ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Chapter 10: Non-current assets

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 263

It must be probable that expected future benefits will flow to the entity from the

asset.

The cost of the asset can be measured reliably.

An intangible asset must initially be recorded at cost. In subsequent periods, the

entity can choose from one of two valuation models:

cost model, or

revaluation model

If an intangible asset is accounted for using the revaluation model, all other

intangible assets in its class must also be re-valued.

In practice, the revaluation model is rarely used for intangibles, because IAS 38

requires that revaluation to fair value should be determined by an active market.

Given the unique characteristics of most intangible assets, an active market is

unlikely to exist – except perhaps for intangibles such as taxi licenses, fishing

licenses or production quotas.

3.3 Sources of intangibles

The recognition of intangible assets and measuring their cost can lead to some

accounting problems.

Separate acquisition

When an intangible asset is purchased as a separate item, the accounting treatment

is not controversial. The three requirements for recognition are always met. There is

a separate and identifiable asset, and a recognisable purchase cost. There has been a

transaction to acquire the intangible and so clearly it is expected that the transaction

will generate future economic benefits.

Note: When an intangible asset is acquired by purchase, its cost can usually be

measured reliably. The cost of a separately-acquired intangible, such as patent rights

or rights to ownership of a trademark, should comprise:

the purchase price, including import duties and non-refundable purchase tax,

plus

any directly attributable costs of preparing the asset for its intended use.

Acquisition as part of a business combination

An intangible asset may be acquired as part of the acquisition of a new subsidiary.

As a result of a business combination, the acquirer may pay more than the sum of

the fair value of the net assets of the subsidiary that is acquired. This may be

because the acquirer is gaining access to the goodwill (reputation) of the acquired

subsidiary, but it could also be to recognise the existence of intangibles that are not

reflected in the statement of financial position of the acquired subsidiary.

Examples might include customer lists, orders waiting to be fulfilled, established

customer relationships and non-competition agreements.

Paper P2: Corporate Reporting (International)

264 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

On acquisition of a subsidiary, these intangibles must be recognised separately from

the purchased goodwill, but only if the asset’s fair value can be measured reliably.

(The requirement that the intangible should probably provide future economic

benefits for recognition is always considered to be satisfied, because this probability

will be reflected in the fair value measurement of the intangible.)

IAS 38 argues that the fair value of intangibles acquired in this way can normally be

measured reliably. The only exception would be where the intangible arises from a

legal right or a contractual right, and either:

it is not separable (for example, it is a licence restricted to use by the entity only,

so that it cannot be sold as a separate item), or

it is separable, but there is no history or evidence of the exchange of similar

assets (in other words, it is a unique licence whose value cannot be measured

reliably).

Internally-generated intangible assets

Internally-generated goodwill must not be recognised as an asset. This is because it

is not identifiable (it is not separable from the entity) and reliable measurement

would not be possible.

However, development costs might be recognised as an internally-generated

intangible asset. Development costs are incurred at the end of a research and

development process, which happens in two phases:

a research phase, and

a development phase.

3.4 Research and development expenditure

Definitions

The term ‘research and development’ is commonly used to describe work on the

innovation, design, development and testing of new products, processes and

systems. IAS 38 makes a clear distinction between ‘research’ and ‘development’.

Research is defined as original and planned investigation undertaken to gain

new scientific knowledge and understanding.

Development is the application of research findings or other knowledge to a

plan or design for the production of new or substantially improved products,

processes, systems or services before the start of commercial production or use.

Accounting treatment of research costs

Expenditure on research should be recognised as an expense in profit or loss as it is

incurred. Research costs cannot be an intangible asset. (Any property, plant and

equipment used in research or on a research phase, such as laboratory equipment,

could be capitalised in accordance with IAS 16 and depreciated. The depreciation

charge is a revenue expense.)

Chapter 10: Non-current assets

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 265

Accounting treatment of development costs

Development costs should be recognised as an asset, but only if all the following

conditions

can be demonstrated:

It is technically feasible to complete the development project.

The entity intends to complete the development of the asset and then use or sell it.

The asset that is being developed is capable of being used or sold.

Future economic benefits can be generated. This might be proved by the

existence of a market for the asset’s output or the usefulness of the asset within

the entity itself.

Resources are available to complete the development project.

The development expenditure can be measured reliably (for example, via costing

records).

If any of these conditions are not met, the development expenditure should be

recognised as a revenue expense in profit or loss, and cannot be treated as an

intangible asset. Once such expenditure has been written off as an expense, it cannot

subsequently be reinstated as an intangible asset (for example, if all the conditions

are subsequently met for recognising the costs of the development work as an

intangible asset). Development costs must be capitalised, but only development

costs incurred after all the conditions for capitalisation as an intangible asset are met

Example

Entity Q has undertaken the following activities during Year 1:

(1) Training of sales staff at a cost of $50,000. Additional revenue as a result of

training the staff to a higher level of skill is expected to be in the region of

$500,000.

(2) Development of a new product. Total expenditure on development of the

product has been $800,000. All of the conditions for recognising the

development costs as an intangible asset have now been met. However,

$200,000 of the $800,000 was spent before it became clear that the project was

technically feasible, could be resourced and the developed product would be

saleable and profitable.

Required

Consider how the above amounts will be dealt with in the financial statements of

Entity Q for Year 1.

Answer

Training costs

. These must be written off as an expense in profit or loss as incurred.

The ‘asset’ (the training costs) is not controlled by Entity Q. The cost is controlled by

the staff who could leave at any time.

Development costs. The $200,000 must be written off as an expense in profit or loss.

The remaining $600,000 must be capitalised and recognised as an intangible asset

(development costs).

Paper P2: Corporate Reporting (International)

266 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Measurement of internally-generated intangibles

Intangible assets should be measured initially at their cost.

The cost of a purchased intangible asset is its purchase price.

The cost of an internally-generated intangible asset (such as development

expenditure) is the expenditure incurred from the date when the asset first meets

the recognition criteria. It should not include:

selling, administrative and other general overheads

training costs

advertising expenditure.

Measurement after initial recognition

As with IAS 16 and tangible non-current assets, having recognised an intangible

asset, the entity should then choose between:

the cost model, or

the revaluation model.

This is an accounting policy choice and the selected policy must be applied

consistently across each class of intangible assets.

Under the

cost model, assets are carried at cost minus any accumulated

amortisation and any accumulated impairment losses. Costs that may be capitalised

if they meet the above development criteria include:

costs of materials and services used

costs of employee benefits

fees to register a legal right, and

amortisation of patents and licenses that are used to generate the intangible

asset.

Under the

revaluation model assets are carried at fair value, minus any

accumulated amortisation and any accumulated impairment losses. Fair value must

be determined by reference to an

active market. Revaluations must be carried out

regularly, so that for any reporting period the carrying amount of the asset in the

statement of financial position is not materially different from its fair value.

An active market is defined as one where:

the items traded are homogenous

willing buyers and sellers can be found at any time, and

prices are available to the public.

If no such market exists for the intangible asset (and in practice, due to the unique

nature of intangibles, it rarely will exist) then the cost model must be adopted.

Chapter 10: Non-current assets

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 267

Website development costs and software development costs

SIC Interpretation 32 Intangible assets – website costs considers the accounting

treatment of development costs for a web site. The Interpretation states that the

development by an entity of its own website for internal or external access is an

internally-generated asset and should be accounted for in accordance with IAS 38.

This means that capitalisation should only occur if the development meets the

requirements for recognition listed above.

The most difficult item to ‘prove’ for the purpose of recognising the development

cost as an asset is the requirement that it will generate future economic benefits

from the website. A website that simply promotes and advertises its own products

and services does not meet this requirement, so the costs of developing the website

would have to be ‘expensed’ and written of to profit or loss as incurred. However a

website that allows customers to place orders will generate future benefits and so

the costs of its development should be capitalised.

If an entity has computer software that is essential to the operation of the computer

hardware (for example the operating system on a computer) the software should be

capitalised as part of the hardware cost in accordance with IAS 16. If the computer

software is a stand-alone package, it should be accounted for in accordance with

IAS 38.

3.5 Amortisation of intangible assets

An intangible asset, once recognised, should be amortised over its estimated useful

life, unless this is believed to be indefinite. When determining the useful life, it is

necessary to consider:

the expected usage by the entity

typical product life cycle for the asset

technical, technological or commercial obsolescence

the stability of the industry and changes in market demands

expected actions by competitors/ potential competitors

the level of maintenance to obtain future economic benefits

the period of control over the asset and any legal limits on its use (i.e. expiry

date of a patent agreement), and

whether the useful life of the asset is dependent on the useful life of other assets.

Given the rate of change in technology, computer software and many other

intangible assets are likely to have very short useful lives.

(Note: Purchased goodwill on the acquisition of a subsidiary is not amortised.

However, it is subject to impairment.)

Paper P2: Corporate Reporting (International)

268 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example

A broadcasting licence is renewable every ten years, on condition that the entity

provides a suitable level of service and complies with legislative requirements. The

licence may be renewed indefinitely at little cost and has been renewed twice before.

The current licence expires in five years and the entity intends to renew it

indefinitely. Evidence supports their ability to do so.

Required

Outline an appropriate amortisation policy for this intangible, explaining what

further information is required to support your decision.

Answer

The licence should not be amortised as it appears that the useful life is indefinite

and so it is expected to contribute to the entity’s cash flows indefinitely. As a result

of not being amortised, an annual impairment review must be conducted.

Further information required to support this conclusion:

Any difficulties renewing the licence in the past, which might indicate possible

problems in the future.

Any breach of service levels and legislative requirements which may jeopardise

applications to renew in the future.

Whether technology is expected to be replaced such that this licence is no longer

required or appropriate.

Chapter 10: Non-current assets

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 269

Impairment of assets (IAS 36)

Objective and scope of IAS 36

Identifying that an asset may have impaired

Measuring the recoverable amount

Recording the impairment

Cash generating units

4 Impairment of assets (IAS 36)

4.1 Objective and scope of IAS 36

The objective of IAS 36: Impairment of assets is to ensure that assets are ‘carried’ in

the financial statements at

no more than their recoverable amount.

The recoverable amount of an asset is defined as the higher of its:

fair value minus costs to sell, and

value in use.

Fair value less costs to sell is the amount obtainable from the sale of an asset in an

arm’s length transaction between knowledgeable, willing parties, less the costs of

disposal.

Value in use is the present value of future cash flows from using an asset, including

its eventual disposal.

IAS 36 applies to all assets, except for:

inventories (IAS 2)

deferred tax assets (IAS 12)

assets arising on a pension scheme (IAS 19)

financial instruments (IAS 39)

investment property that is measured at fair value (IAS 40)

biological assets measured at fair value (IAS 41)

assets held for sale (IFRS 5).

IAS 36 does cover impairments of property, plant and equipment and intangible

non-current assets, including purchased goodwill.

There are various stages in accounting for an impairment loss:

(1) Establish whether there is an indication of impairment.

(2) If so, assess the recoverable amount.

(3) Write down the affected asset (by the amount of the impairment) to its

recoverable amount.

Each of these stages will be considered in turn.

Paper P2: Corporate Reporting (International)

270 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

4.2 Identifying that an asset may have impaired

An entity is required to assess at the end of each reporting period whether there is

an indication that an asset may be impaired. If an indication of impairment is found,

then work must continue to ascertain the recoverable amount of the asset.

In addition, a calculation of the recoverable amount must take place annually,

regardless of any indications of impairment, for the following assets:

goodwill

intangible assets with a indefinite useful life

an intangible asset not yet brought into use (development costs that have been

capitalised, but where amortisation has not yet started).

Indicators of impairment

When assessing whether there is an indication of impairment, IAS 36 requires that,

as a minimum, the following sources are considered:

Sources of information indicating impairment

External sources Internal sources

An unexpected decline in the asset’s

market value.

Evidence that the asset is damaged

or no longer of use to the entity.

Significant changes in technology,

markets, economic factors or laws

and regulations that have an

adverse effect on the company.

There are plans to discontinue or

restructure the operation for which

the asset is currently used.

An increase in interest rates,

affecting the value in use of the

asset.

There is a reduction in the asset’s

expected remaining useful life.

The company’s net assets have a

higher carrying value than the

company’s market capitalisation

(which suggests that the assets are

over-valued in the statement of

financial position).

There is evidence that the entity’s

expected performance is worse than

expected.

4.3 Measuring the recoverable amount

An asset must be carried at no more than its recoverable amount. If the carrying

value is higher than the recoverable amount, the asset has suffered impairment and

must be written down. An asset is therefore carried in the statement of financial

position at the lower of:

its current carrying value, and

its recoverable amount.

But what is the ‘recoverable amount’ of an asset?

Chapter 10: Non-current assets

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 271

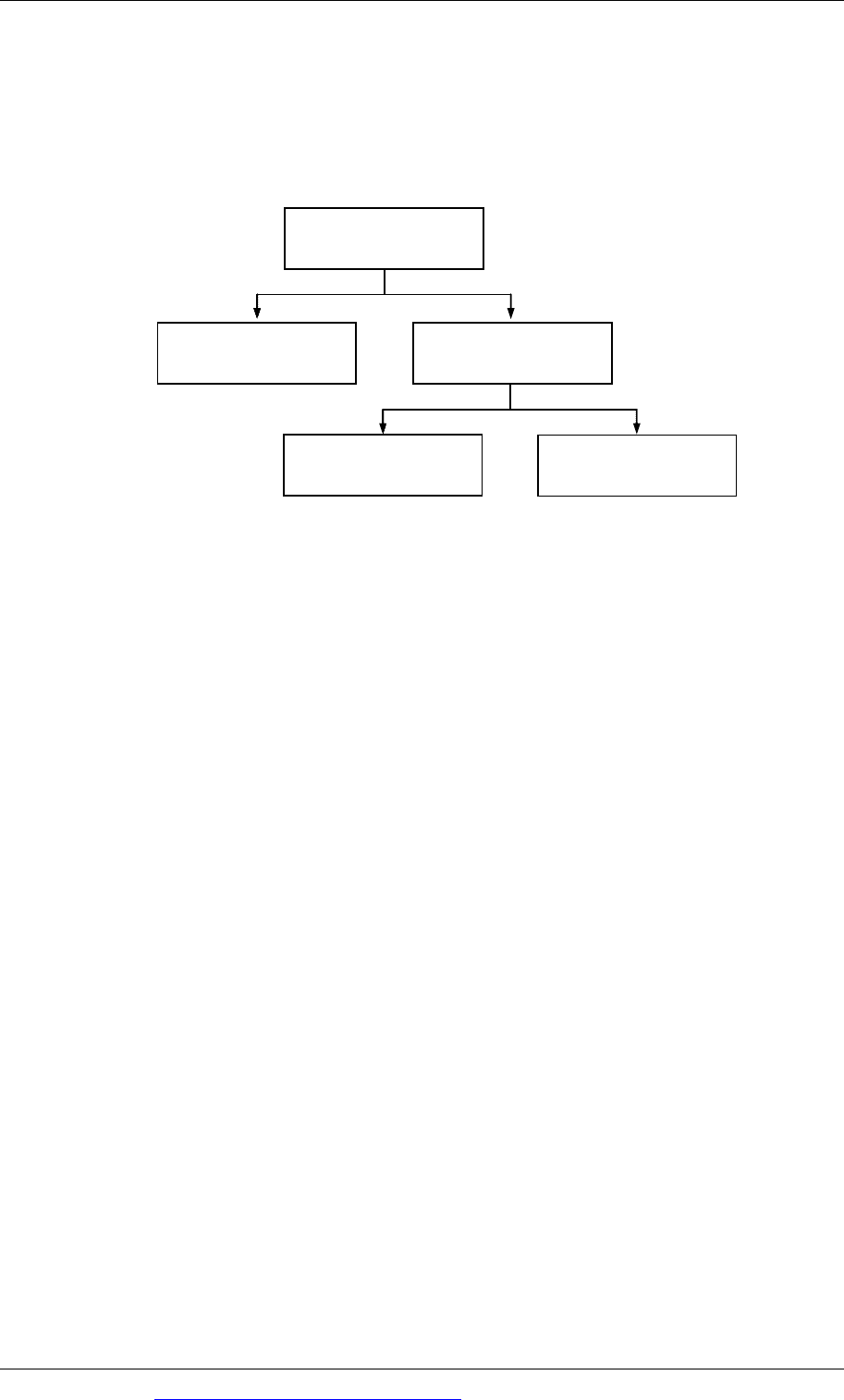

Recoverable amount is the higher of:

an asset’s fair value minus costs to sell, and

its value in use.

In summary:

Carrying value

Value at the lower of

Recoverable amount:

the higher of

Fair value less

costs to sell

Value in use

Fair value minus costs to sell

Fair value is normally market value. If no active market exists, it may be possible to

estimate the amount that the entity could obtain from the disposal.

Direct selling costs normally include legal costs and costs necessary to bring the

asset into a condition to be sold. However, redundancy and similar costs (for

example, where a business is reorganised following the disposal of an asset) are not

direct selling costs.

In determining fair value, the following sources should be used in descending

order:

(1) The price in a binding sales agreement between willing and unrelated parties.

(2) If (1) does not exist: the price at which someone is prepared to buy (‘bid price’)

in an active market.

(3) If (1) and (2) do not exist: an approximate value based on the most recent price

obtained in the market or based on other available information.

Value in use

Value in use is calculated by:

estimating future cash flows from the use of the asset (including those from

ultimate disposal)

discounting them to present value.

Estimates of future cash flows should be based on reasonable and supportable

assumptions that represent management’s best estimate of the economic conditions

that will exist over the remaining useful life of the asset.

Paper P2: Corporate Reporting (International)

272 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The net present value is derived by discounting back the future operating cash

flows at the risk-free market rate of interest.

Example

A company has a machine in its statement of financial position with a net book

value of $300,000. The machine is used to manufacture the company’s best-selling

product range, but the entry of a new competitor to the market has severely affected

sales. As a result, the company believes that the future sales of the product over the

next three years will be only $150,000, $100,000 and $50,000. The asset will then be

sold for $25,000. An offer has been received to buy the machine immediately for

$240,000, but the company would have to pay shipping costs of $5,000.

The risk-free market rate of interest is 10%.

Market changes indicate that the asset may be impaired and so the recoverable

amount for the asset must be calculated.

Fair value minus costs to sell is $235,000 ($240,000 fair value minus $5,000

disposal costs)

Value in use is the discounted future cash flows from keeping the asset. This is:

150,000

1.1

+

100,000

1.1

2

+

50,000

+

25,000

()

1.1

3

= $275, 357

The recoverable amount is the higher of (1) value in use and (2) fair value minus

costs to sell. In this example, this is $275,357 (the higher of

$235,000 and $275,357).

The asset has a carrying value of $300,000, which is higher than the recoverable

amount from using the asset. The asset should be valued at the lower of carrying

value and recoverable amount. It must therefore be written down to the recoverable

amount, and an impairment of $24,643 must be recorded. (Impairment = $300,000 –

$275,357.)

4.4 Recording the impairment

The impairment loss should normally be recognised immediately in profit or loss.

However, if the impairment relates to a re-valued asset, it is treated as other

comprehensive income and (as a downward revaluation) the impairment loss

should be set against the revaluation reserve balance relating to that asset. If there is

any excess impairment, this should be charged to profit or loss.

Following the recognition of the impairment, the future depreciation of the asset

should be based on the revised carrying amount, minus the residual value, over the

remaining useful life.