ACCA P1 Governance, Risk and Ethics - 2011 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Paper P1: Governance, risk and ethics

344 © Emile Woolf Publishing Limited

the balanced scorecard and sustainability balanced scorecard

the sustainability assessment model (SAM) and full-cost accounting (FCA).

2.4 ‘Environmental footprint’ for individual companies

It is possible to talk about an environmental footprint for individual companies

rather than countries, although not as common. A company can measure its

environmental footprint through a series of measurements. The measurements

appropriate for each individual company might vary according to the nature of its

operations, but should relate to the following environmental issues:

the company’s consumption of materials subject to depletion (such as quantities

of livestock, timber or non-farmed fish) and non-renewable resources (such as

oil, natural gas and coal): also the company’s use of other key resources such as

land

the pollution created by the company’s activities, measured for example in terms

of emissions of carbon dioxide, chemical waste or spillages of oil

an assessment, in either qualitative or quantitative terms, of the broader effect of

the company’s resource consumption and pollution on the environment.

2.5 Triple bottom line reporting

The term ‘triple bottom line’ was ‘invented’ in 1994 by J Elkington. Its aim is to

encourage companies to recognise social and environmental issues in their business

models and reporting systems. This method of reporting is encouraged by the

Global Reporting Initiative (GRI), an internationally-recognised body that promotes

sustainability reporting.

The ‘triple bottom line’ gets its name because companies report their performance

not simple in terms of profit: they provide key measurements for three aspects of

performance:

economic indicators

environmental indicators, and

social indicators.

Triple bottom line reporting is therefore providing a quantitative summary of a

company’s economic environmental and social performance over the previous year.

Economic indicators will include measurements relating to:

sales revenue

profits, earnings and earnings per share

dividends per share

global market share (as a % of the total market)

in some industries, such as car production, units of sale worldwide.

Chapter 16: Social and environmental issues in ethics and business

© Emile Woolf Publishing Limited 345

Environmental indicators might include measurements relating to:

reducing the ‘intensity’ of materials in products and services

reducing energy intensity

minimising the release of toxic materials/pollutants

improving the ability to recycle material

maximising the use of renewable resources

extending the life of a product.

Example

One major global company using triple bottom line reporting reported its

environmental performance in terms of:

global energy use, measured in thousand of GWh

global carbon dioxide emissions, measured in metric tons

production of non-recycled waste, measured in metric tonnes

the number of manufacturing sites that had been awarded an ISO 14000

certificate (which is explained later).

The same company reported, as social indicators:

its donations to communities and sponsorships, measured in US dollars

diversity: the percentage of its employees who were female and the percentage

who came from minority groups

the number of discrimination charges brought against the company during the

year

employee satisfaction, based on a census of employee opinion

the recordable injury rate per 1,000 employees.

Weaknesses in triple bottom line reporting

There are several weaknesses with triple bottom line reporting.

There are no widely-established standards for triple bottom line reporting, and

no standard methods for measuring social and environmental impacts. It is

therefore usual to compare the sustainability of one company with the

sustainability of another. (The work of the Global Research Initiative or GRI is to

standardise measurements for the triple bottom line. It has been publishing

Sustainability Reporting Guidelines since 1999. These were updated and

amended in 2002.)

If the social and environmental measures are not subject to independent audit,

there might be doubts about the reliability of the data presented in a company’s

report.

Paper P1: Governance, risk and ethics

346 © Emile Woolf Publishing Limited

2.6 Balanced scorecard and sustainable balanced scorecard

The concept of the balanced scorecard was suggested by Kaplan and Norton in the

1990s, as a method of setting targets and measuring performance, for both entire

companies and individual managers within a company.

The balanced scorecard is a ‘strategy map’ divided into four element or

perspectives:

a financial perspective

a customer perspective

an internal perspective (operations)

an innovation and learning perspective.

For each perspective, goals, targets and tasks are established, with indicators of

performance for comparing actual results against the target. The purpose of a

balanced scorecard is to prevent management from directing all their attention to

short-term financial considerations. The four perspectives give suitable importance

to short-term profitability, but also provide for non-financial and longer-term

strategic issues.

A sustainable balanced scorecard has been developed by Moller and Schaltegger.

This adds a ‘non-market’ perspective to the balanced scorecard, for the

environmental and social impacts of the company’s operations or the manager’s

activities. This type of scorecard therefore includes an element of accounting for

sustainability.

2.7 Sustainability Assessment Model (SAM) and full-cost accounting (FCA)

The Sustainability Assessment Model (SAM) measures the impacts on sustainability

of a product over its full life cycle, from raw material extraction through the

production process to its final consumption. These impacts:

the direct economic cost of the product, but also

the direct impact of the company’s operations on society and the environment,

and also

the broader social costs and benefits.

The total impacts are measured as a cost, known as full cost, and the measurement

system supporting the Sustainability Assessment Model is called full-cost

accounting or FCA, because it includes environmental and social costs as well as

economic costs.

The SAM is also used to measure the performance of a company on an index of

sustainability (SAMi). This measures the percentage distance that the company is

from achieving sustainability.

The SAM and FCA approach

The SAM is a four-step approach to measuring the impacts of a project or product

over its entire life cycle, from cradle to grave.

Chapter 16: Social and environmental issues in ethics and business

© Emile Woolf Publishing Limited 347

Step 1. A SAM exercise is established. The object of the exercise is identified, that

will be subjected to evaluation. This might be a product, a process, a part of an

entity’s operations or the whole of its operations.

Step 2. The boundaries of the SAM evaluation are defined. All the costs and

benefits to be included, including environmental and social costs or benefits, are

identified over the full life cycle of the product (or other object of the exercise).

Step 3. The impacts of the product are measured under four headings:

- economic

- resource use

- environmental

- social.

Some of these measurements might be in money terms, but many of the costs

and benefits will be non-monetary measures, including physical (environmental)

measures.

Typically, the economic impacts and social impacts should normally be positive

(benefits), whereas the resource use and environmental impacts are negative.

Step 4. These non-monetary measures are converted into a common basis of

measurement: money. This total money measurement provides the full cost

analysis of the product, process or operation.

‘None of these steps is easy to do and a great deal of judgement will be exercised at

each stage…. While at some levels FCA appears to be conceptually straightforward,

it is not an easy technique to develop and use in practice. In particular, FCA requires

substantial amounts of physical data about the object of the exercise and requires

extensive modelling of complex real-world relationships. The data required for FCA

is usually only available in organisations that are at the forefront in responding to

the environmental agenda’ (Bebbington, Gray, Hibbitt and Kirk, 2001). The main

problem is deciding how to convert the physical measurements of environmental

impacts into money measures.

Making use of FCA

Full-cost analysis might show the entire cost of a product or an activity, including its

social and environmental impacts (or ‘externalities’). However, it might have

benefits for strategic planning in companies where it might be expected that in

future companies might be required to pay for its ‘externalities’, so that the

‘externalities’ become internal costs.

For example, companies might in the future be required to pay for their impact on

the environment by:

paying a carbon tax for their carbon emissions

having to take back products from customers at the end of their useful life, for

recycling or disposing of the materials

having to comply with stricter environmental standards.

Companies that are aware of the full costs incurred by their products should be in a

better position than other companies to plan reductions in those costs, by acting

now to reduce carbon emissions, improve environmental standards and so on.

Paper P1: Governance, risk and ethics

348 © Emile Woolf Publishing Limited

2.8 Sustainability reporting: concluding remarks

For various reasons, companies are increasingly producing sustainability reports in

one form or another. The reasons that seem to be persuading companies to report on

sustainability include competition, risk management, emerging markets, corporate

reputation and, in some countries, mandatory minimum reporting requirements.

However, there is (as yet) no universal agreement about the meaning of

sustainability, which acts as a restraint on the development of suitable reporting.

Chapter 16: Social and environmental issues in ethics and business

© Emile Woolf Publishing Limited 349

Environmental management systems, environmental management

accounting and environmental audit

Environmental management systems: ISO 14000 and EMAS

Environmental management accounting (EMA)

EMA techniques

Social and environmental reporting

Social and environmental audit / environmental audit

3 Environmental management systems, environmental

management accounting and environmental audit

3.1 Environmental management systems: ISO 14000 and EMAS

An environmental management system is a broad general term for any system used

by an entity to monitor and manage the impact that its products and operations

have on the environment. The aims of a management system might be to:

minimise the negative impact of operations on the environment (damage to air,

water or land)

comply with environmental laws and regulations

make continual improvements in either of the above areas.

An environmental management system includes an environmental information

system. Information is needed to:

monitor compliance with environmental laws and regulations, and/or

monitor the implementation of the company’s own environmental policies.

An information system may provide, for example, information about physical

quantities of emissions of waste or toxic materials, resources in the environment, the

environmental characteristics of the company’s products or services, information

about environmental ‘incidents’ such as spillages of waste or toxic materials.

Guidance for companies in the structuring and operating of an environment

management system is provided by a number of international.

ISO 14000

The International Standards Organisation (ISO) has issued a series of standards on

environmental management systems, known as the ISO 14000 series of standards.

They are standards that specify a process for managing, controlling and improving

an entity’s environmental performance.

Paper P1: Governance, risk and ethics

350 © Emile Woolf Publishing Limited

They specify an environmental management system, provide guidance for using the

system and explain how a company’s environmental management system can be

audited and receive an ISO 14000 certification.

ISO 14001, one of the standards in the 14000 series, provides general guidance on:

the general requirements for an environmental management system

environmental policy: an entity must have an environmental policy in existence,

as a condition of meeting ISO 14000 requirements

planning: an entity should declare its main environmental objectives, which

should be primary areas of planning the company’s environmental programme

and improvement process

implementation and operation: a system must establish procedures, work

instructions and controls to ensure that the environmental policy is implemented

and the planning targets are achieved

checking and corrective/control actions

management review: there should be a regular review of the environmental

management system to ensure that it is suitable (for the entity and its objectives)

and effective in operation.

The standard can be applied by any company in any industry, any where in the

world. Companies wishing to obtain ISO 14000 certification will be audited against

the requirements of this standard. Having obtained the certificate, companies will

be subject to regular audits to ensure that they are maintaining compliance with the

requirements of ISO 14000.

Another standard in the series, ISO 14004, provides more detailed guidance,

including guidance on how to take a structured approach to setting environmental

targets and objectives and establishing and implementing a system for monitoring

and control.

Companies that apply ISO 14000 and obtain ISO 14000 certification will therefore

have a management system for:

identifying the aspects of its business that have an impact on the environment

monitoring changes in legislation and regulation on environmental issues

producing objectives/targets for improvement

planning to achieve these improvements, and

conducting regular reviews for continual improvement.

ISO 14000 does not specify targets for achievement or standards of environmental

performance. It provides guidance on a management system for the management of

environmental issues.

The benefits of obtaining an ISO 14000 certificate

Companies must be ‘audited’ by an independent external expert before they are

awarded an ISO 14000 certificate. Having obtained a certificate, they are therefore

Chapter 16: Social and environmental issues in ethics and business

© Emile Woolf Publishing Limited 351

able to provide an assurance that the company has an active concern for

environmental issues to:

employees, and

individuals and groups outside the company, such as the government, the

public, customers and investors/shareholders.

Certification also allows companies to make validated claims about the

environmental effect (‘environmental-friendliness’) of their products.

EMAS

EMAS is the Eco-Management and Audit Scheme. It is a scheme operated by the

European Union which recognises companies that are continually improving their

environmental performance. Organisations registered with EMAS comply with law,

run an environment management system and publish environmental statements

which are independently-verified.

EMAS is very similar in concept to ISO 14000.

3.2 Environmental management accounting (EMA)

Management accounting is concerned with the provision of information to

management, to help management make decisions. Environmental management

accounting has the same purpose, but it identifies environmental costs and benefits,

which might be measured in either physical terms or money terms.

Environmental management accounting (EMA) provides information that supports

the operation of an environmental management system. It provides managers with

financial and non-financial information to support their environmental management

decision-making. EMA complements other ‘conventional’ management accounting

methods, and does not replace them.

The main applications of EMA are for:

estimating annual environmental costs (for example, costs of waste control)

budgeting and setting targets for improvements in environmental performance

product pricing

investment appraisal (for example, estimating clean-up costs at the end of a

project life and assessing the environmental costs of a project)

identifying opportunities for cost savings

estimating savings from environmental projects.

Although environmental management accounting information is intended for use

mainly by management, it is also included in reports that the entity publishes

externally, such as sustainability reports/environment reports.

Paper P1: Governance, risk and ethics

352 © Emile Woolf Publishing Limited

Example

Environmental management accounting can be used to identify opportunities for

cost savings.

An example might be the assessment of a proposal to replace the use of toxic

materials with a non-toxic alternative material that has a higher purchase cost from

the supplier.

An analysis of environmental costs might show that the company would benefit

from a switch to non-toxic materials in the form of:

removing the cost of having to make reports to the regulatory authorities on

toxic materials, and

a reduction in materials handling costs.

The benefits might exceed the higher costs of the non-toxic materials.

Environmental management accounting is also used in the assessment of using

recycled materials and making constructive use of ‘waste’ materials.

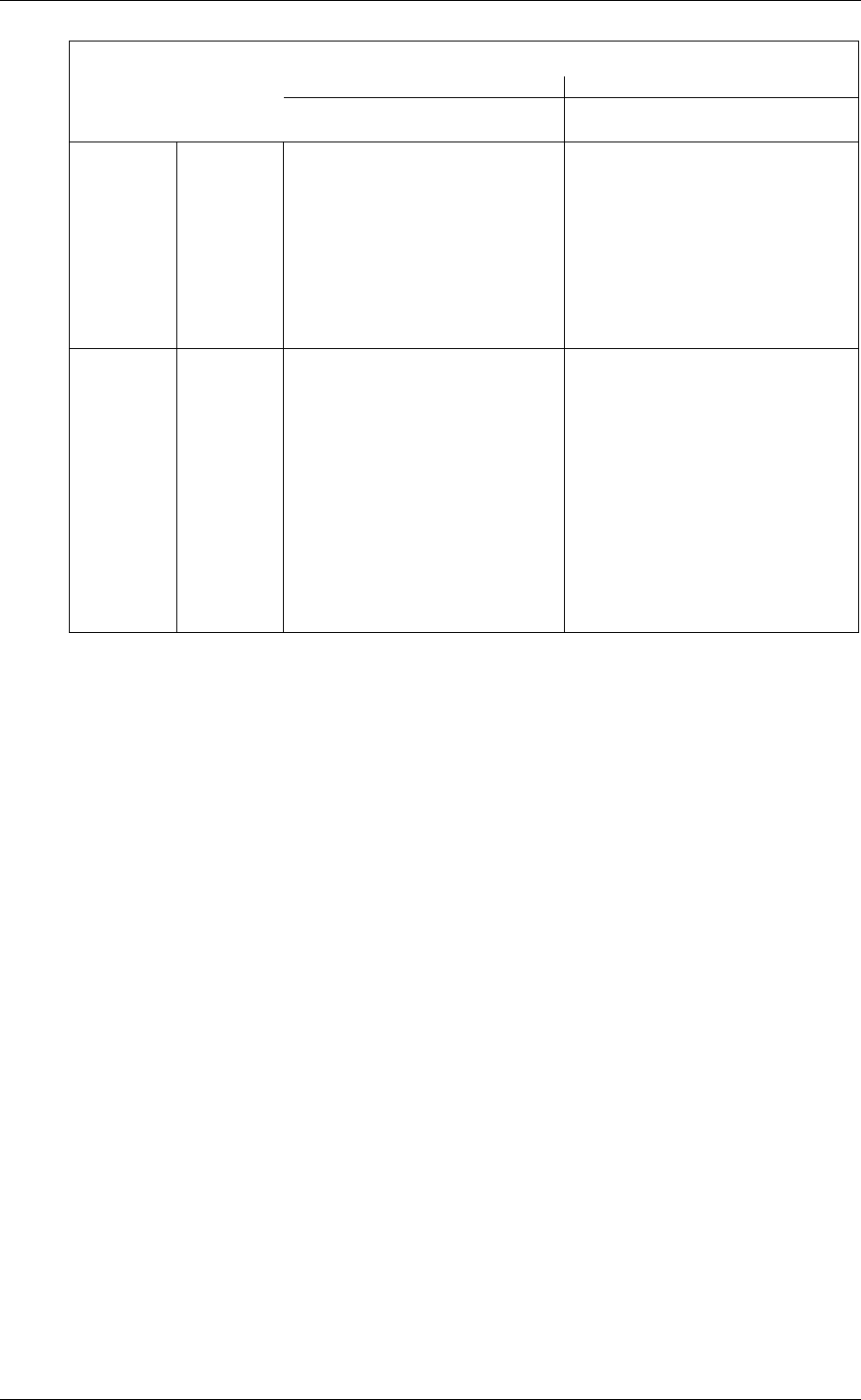

A framework for environmental management accounting

Burritt et al (2001) suggested a framework for EMA based on providing information

to management:

that is gathered from internal or external sources

as monetary or physical measurements: physical measures of energy

consumption, pollution and so on can be converted into a monetary measure

as historical or forward-looking information

where the focus is short-term or longer-term

that consists of routine reports or ad hoc information.

Four of these elements of EMA are shown in the following table.

Chapter 16: Social and environmental issues in ethics and business

© Emile Woolf Publishing Limited 353

Environmental management accounting (EMA)

Monetary EMA Physical EMA

Short-term

focus

Long-term

focus

Short-term

focus

Long-term

focus

Historical

orientation

Routine

reporting

Environmental

cost

accounting

Analysis of

environmentally-

induced capital

expenditures

Material and

energy flow

accounting

Accounting for

environmental

capital impacts

Ad hoc

(one-off)

information

Historical

assessment of

environmental

decisions

Environmental

life cycle

costing,

environmental

target costing

Historical

assessment of

short-term

environmental

impacts, e.g. of

a site or product

Post-investment

assessment of

environmental

impacts of

capital

expenditures

Future

orientation

Routine

reporting

Environmental

operational

budgets and

capital

budgets

(monetary

reporting)

Environmental

long-term

financial

planning

Environmental

long-term

physical

planning

Ad hoc

(one-off)

information

Relevant

environmental

costing (e.g.

special orders)

Environmental

life cycle

budgeting and

target costing

Assessment of

environmental

impacts

Physical

environmental

investment

appraisal.

Specific project

life cycle

analysis

3.3 EMA techniques

Environmental management accounting techniques include:

re-defining costs

input-output analysis

environmental activity-based accounting

environmental life cycle costing.

Re-defining costs

The US Environmental Protection Agency (1998) suggested terminology for

environmental costing that distinguishes between:

conventional costs: these are environmental costs of materials and energy that

have environmental relevance and that can be ‘captured’ in costing systems

potentially hidden costs: these are environmental costs that might get lost within

the general heading of ‘overheads’

contingent costs: these are costs that might be incurred at a future date, such as

clean-up costs

image and relationship costs: these are costs associated with promoting an

environmental image, such as the cost of producing environmental reports.

There are also costs of behaving in an environmentally irresponsible way, such

as the costs of lost sales as a result of causing a major environmental disaster.