ACCA F9 Financial Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 16: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 295

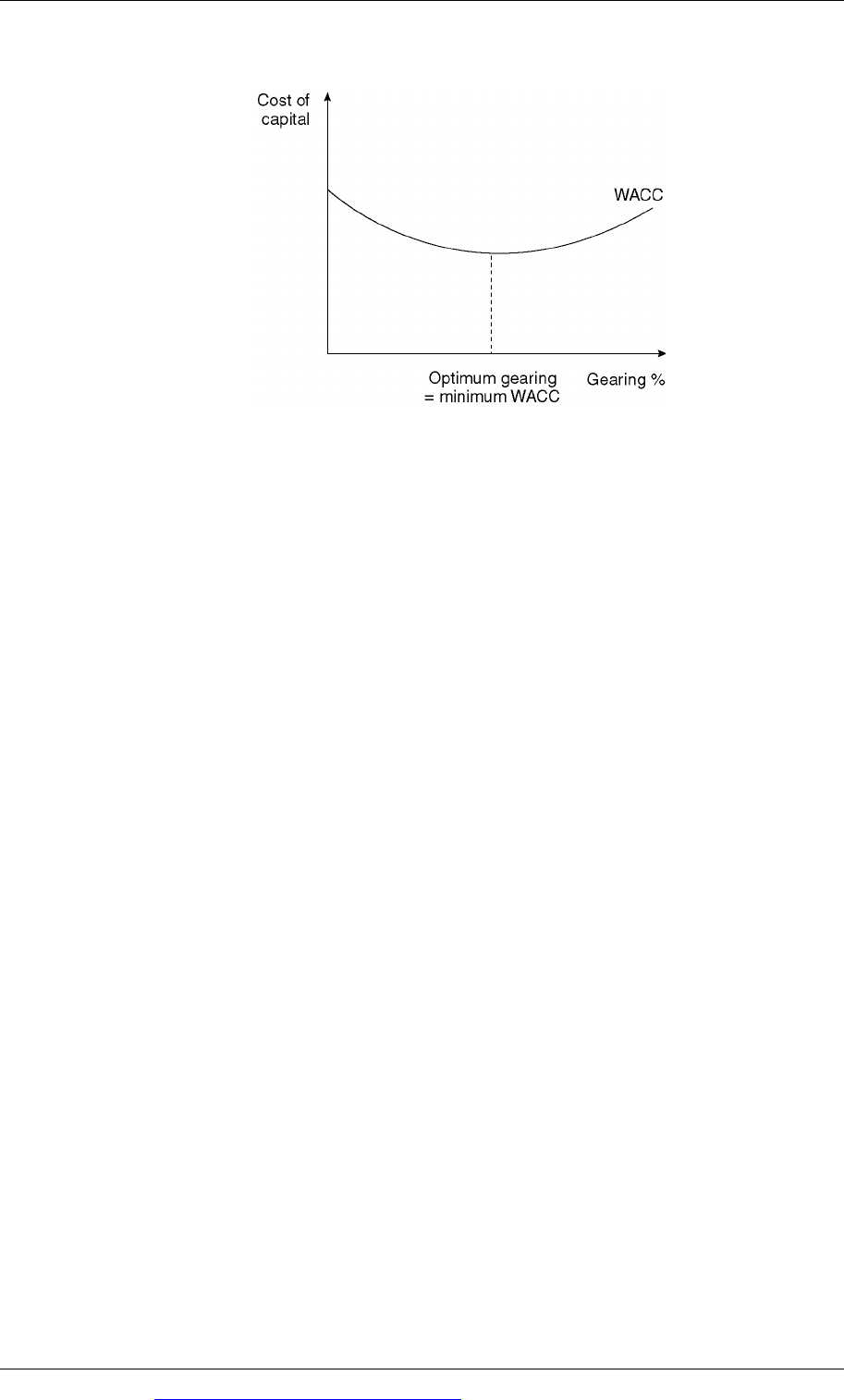

Traditional view of gearing and the WACC

The greatest weakness with traditional theory is that it is based on assumptions and

observation. It does not provide any guidance about how to identify or calculate:

the level of gearing where WACC is minimised, or

the WACC at the optimal gearing level.

5.2 The Modigliani-Miller view: ignoring corporate taxation

The traditional view of gearing and WACC was challenged by Modigliani and

Miller (MM) in the 1950s. Initially, their arguments were based on the assumption

that corporate taxation, and the tax relief on interest, could be ignored.

You do not need to know Modigliani and Miller’s arguments in detail, only the

main assumptions on which their arguments were based and the conclusions they

reached.

Assumptions

MM made several assumptions in making their propositions.

There is a perfect capital market in which investors all have the same

information and also act rationally. Consequently they all share the same

expectations about the future earnings of a company and also the level of its

business risk.

There is no taxation.

Debt is risk-free and freely-available to both companies and investors.

There are no transaction costs involved in buying or selling shares or debt

capital.

It is not possible to explain properly the relevance of the assumptions about risk-

free debt, its availability and the absence of transaction costs in buying and selling

shares. These assumptions were used by MM to justify their views and explain how

investors were indifferent to the gearing of companies because they are able to

adjust their own personal gearing by borrowing and buying or selling shares.

Paper F9: Financial management

296 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Modigliani and Miller’s propositions: ignoring taxation

MM argued that if corporate taxation is ignored, an increase in financial gearing will

have the following effect:

As the level of gearing increases, there is a greater proportion of cheaper debt

capital in the capital structure of the firm.

However, the cost of equity rises as gearing increases.

As gearing increases, the net effect of the greater proportion of cheaper debt and

the higher cost of equity is that the WACC remains unchanged. The effect of the

higher cost of equity is exactly equal to the offsetting effect of having a larger

proportion of debt capital in the capital structure.

The WACC is the same at all levels of financial gearing.

The total value of the company (equity + debt capital) is therefore the same at

all levels of financial gearing.

Modigliani and Miller therefore reached the conclusion that the level of gearing is

irrelevant for the value of a company. There is no optimum level of gearing that a

company should be trying to achieve.

Modigliani-Miller view of gearing and the WACC: no taxation

MM’s theory is sometimes called the ‘net operating income’ approach because MM

argued that, in the absence of taxation, the total market value of a company is

determined by just two factors:

The total earnings of the company (profit after interest, if tax is ignored).

The business risk of the company, which determines the WACC. WACC is not

affected by financial gearing, but it is affected by the perceived business risk of

investing in the company. WACC is higher for companies with higher business

risk.

Modigliani-Miller formulae: no taxation

There are three formulae for the Modigliani and Miller theory, ignoring corporate

taxation. These are shown below. The letter ‘

U

’ refers to an ungeared company (all-

equity company) and the letter ‘

G

’ refers to a geared company.

Chapter 16: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 297

(1) WACC

The WACC in a geared company and the WACC in an identical but ungeared

(all-equity) company are the same:

WACC

G

= WACC

U

(2) Total value of the company (equity plus debt capital)

The total value of an ungeared company is equal to the total value of an

identical geared company (combined value of equity + debt capital):

V

G

= V

U

This total value can be calculated for a company with constant annual

operating profits (profits before interest) as:

Annual operating profits/WACC.

(3)

Cost of equity

The cost of equity in a geared company is higher than the cost of equity in an

ungeared company, by an amount equal to:

the difference between the cost of equity in the ungeared company and the

cost of debt (K

EU

– K

D

)

multiplied by the ratio of the market value of debt to the market value of

equity in the geared company (D/E).

()

DEUEUEG

KK

E

D

KK −+=

where

K

EG

= the cost of equity in a geared company

K

EU

= cost of equity in an ungeared company

K

D

= the cost of debt in the geared company

D = the market value of debt capital in the geared company

E = the market value of equity in the geared company

Example

An all-equity company has a market value of $60 million and a cost of equity of 8%.

It borrows $20 million of debt finance, costing 5%, and uses this to buy back and

cancel $20 million of equity. Tax relief on debt interest is ignored.

Required

According to Modigliani and Miller, if taxation is ignored, what would be the effect

of the higher gearing on (a) the WACC (b) the total market value of the company

and (c) the cost of equity in the company?

Paper F9: Financial management

298 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

According to Modigliani and Miller:

(a)

WACC. The WACC in the company is unchanged, at 8%.

(b)

Total value. The total market value of the company with gearing is identical

to the market value of the company when it was all equity, at $60 million. This

now consists of $20 million and $40 million equity ($60 million – $20 million of

debt)

(c)

Cost of equity. The cost of equity in the geared company is

8%+

20

40

× 8 −5

()

⎡

⎣

⎢

⎤

⎦

⎥

% = 9.5%

Example

A company has $500 million of equity capital and $100 million of debt capital, all at

current market value. The cost of equity is 14% and the cost of the debt capital is 8%.

The company is planning to raise $100 million by issuing new shares. It will use the

money to redeem all the debt capital.

Required

According to Modigliani and Miller, if the company issues new equity and redeems

all its debt capital, what will be the cost of equity of the company after the debt has

been redeemed? Assume that there is no corporate taxation.

Answer

In the previous example, the Modigliani-Miller formulae were used to calculate a

cost of equity in a geared company, given the cost of equity in the company when it

is ungeared (all-equity). This example works the other way, from the cost of equity

in a geared company to a cost of equity in an ungeared company. The same

formulae can be used.

Using the known values for the geared company, we can calculate the cost of equity

in the ungeared company after the debt has been redeemed.

()

DEUEUEG

KK

E

D

KK −+=

()

8.0K

500

100

K0.14

EUEU

−+=

1.2 K

EU

= 14.0 + 1.6

K

EU

= 13.0% (= 15.6/1.2).

Chapter 16: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 299

Exercise 2

A company has $80 million of equity capital, which costs 10% and $20 million of

debt capital that costs 5%. The company borrows $20 million of debt finance, costing

5%, and uses this to buy back and cancel $20 million of equity.

According to Modigliani and Miller, ignoring corporate taxation, what will be:

(a)

the WACC of the company after the increase in gearing

(b)

the market value of equity in the company after the increase in gearing, and

the cost of equity in the company after the increase in gearing.

(Hint: To calculate the new cost of equity, calculate the cost of equity in an all-equity

company first, and then calculate the cost of equity for the company at its new level

of gearing.)

5.3 The Modigliani-Miller view: allowing for corporate taxation

Modigliani and Miller revised their arguments to allow for corporate taxation and

the fact that there is tax relief on interest. You do not need to know the arguments

they used to reach their conclusions, but you must know what their conclusions

were.

Modigliani and Miller argued that allowing for corporate taxation and tax relief on

interest, an increase in gearing will have the following effect:

As the level of gearing increases, there is a greater proportion of cheaper debt

capital in the capital structure of the firm. However, the cost of equity rises as

gearing increases.

As gearing increases, the net effect of the greater proportion of cheaper debt and

the higher cost of equity is that the WACC becomes lower. Increases in gearing

therefore result in a reduction in the WACC.

The WACC is at its lowest at the highest practicable level of gearing.

There are practical limitations on gearing that stop it from reaching very high

levels. For example, lenders will not provide more debt capital except at a much

higher cost, due to the high credit risk or insolvency risk.

The conclusions that MM reached were that:

The total value of the company is higher for a geared company than for an

identical all-equity company.

The value of a company will rise, for a given level of annual cash profits before

interest and tax, as its gearing increases.

There is an optimum level of gearing that a company should be trying to

achieve. A company should be trying to make its gearing as high as possible, to

the maximum practicable level, in order to maximise its value.

A graph showing the relationship between WACC and gearing, according to MM’s

theory with taxation, is as follows:

Paper F9: Financial management

300 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Modigliani-Miller view of gearing and the WACC: with taxation

Modigliani-Miller formulae: allowing for taxation

There are three formulae for the Modigliani and Miller theory, allowing for

corporate taxation. These are shown below. The letter ‘

U

’ refers to an ungeared

company (all-equity company) and the letter ‘

G

’ refers to a geared company.

(1)

WACC

The WACC in a geared company is lower than the WACC in an all-equity

company, by a factor of

1−

Dt

D + E

()

.

WACC

G

= WACC

U

1−

Dt

D + E

()

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

where t is the rate of taxation.

(2)

Value of a company

The total value of a geared company (equity + debt) is equal to the total value

of an identical ungeared company plus the value of the ‘tax shield’. This is the

market value of the debt in the geared company multiplied by the rate of

taxation (Dt).

V

G

= V

U

+Dt

(3)

Cost of equity

The cost of equity in a geared company is higher than the cost of equity in an

ungeared company, by a factor equal to:

the difference between the cost of equity in the ungeared company and the

cost of debt, (K

EU

– K

D

)

multiplied by the ratio

1−t

()

×

D

E

.

K

EG

= K

EU

+

1− t

()

D

E

K

EU

−K

D

(

)

Chapter 16: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 301

When making calculations for the effect of gearing on the WACC and cost of equity,

when you allow for taxation, it is usually necessary to begin by calculating the effect

of a change in gearing on total market value and the market value of equity. In other

words, you will usually have to begin with the formula V

G

= V

U

+ Dt.

Example

An all-equity company has a market value of $60 million and a cost of equity of 8%.

It borrows $20 million of debt finance, costing 5%, and uses this to buy back and

cancel $20 million of equity. The rate of taxation on company profits is 25%.

According to Modigliani and Miller:

(a)

Market value

The market value of the company after the increase in its gearing will be:

V

G

= V

U

+Dt

V

G

= $60 million + ($20 million × 0.25) = $65 million.

The market value of the debt capital is $20 million; therefore the market value

of the equity in the geared company is $45 million ($65 million – $20 million).

(b)

WACC of the geared company

The WACC of the company after the increase in its gearing is calculated as

follows:

WACC

G

= WACC

U

1−

Dt

D + E

()

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

WACC

G

= 8% 1−

$20 million × 25%

()

$65 million

()

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

= 8% 0.9231

()

= 7.38%

(c)

Cost of equity in the geared company

K

EG

= K

EU

+

1− t

()

D

E

K

EU

−K

D

(

)

K

EG

= 8% + 20

1−0.25

()

45

× 8 − 5

()

⎡

⎣

⎢

⎤

⎦

⎥

% = 8% + 1% = 9%

Check: the WACC can now be calculated as follows:

Sourceoffinance Market

value

Cost Marketvaluex

Cost

$million r MVxr

Equity 45.00 0.09 4.05

Debt(after‐taxcost) 20.00 0.0375 0.75

65.00 4.80

WACC =

4.80

65.00

= 0.0738 or 7.38%

Paper F9: Financial management

302 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Pecking order theory

Preferred sources of finance

Ease of obtaining finance

6 Pecking order theory

6.1 Preferred sources of finance

Pecking order theory is a view about how companies seek to raise new capital that

contradicts views of capital structure based on Modigliani and Miller theory or the

traditional view of WACC.

Pecking order theory suggests that when companies try to raise new capital, they

are not concerned with minimising the WACC. They look for cheap capital and

convenient access to new capital.

Many companies have a preferred order for sources of finance as follows.

Retained earnings

New debt

New equity

It therefore goes against the theory that companies have a unique combination of

debt and equity which will minimise their cost of capital.

6.2 Ease of obtaining finance

The reason for the order of preference of sources of finance may be due to the ease

of obtaining the finance.

Retained earnings are easily accessible and have no issue costs. To obtain

retained earnings, all a company needs to do is to be profitable and keep

dividends below the total amount of earnings. Financial managers might

therefore consider retained earnings to have no cost, although this is not correct.

It is cheaper to raise debt finance than equity and it is possible to raise smaller

amounts when required. Bank finance in particular is relatively quick and

inexpensive to obtain, even though the bank will charge an arrangement fee for

any loan that it provides.

The cost of raising capital by issuing new shares for cash is quite high. They

include for example the costs of professional fees of investment banking

advisers, accountants and lawyers, underwriting fees, costs of meeting

regulatory requirements and so on.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 303

Paper F9

Financial management

CHAPTER

17

Capital asset pricing model

(CAPM)

Contents

1 Riskandinvestments

2 Componentsofthecapitalassetpricingmodel

(CAPM)

3Thecostofcapitalforcapitalinvestment

appraisal

4Project‐specificdiscountrates

Paper F9: Financial management

304 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Risk and investments

Risk and return in investments

What is investment risk?

Diversification to reduce risk: building an investment portfolio

Systematic and unsystematic risk

1 Risk and investments

1.1 Risk and return in investments

Investors invest in shares and bonds in the expectation of making a return. The

return that they want from any investment could be described as:

a return as reward for providing funds and keeping those funds invested, plus

a return to compensate the investor for the risk.

As a basic rule, an investor will expect a higher return when the investment risk is

higher.

1.2 What is investment risk?

Investors in bonds, investors in shares and companies all face investment risk.

In the case of bonds, the risks for the investor are as follows:

The bond issuer may default, and fail to pay the interest on the bonds, or fail to

repay the principal at maturity.

There may be a change in market rates of interest, including interest yields on

bonds. A change in yields will alter the market value of the bonds. If interest

rates rise, the market value of bonds will fall, and the bond investor will suffer a

loss in the value of his investment.

In the examination, you might be told to assume that debt capital is risk-free for the

purpose of analysing the cost of equity. In practice however, only government debt

denominated in the domestic currency of the government is risk-free.

In the case of equity shares, the risks for the investor are that:

the company might go into liquidation, or,

much more significantly, the company’s profits might fluctuate, and dividends

might also rise or fall from one year to the next.

For investors in equities, the biggest investment risk comes from uncertainty and

change from one year to the next in annual profits and dividends. Changes in

expected profits and dividends will affect the value of the shares. Bigger risk is

associated with greater variability in annual earnings and dividends.