ACCA P7 (INT) Advanced Audit & Assurance - Study Text - 2010 (Emile Woolf Publishing)

Подождите немного. Документ загружается.

Chapter 4: Professional responsibility and liability

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 65

Management is therefore responsible for the prevention and detection of fraud and

error.

Responsibilities of the auditor

The auditor is responsible for reporting on whether the financial statements show a

‘true and fair view’. He is therefore only concerned with fraud and error that has a

material effect on the true and fair view.

The auditor’s responsibility is to obtain reasonable assurance that the financial

statements, taken as a whole, are free from material misstatement, whether caused

by fraud or error.

It is not the primary responsibility of the auditor to prevent or detect fraud or error,

although the audit may act as a deterrent to fraud. Auditors may also discover error

or fraud during the course of their audit work, but they are by no means certain to

do so whenever error or fraud has occurred.

It must be recognised that some material misstatements caused by fraud or error

may go undetected, because of the inherent limitations in any audit and the fact that

deliberate attempts may be made to conceal fraud from the auditor.

ISA240 states the responsibilities of management and the auditor as follows:

‘The primary responsibility for the prevention and detection of fraud rests with

both those charged with governance of the entity and management.’

‘An auditor conducting an audit in accordance with ISAs is responsible for

obtaining reasonable assurance that the financial statements as a whole are free

from material misstatement, whether caused by fraud or error.’

Professional scepticism

The auditor should perform the audit with a suitable degree of professional

scepticism.

The audit team should discuss the possibility of fraud in the context of the

specific characteristics of the audit engagement.

Discussions should be held with management on the procedures (controls) in

place to detect or prevent fraud.

The risks of possible fraud should be identified and its possible impact on the

financial statements should be evaluated.

Audit procedures should be designed to obtain evidence that fraud, which may

impair the financial statements, has not occurred, or has been detected and

corrected (or disclosed in the financial statements).

Paper P7: Advanced audit and assurance (International)

66 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

2.3 The auditor’s procedures where fraud or error is suspected

The auditor should take the following steps when fraud or error is suspected:

Identify the extent and possible impact on the financial statements of the fraud

or error. Document the facts fully in the audit files. Additional testing may be

required to establish the likely extent of any misstatement.

Consider the possible impact on other areas of the audit and on the overall

assessment of audit risk. This may result in a revision to the original audit plan.

The findings should be discussed with management, regardless of the extent of

the problem, and management should be kept informed of developments.

The auditor should determine the action that management should take. This

should include the possibility of seeking legal advice if fraud is suspected.

The auditor should normally communicate on a formal basis to management at

an appropriate level. In the case of a company, the auditor communicates

formally with the board of directors or the audit committee. However, if

management themselves are involved in a suspected fraud, the auditor should

consider taking legal advice to decide the best course of action. In extreme cases,

the auditor may feel it is appropriate to resign.

The auditor should consider the impact on his audit report to the shareholders,

in terms of any impact on the true and fair view presented by the financial

statements.

The auditor should consider whether there is any requirement to report to

appropriate authorities. This must be considered in the context of the auditor’s

duty of confidentiality to his client.

Chapter 4: Professional responsibility and liability

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 67

The auditor’s liability

Criminal liability

Civil liability

3 The auditor’s liability

Legal claims may be made against an auditor on a number of grounds.

The auditor may be prosecuted by the authorities for a criminal act, and be

criminally liable if found guilty. (The penalty may be a fine, or possibly

imprisonment for a guilty individual.)

The auditor may be liable under civil law. A ‘civil’ legal action may be brought

against an auditor by another person who has suffered loss or damage because

of the auditor’s actions. The person bringing the legal action usually seeks a

money payment (‘damages’) from the auditor, to recover their losses they have

suffered.

The precise details about an auditor’s criminal and civil liabilities vary from one

country to another, depending on national legislation. However, the general

position is described below.

3.1 Criminal liability

The auditor may be criminally liable in the following circumstances:

(1) Where he accepts appointment as auditor under a statutory provision without

being qualified to act.

(2) Where he is involved in fraud, such as falsifying accounting documents or

records.

(3) Where he is guilty of ‘insider dealing’. The criminal law of many countries

makes it an offence for a person with inside knowledge of price-sensitive

information to use or pass on that information. Insider dealing is also

prohibited under the IFAC and ACCA rules of professional conduct. Auditing

practices should take suitable steps to reduce the risk of insider dealing. For

example, it is normal practice for audit firms to impose restrictions on the

amount of shares that their staff may hold in client companies, and to require

staff to declare all their shareholdings. These procedures also help the audit

firm to ensure auditor independence.

(4) Criminal liability may also arise for certain offences relating to:

− the winding up of a company

− tax law

− financial services legislation, in areas such as dealing in investments or

giving investment advice.

− Money laundering (as discussed in Chapter 2)

Paper P7: Advanced audit and assurance (International)

68 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

3.2 Civil liability

A major threat faced by the auditing profession is the possibility of legal claims

against auditors as a result of negligent (or ‘careless’) auditing. The details of legal

liability vary from one country to another. The following discussion is intended to

give you an appreciation of the general legal principles involved, and is based on

English law.

For your examination, you should focus on the general principles, not the detailed

national rules. The legal cases described below show how the legal issues have

developed over time.

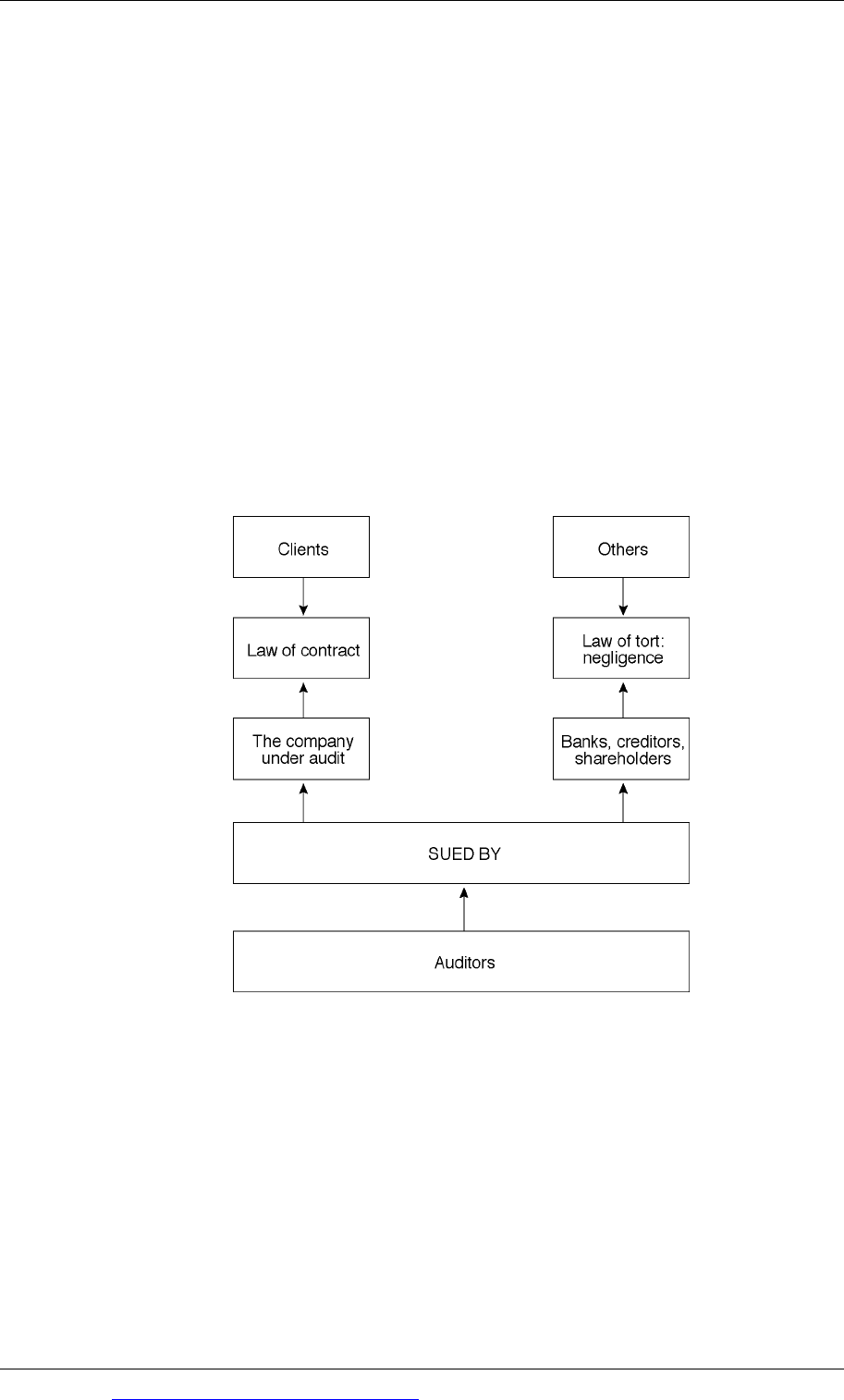

Contract law and the law of tort

Under English law, an auditor may face legal claims for losses suffered as a result of

negligent auditing under two separate branches of law: contract law and the law of

tort. A summary of the position is as follows:

Contract law

A company has a contract with its external auditor for the provision of audit

services. It can therefore sue the auditor for breach of contract if the auditor is

negligent in carrying out the terms of the contract.

Note that only the company can sue the auditor for a breach of contract. Other

persons who might want to sue an auditor, such as banks, creditors and

shareholders, do not have a contract with the auditor; therefore they cannot bring a

legal action under the law of contract.

Chapter 4: Professional responsibility and liability

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 69

When a legal action is brought against an auditor by a company for breach of

contract (negligence), the action is usually initiated by the board of directors of the

company.

Standards of skill and care

When carrying out their duties for a client, the auditors must exercise reasonable

care and skill. The ACCA’s Code of Ethics and Conduct require that members

should carry out their professional work with professional competence and due

care and with proper regard for the technical and professional standards expected

of them as members.

The degree of skill and care expected of an auditor in a particular situation depends

on the circumstances. There is no general standard of skill and care; the auditor is

expected to react to the situation and the particular circumstances that he is facing.

The case summarised below indicates the view that English courts have taken of the

degree of skill and care owed by an auditor to his client under contract law.

Re Thomas Gerrard & Son (1968)

The managing director of a company falsified the accounts in order to conceal

losses. As a consequence, dividends were paid (illegally) either wholly or partially

out of capital over a number of years. The managing director had done this by

including non-existing goods in inventory and by altering invoices. The auditors

discovered the altered invoices, but did not pursue the matter further. They

accepted assurances from the management that there was no problem.

The court’s decision. It was ‘held’ (decided) by the court that the discovery of the

altered invoices should have put the auditors on alert. Once they had made this

discovery they were no longer entitled to accept the assurances of the directors.

The auditors’ suspicions should have been aroused and enquiries should have

been made with suppliers, to verify the assurances given by the company’s

management. The auditors were therefore negligent.

In the absence of suspicious circumstances, the auditor is entitled to accept the

word of a responsible company official. But once an auditor’s suspicions have

been aroused, he has a duty to investigate the matter until it is satisfactorily

resolved.

In general, if the auditor has followed auditing standards and can demonstrate this

in his working papers, he will not usually be found guilty of negligence. This is why

it is so important for the auditor to ensure that he maintains adequate working

papers and obtains sufficient, relevant and reliable evidence to support his audit

opinion.

Paper P7: Advanced audit and assurance (International)

70 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Liability in tort

Only the client company can sue the auditor in the law of contract, because only the

company has a contract with the auditor. Others who feel they may have suffered as

a result of negligent auditing have to rely on a different branch of law – the law of

tort. An important question is: ‘To what extent can others rely on the civil law, and

bring an action for negligence against the auditors of a company?’

A tort can be defined as a ‘civil wrong’ other than that arising under contract law,

giving rise to a claim for damages. (A civil wrong is wrongdoing that is not a

criminal offence, but which allows the injured person to bring an action in civil law

against the wrongdoer.) Negligence is just one of many branches of tort.

Examples of other persons who may suffer loss because of an auditor’s negligence

and relying on financial statements that do not give a true and fair view are:

A bank that lends money to a company, and the company subsequently defaults

and fails to make payments of interest or repayments of the loan principal

A supplier who has given credit to the company, whose debts have to be written

off as ‘bad’.

Another company who relies on the financial statements when deciding to make

a takeover bid for the audited company.

An investor who relies on the financial statements to buy shares in the company,

and the share price falls when the true state of the company later becomes

apparent.

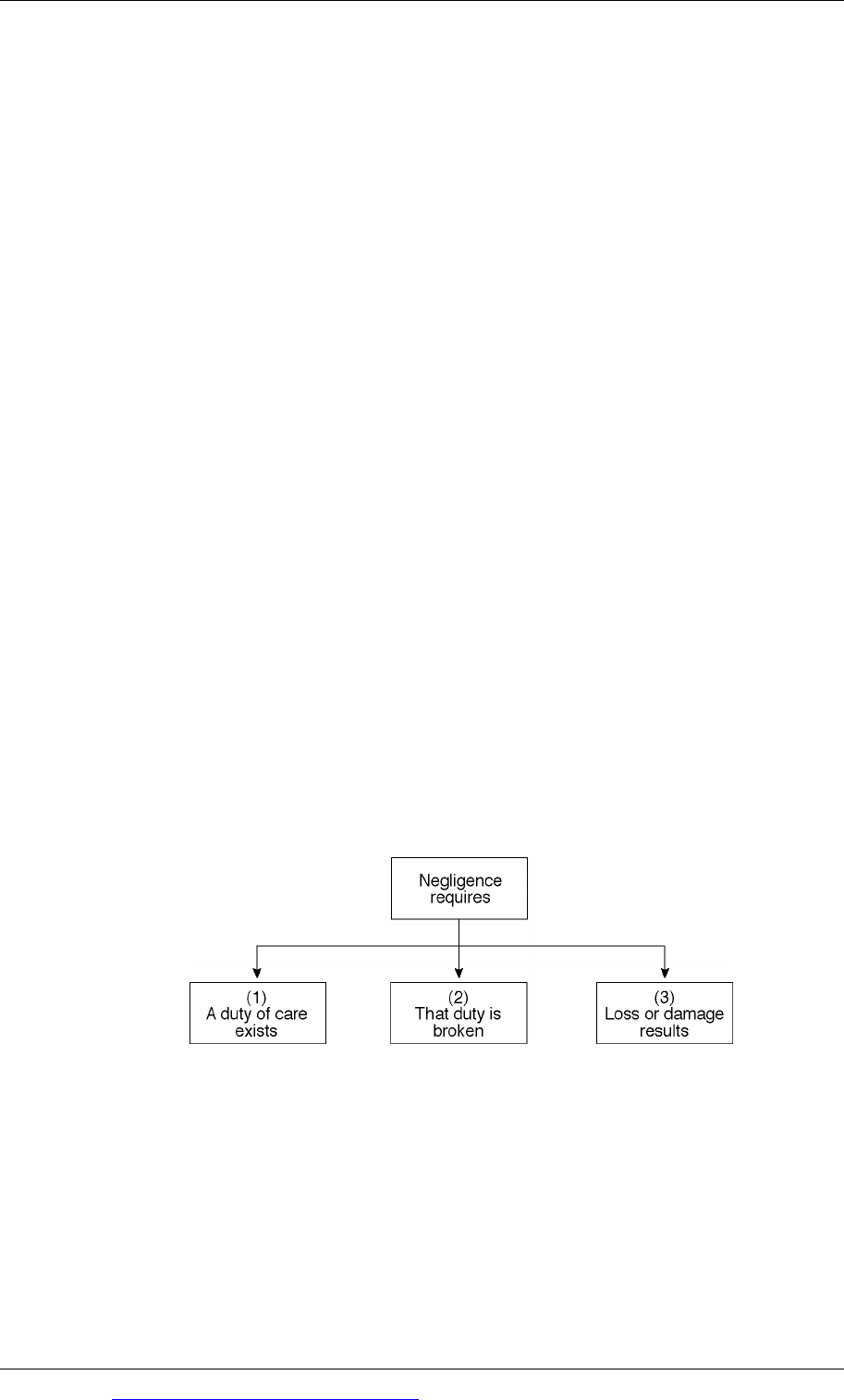

Making a successful claim for auditor negligence (law of tort)

If a person is to make a successful claim against the auditor in the tort of negligence,

three conditions must be satisfied.

Condition (1) – The auditor must owe a duty of care to the person who has

suffered a loss due to the auditor’s negligence. The existence of a duty of care

has proved the most troublesome of the three conditions to establish, in cases

brought before the courts. This is considered in more detail below.

Chapter 4: Professional responsibility and liability

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 71

Condition (2) – The duty of care must have been broken. The party bringing the

claim against the auditor has to show that the auditor did not exercise a

reasonable degree of care in the circumstances, so that the duty of care was

broken. A typical method used in court cases to prove that a duty has been

broken is to call another firm of auditors as expert witnesses. The expert

witnesses are asked to give their view on whether the audit was performed

correctly.

Condition (3) – A loss or damage must result from breach of the duty of care.

Proving that this condition has been met is usually a question of demonstrating

that the person making the claim suffered a financial loss as a result of the

negligent auditing. For example, if a bank lent money to a company on the basis

of audited accounts that were subsequently found to contain material errors or

omissions, and the company subsequently defaulted on its loan, the bank can

demonstrate a measurable financial loss.

Establishing the existence of a duty of care (law of tort)

Most of the major court cases on auditor negligence have been concerned with the

question of whether the auditor owes a duty of care to the ‘plaintiff’. (The plaintiff is

the person making the claim for damages.) The cases summarised below, taken

from UK law, show how the view of the courts on this question has developed over

time, since the 1950s.

You should concentrate on the principles involved, rather than the details of the

cases. Some of the cases do not deal specifically with auditors, but the principle

established by the court would be applicable to auditors in similar situations.

Candler v Crane Christmas (1951)

In this case, Candler sued the accountants Crane Christmas when he lost money

he had invested in a company. Crane Christmas had prepared the accounts, and

it was alleged that they had been negligent in doing so. But were the accountants

liable to Candler?

The court ruling was that although the accounts were negligently prepared,

Candler could not recover his losses from the accountants because he did not

have a contract with them.

Therefore, in the 1950s, the legal view was that an auditor did not owe a duty of

care to third parties who were not in a contractual relationship with the auditor.

Hedley Byrne v Heller & Partners (1964)

This is a case dealing with banks, but it was seen as relevant to all professionals,

including auditors and accountants. The plaintiff, Hedley Byrne, lost money

when a bank reference from the defendant (Heller & Partners, a bank) turned out

to have been negligently produced. The bank indicated in its reference that a

mutual client was a good credit risk when this was not the case.

The court ruled that although Hedley Byrne did not have a contract with the

bank, Heller & Partners, they could recover their losses due to the negligence and

Paper P7: Advanced audit and assurance (International)

72 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

loss involved, because the bank knew the plaintiff by name. However, the bank

did not have to pay any damages due to a general disclaimer in its letter (that

gave the reference) absolving it from any liability.

This legal decision affected auditors, because the court has decided that if a third

party (with whom the auditor did not have a contract) could show that it relied

on the work of an auditor which later turned out to be wrong, the auditor might

be liable for damages for negligence. However, this principle was only extended

to plaintiffs that the auditor actually knew by name. Unidentified third parties

were not able to claim against the auditor for negligence.

JEB Fasteners v Marks Bloom (1980)

In this case, the plaintiff acquired the share capital of a company. The audited

accounts, due to the negligence of the auditors, did not show a true and fair view

of the state of affairs of the company. It was accepted that, at the time of the audit,

the defendant auditors did know of the plaintiffs, but did not know that they

were contemplating a take-over bid.

Whilst recognising that the auditors owed a duty of care in this situation, the court

decided that the auditors were not liable because the plaintiff had not actually

suffered any loss. It was proved that the plaintiffs would have bought the share

capital of the company at the agreed price, no matter what the accounts of the

company had shown.

Caparo Industries v Dickman and Touche Ross & Co (1989)

This is seen as a leading case in English law in the area of ‘to whom does the auditor owe

a duty of care’.

Fidelity plc was taken over by Caparo Industries. Fidelity’s accounts had been

audited by Touche Ross. Caparo alleged that the accounts overstated the profits

of Fidelity plc and that they had relied on the audited accounts of Fidelity when

deciding to purchase shares in the company and make a takeover bid.

The court held that a duty of care was not owed to potential investors in a company,

or persons making a takeover bid, because of:

a lack of proximity (a lack of ‘closeness of relationship’) between the auditor

and a potential investor, and

the fact that it would not be just and reasonable to impose a duty on the

auditor to such investors.

In the above case, the court identified the auditor’s functions as being:

to protect the company itself from errors and wrongdoing; not to protect the

shareholders of the company from error, and

to provide shareholders with information such that they can scrutinise the

conduct of a company’s affairs and remove or reward those responsible (the

directors).

The auditor does not exist to aid investment decisions.

Chapter 4: Professional responsibility and liability

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 73

BBH v ADT (1995)

The former BDO Binder Hamlyn (BBH) partnership had audited the 1988/89

accounts of BSG. BSG had been acquired by ADT (an electronic security group)

for £105 million in 1990. BSG was later found to be worth only £40 million.

Usually, the auditors do not owe a duty of care to third parties. However, in this

case, one of the audit partners had verbally confirmed the accuracy of BSG’s

accounts during a meeting. At this point, the partner (and the firm) therefore

established a verbal contract with ADT.

In December 1995, ADT were awarded £65 million damages plus interest and

costs for negligence, against BBH. BBH appealed this decision and an out of court

settlement was reached with ADT.

Royal Bank of Scotland v Bannerman Johnstone Maclay [2002].

The ‘Bannerman case’ was a case in Scotland, but was considered to have legal

implications for and so is considered to have significant legal implications for

England and Wales too. Bannerman were the auditors of a company that had

arranged an overdraft facility with the bank. The overdraft arrangement included a

requirement for the company to send the bank a copy of its audited annual

accounts at the end of each year. The company became insolvent, owing a lot of

money to the bank. The bank claimed that it had relied on the auditors’ unqualified

opinion to continue providing the overdraft facility to the company. The audit firm

claimed that it had no duty of care to the bank. The court decided that although

there had been no direct contact between the audit firm and the bank, the auditors

would have known about the requirement in the overdraft facility arrangement.

This was knowledge they would have gained during the course of their audit work

was sufficient, in the absence of any disclaimer, to create a duty of care to the

bank. In the judge’s view, the absence of a disclaimer was a crucial feature of the

case.

Out-of-court settlements

Large claims against auditors in high-profile cases (such as Enron) receive a high

level of publicity. Many other cases are not widely publicised, often because they

are settled ‘out of court’. This involves the parties who are in dispute reaching a

negotiated settlement, rather than taking their case to court.

The advantages of out-of-court settlements are that:

it avoids the cost and time involved in a court case

it may avoid adverse publicity for the auditor

the final settlement may be lower (because both sides save legal costs, and the

plaintiff might agree to a lower settlement to avoid the cost and the risk of losing

the case).

Paper P7: Advanced audit and assurance (International)

74 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The disadvantages of out-of-court settlements are that:

the final responsibility may be left undecided, so the legal position remains

unclear

it may encourage others to take action against auditors

insurance premiums may rise (see below).

Example

An audit firm has been the auditor of Entity AZ for a number of years.

Its audit team has recently discovered that during that time, the managing director

of AZ has been consistently overvaluing inventories.

Entity B has recently purchased a major stake in Entity Z, relying on the audited

financial statements to do so.

Required

What possible defence might the audit firm use if it is sued by Entity B after a

successful takeover?

Answer

The audit firm can claim that it did not owe a duty of care to Entity B.

If the audit work has been performed to expected standards, the firm should be able

to claim that the audit work was performed with diligence and care, and in

accordance with ISAs. The audit work could not reasonably have detected the fraud

given its nature and the seniority of the individual committing the fraud.

The firm might also be able to claim that Entity B has not suffered any financial loss

as a result of its reliance on the audited financial statements.

Use of disclaimers in audit reports

A disclaimer is not a requirement of an audit report, but some audit reports include

one. A disclaimer states that:

the auditor’s report is intended for use of the company and the company’s

shareholders as a body, and

no responsibility is accepted by the auditor to anyone except the company or the

shareholders as a body for the content of the report.

The purpose of a disclaimer is to reduce the risk of legal claims by ‘third parties’

against the auditor for negligence.

The main problem with a disclaimer however is that in spite of the ruling in the

Bannerman case, a disclaimer cannot guarantee protection for an auditor against

third party claims, because the circumstances of each individual claim may be

different.