,700

Purchases (12,400 + 1,000)

13,400

Sales (14,600 + 1,040)

15,640

Sundry payables

1,620

Receivables (12,000 + 800)

12,800

Bank loan interest

1,400

Other expenses (11,020 + 260)

11,280

Vehicles

2,020

53,960

53,960

And it balances!

110465 www.ebooks2000.blogspot.com