ACCA P7 (INT) Advanced Audit & Assurance - Study Text - 2010 (Emile Woolf Publishing)

Подождите немного. Документ загружается.

Chapter 6: The audit approach

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 115

Before the auditor can rely on the systems and controls that are in place, he must

establish what those systems and controls are, and carry out an evaluation of the

effectiveness of the controls.

3.2 What makes an effective system of internal controls?

ISA 315 identifies five elements which together make up an internal control system.

These are:

the control environment

the entity’s risk assessment process

the information system

control activities (internal controls)

the review and monitoring of controls.

3.3 The control environment

The ‘control environment’ is often referred to as the general ‘attitude’ to internal

control of management and employees in the organisation.

The control environment has been defined by the Institute of Internal Auditors as

follows: ‘the attitude and actions of the board [of directors] and management

regarding the significance of control within the organisation. The control

environment provides the discipline and structure for the achievement of the

primary objectives of the system of internal control. The control environment

includes the following elements:

integrity and ethical values

management’s philosophy and operating style

organisational structure

assignment of authority and responsibility

human resource policies and practice

competence of personnel.’

A strong control environment is typically one where management shows a high

level of commitment to establishing and operating sound controls.

The existence of a strong control environment cannot guarantee that controls are

operating effectively, but it is seen as a positive factor in the auditor’s risk

assessment process. Without a strong control environment, the control system as a

whole is likely to be weak.

Evaluating the control environment

ISA 315 requires auditors to gain an understanding of the control environment. Part

of this understanding involves the auditor evaluating the control environment, and

assessing its effectiveness.

Paper P7: Advanced audit and assurance (International)

116 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

In evaluating the control environment, the auditor should consider such factors as:

management participation in the control process, including participation by the

board of directors

management’s commitment to a control culture

the existence of an appropriate organisation structure with clear divisions of

authority and responsibility

an organisation culture that expects ethically-acceptable behaviour from its

managers and employees

appropriate human resource policies, covering recruitment, training,

development and motivation, which reflect a commitment to quality and

competence in the organisation.

3.4 The entity’s risk assessment process

Within a strong system of internal control, management should identify, assess and

manage business risks, on a continual basis. Significant business risks are any events

or omissions that may prevent the entity from achieving its objectives.

Identifying risks means recognising the existence of risks or potential risks.

Assessing the risks means deciding whether the risks are significant, and possibly

ranking risks in order of significance. Managing risks means developing and

implementing controls and other measures to deal with those risks.

ISA 315 requires the auditor to gain an understanding of these risk assessment

processes used by the client company’s management, to the extent that those risk

assessment processes may affect the financial reporting process.

The quality of the risk assessment and management process within the client

company can be used by the auditor to assess the overall level of audit risk. If

management has no such process in place, the auditor will need to do more work on

this aspect of the audit planning.

3.5 The information system

ISA 315 requires the auditor to gain an understanding of the business information

systems (including the accounting systems) used by management to the extent that

they may affect the financial reporting process.

This aspect of the auditor’s work will involve identifying and understanding the

following:

the entity’s principal business transactions

how these transactions and other events relevant to the financial reporting

process are ‘captured’ (identified and recorded) by the entity

the processing methods, both manual and electronic, applied to those

transactions

Chapter 6: The audit approach

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 117

the accounting records used, both manual and electronic, to support the figures

appearing in the financial statements

the processes used in the preparation of the financial statements.

The information system therefore consists of:

infrastructure (physical and hardware components) – manual accounting

systems may have little infrastructure.

software (in IT-based accounting systems)

people

procedures

data.

3.6 Control activities

Control activities are the practices and procedures, other than the control

environment, used to ensure that the entity’s objectives are achieved. They are the

application of internal controls.

Control activities are the specific procedures designed:

to prevent errors that may arise in processing information, or

to detect and correct errors that may arise in processing information.

Categories of control activities (internal controls)

Controls include the following types: (In the examination, if you are asked to

suggest suitable internal controls within a given system the items in this list should

provide a useful checklist.)

Authorisation controls. These require that all significant transactions must be

authorised by a manager at an appropriate level in the organisation.

Physical controls over assets. These are controls for safeguarding assets from

unauthorised use, or from theft or damage. An example is limiting access to

inventory areas to a restricted number of authorised personnel.

Arithmetic controls. These are checks on the arithmetical accuracy of

processing. An example is checking invoices from suppliers, to make sure that

the amount payable has been calculated correctly.

Accounting controls. These are controls that are provided within accounting

procedures to ensure the accuracy or completeness of records. An example is the

use of control account reconciliations to check the accuracy of total trade

receivables or total trade payables.

Management controls. These are controls applied by management. They include

supervision by management of the work of subordinates, management review of

performance and control reporting (including management accounting

techniques such as variance analysis).

Segregation of duties. This type of control is explained below.

Paper P7: Advanced audit and assurance (International)

118 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Segregation of duties

Segregation of duties means dividing the work to be done between two or more

individuals, so that the work done by one individual acts as a check on the work of

the others. This reduces the risk of error or fraud.

If several individuals are involved in the completion of an overall task, this

increases the likelihood that errors will be detected when they are made.

Individuals can often spot mistakes of other people more easily than they can

identify their own mistakes.

It is more difficult for a person to commit fraud, because a colleague may

identify suspicious transactions by a colleague who is trying to commit a fraud.

3.7 Monitoring of controls

It is important within an internal control system that management should review

and monitor the operation of the controls, on a systematic basis, to satisfy

themselves that the controls remain adequate and that they are being applied

properly. ISA 315 requires the auditor to obtain an understanding of this monitoring

process.

3.8 How the auditor uses internal controls

Most audits are, wherever possible, based on a systems-based approach. The

auditor relies on the accounting systems and the related controls to ensure that

transactions are properly recorded. The audit emphasis is therefore, as much as

possible, on the systems processing the transactions rather than on the transactions

themselves.

Understanding the controls

ISA 315 requires the auditor to:

gain an understanding of each of the five elements of the client’s internal control

system, and

document the relevant features of the control systems.

Once this understanding has been gained, the auditor should confirm that his

understanding is correct by performing ‘walk-through’ tests on each major type of

transaction (for example, sales transactions, purchase transactions, payroll).

Walk-through testing involves the auditor selecting a small sample of transactions

and following them through the various stages in their processing in order to

establish whether his understanding of the process is correct.

If he understands the controls that are in place, the auditor can go on to assess their

effectiveness, and the extent to which he can rely on those controls for the purpose

of the audit.

Chapter 6: The audit approach

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 119

Assessing the effectiveness of controls

The degree of effectiveness of an internal control system will depend on the

following two factors:

The design of the internal control system and the individual internal controls.

Is the control system able to prevent material misstatements, or is it able to

detect and correct material misstatements if they occur? Do the internal controls

appear to be adequate and effective ‘on paper’?

The proper implementation of the controls. Controls are not effective unless

they are implemented properly. So are the controls operated properly by the

client’s management and other employees?

The outcome of this evaluation helps the auditor to assess the control risk. This is

the risk that the internal controls will fail to prevent or detect and correct errors in

the financial statements. This evaluation will allow the auditor to decide on the

extent to which he can take a systems-based approach to the audit.

3.9 The auditor’s evaluation of internal controls

The auditor may judge that the control risk is high, or that the control risk is low

because the internal controls are effective.

If the auditor assesses the control risk as very high, he will probably take the

view that a systems-based audit approach will not be appropriate. He will

therefore move on to detailed testing of transactions and balances (and take a

substantive testing approach to the audit).

Before he can assess the control risk as low, the auditor must be satisfied that the

controls are well-designed and should be effective (in other words, they seem

effective ‘on paper’). Even if the controls appear to be acceptable on paper, the

auditor cannot rely on them and perform a systems-based audit unless he is

confident that the controls are actually working in practice. In this situation, the

next stage in the audit process is to carry out tests of controls.

If the outcome of the tests of control indicates that controls are actually operating

effectively, the audit can use a systems-based approach, with a reduced amount of

substantive testing. Even if the internal control system seems to be effective, the

auditor will never rely 100% on his assessment of the controls. He will always do

some substantive testing before reaching his conclusion about the financial

statements.

This is because of the limitations that are inherent in all control systems. It is

impossible to avoid the risk of control failure that is caused by:

human error (and a failure to apply a control properly)

over-riding of controls by management (which is a deliberate decision to ignore

a control), and

the possibility of collusion and fraud.

Paper P7: Advanced audit and assurance (International)

120 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Auditors will always supplement their work on systems with some substantive

testing. The amount of this testing will depend on the auditor’s evaluation of the

effectiveness of the controls.

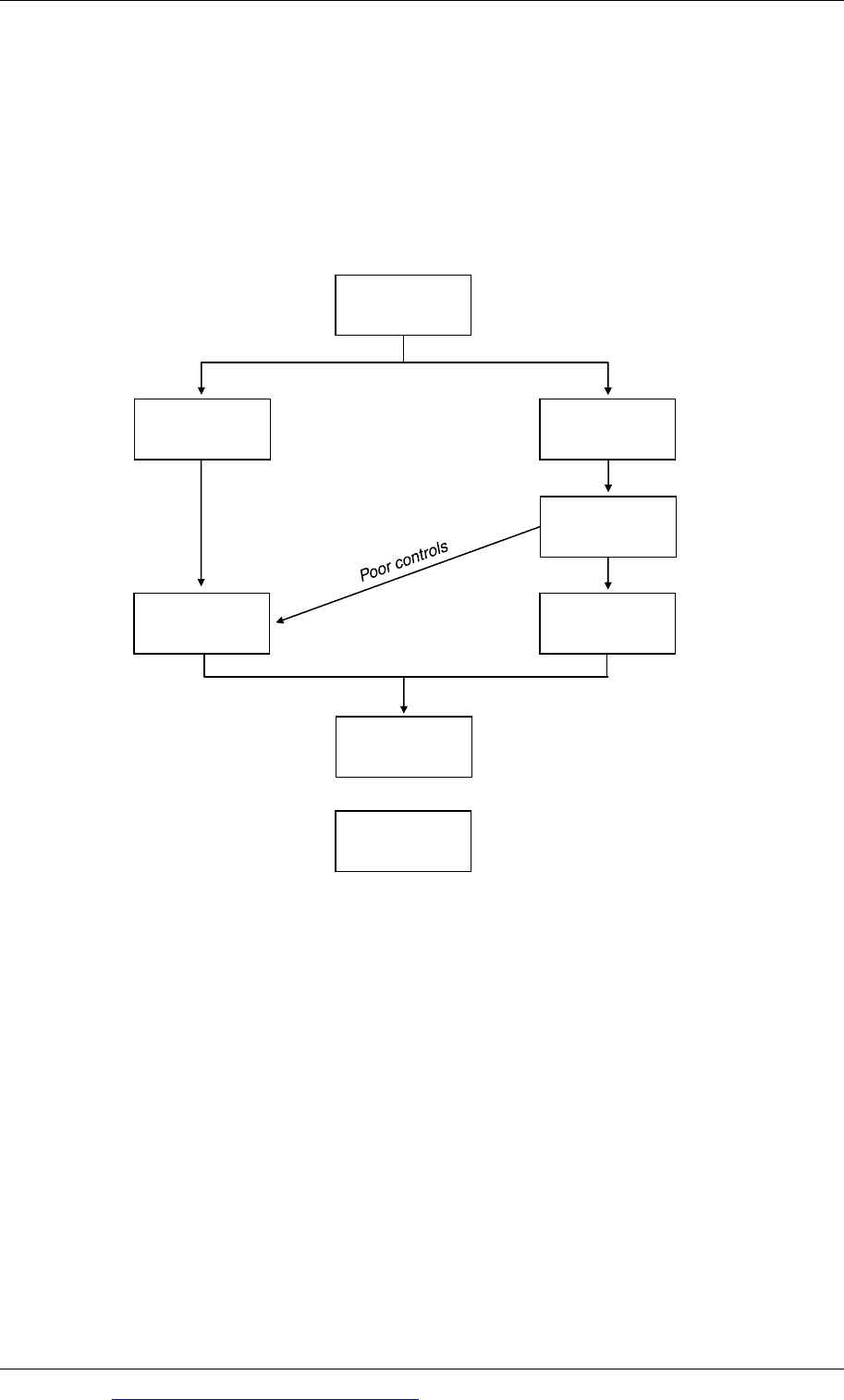

3.10 Summary of the approach to reliance on internal controls

The auditor’s use of a systems-based approach to an audit is summarised in the

following flowchart:

Planning and

risk assessment

Assessment of

internal controls

as weak

Extensive

substantive

testing

Overall review

of financial

statements

Assessment of

internal controls

as strong

Tests of controls

Reduced

substantive

testing

Issue audit

report

Good controls

Chapter 6: The audit approach

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 121

The statement of financial position approach

Substantive tests

The statement of financial position approach

Smaller entities

4 The statement of financial position approach

4.1 Substantive tests

When an auditor assesses the control risk as high, he will not be able to adopt a

systems-based approach to the audit. Instead he will carry out extensive substantive

testing.

Substantive tests are audit procedures performed to detect material misstatements

in the figures reported in the financial statements. They are designed to obtain

evidence about the financial statement assertions. They include:

tests of detail on transactions, account balances and disclosures, and

analytical procedures.

4.2 The statement of financial position approach

The statement of financial position approach is also an approach to the audit based

wholly on substantive testing. However, with this approach the auditor

concentrates primarily on:

testing balances, as opposed to

testing balances and transactions.

It is an approach that is often well-suited to small companies and to companies

where assets and liabilities are substantial in relation to transactions (e.g. investment

companies).

This approach is based on the following accounting equation:

Opening net assets + Profit for the year = Closing net assets

The theory is that if the opening and closing statements of financial position are

‘correct’ then the profit for the year must also be correct.

4.3 Smaller entities

ISAsapplytotheauditsofallentities–whatevertheirsize.However,additional

considerationsspecifictoauditsofsmallerentitiesareincludedwithinthe

applicationandotherexplanatorymaterialofaISAs,whereappropriate.These

Paper P7: Advanced audit and assurance (International)

122 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

additionalconsiderationsassistintheapplicationoftherequirementsoftheISAin

theauditofsuchentities.Theydonot,however,limitorreducetheresponsibilityof

theauditortoapplyandcomplywiththerequirementsoftheISAs.

TheIAASB’sGlossaryoftermsdefinesasmallerentityas

onewhichtypicallypossesses

thefollowingcharacteristics:

Concentration of ownership and management in a small number of individuals

(often a single owner-manager)

One or more of the following:

- Uncomplicated transactions

- Simple record-keeping

- Few lines of business/products

- Few internal controls

- Few levels of management with responsibility for a broad range of controls

- Few personnel, many having a wide range of duties.

Many of the control activities that would typically be found in a large company may

be inappropriate, too costly or impractical for a small entity. Segregation of duties is

an obvious example of this. Smaller entities do not have enough employees for an

‘ideal’ segregation of duties.

Often, control systems in smaller entities are based on a high level of involvement in

day-to-day operations by the directors or owners of the company. Authorisation

controls and review controls, with the owner-manager personally authorising many

transactions, might therefore be a key feature of the control systems in smaller

entities.

Although the active involvement of an owner-manager might mitigate risks arising

for a lack of segregation of duties, the auditor will often see the involvement of an

owner-manager in day-to-day operations as only a partial substitute for ‘normal’

control systems. The following problems may arise:

There may be a lack of evidence as to how systems are supposed to operate. The

auditor will need to rely more on enquiry than on review of documentation.

There may be a lack of evidence of the application of controls in practice (for

example, authorisations may not be documented).

Management may override whatever internal controls are in place.

Management may lack the expertise necessary to control the entity effectively.

There is unlikely to be any independent person within the management team as

there would be within “those charged with governance” in a larger entity.

The attitudes and actions of the owner-manager will be key to the auditor’s risk

assessment. There is unlikely to be a written code of conduct so a culture of integrity

and ethical behaviour, as demonstrated by management example, will be important.

Chapter 6: The audit approach

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 123

The auditor needs to understand and evaluate whatever controls are in place and

plan his audit work accordingly. However, it is likely that a lower level of reliance

will be placed on controls in a smaller entity, which means that a considerable

amount of substantive testing will be needed.

Paper P7: Advanced audit and assurance (International)

124 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP