ACCA F6 FA09 Study Text 2010

Подождите немного. Документ загружается.

Chapter 1: The UK tax system

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 25

2.6 Value added tax

VAT is payable on most goods and services purchased by consumers.

2.7 Stamp duty

Stamp duty is payable on the sale of land and buildings and shares.

2.8 Direct and indirect taxation

All of the above taxes can be classified as either direct or indirect taxation.

Direct taxation

This is where a taxpayer pays their tax directly to HM Revenue & Customs

(HMRC). Examples of direct taxes include income tax, corporation tax, capital gains

tax and inheritance tax.

Indirect taxation

This is where tax, such as VAT, is paid indirectly to HM Revenue & Customs. The

consumer pays indirect taxes to the supplier, who then pays the tax to HMRC.

Paper F6 (UK): Taxation FA2009

26 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Principle sources of revenue law and practice

Ths structure of the UK tax system

The different sources of revenue law

The interaction of the UK tax system with that of other tax jurisdictions

3 Principal sources of revenue law and practice

3.1 The structure of the UK tax system

The structure of the UK tax system can be shown as follows:

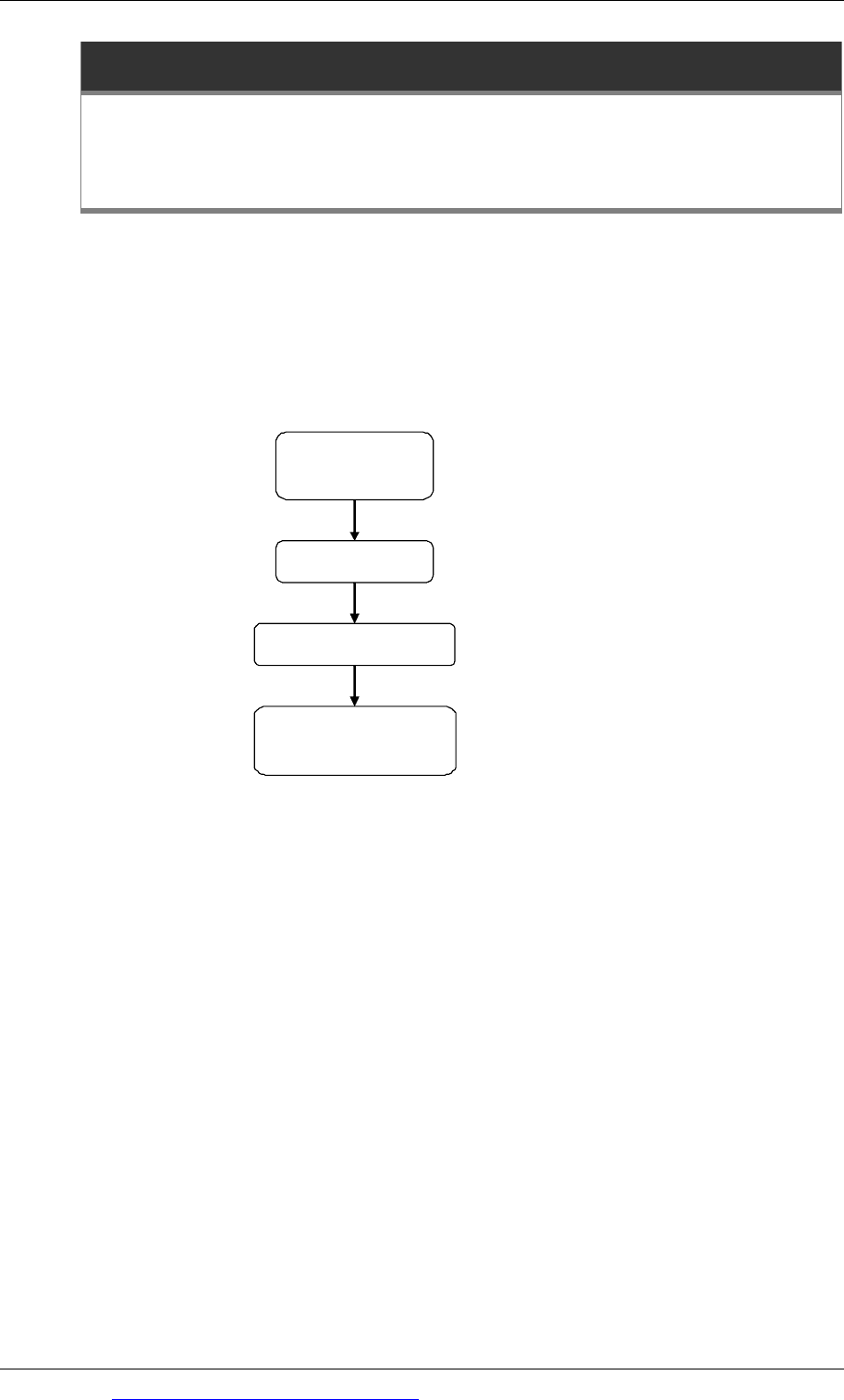

Chancellor of the Exchequer

The Chancellor has the overall responsibility for the UK tax system and one of his

roles includes producing the Budget each year.

The Treasury

The Treasury is the ministry responsible under the Chancellor for the imposition

and collection of taxation.

The Commissioners

The Treasury appoint permanent civil servants, the Commissioners for HM

Revenue and Customs.

Their duties include:

Administering the UK tax system

Implementing tax law.

Treasury

Commissioners

HM Revenue and Customs

Chancellor of the

Exchequer

Chapter 1: The UK tax system

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 27

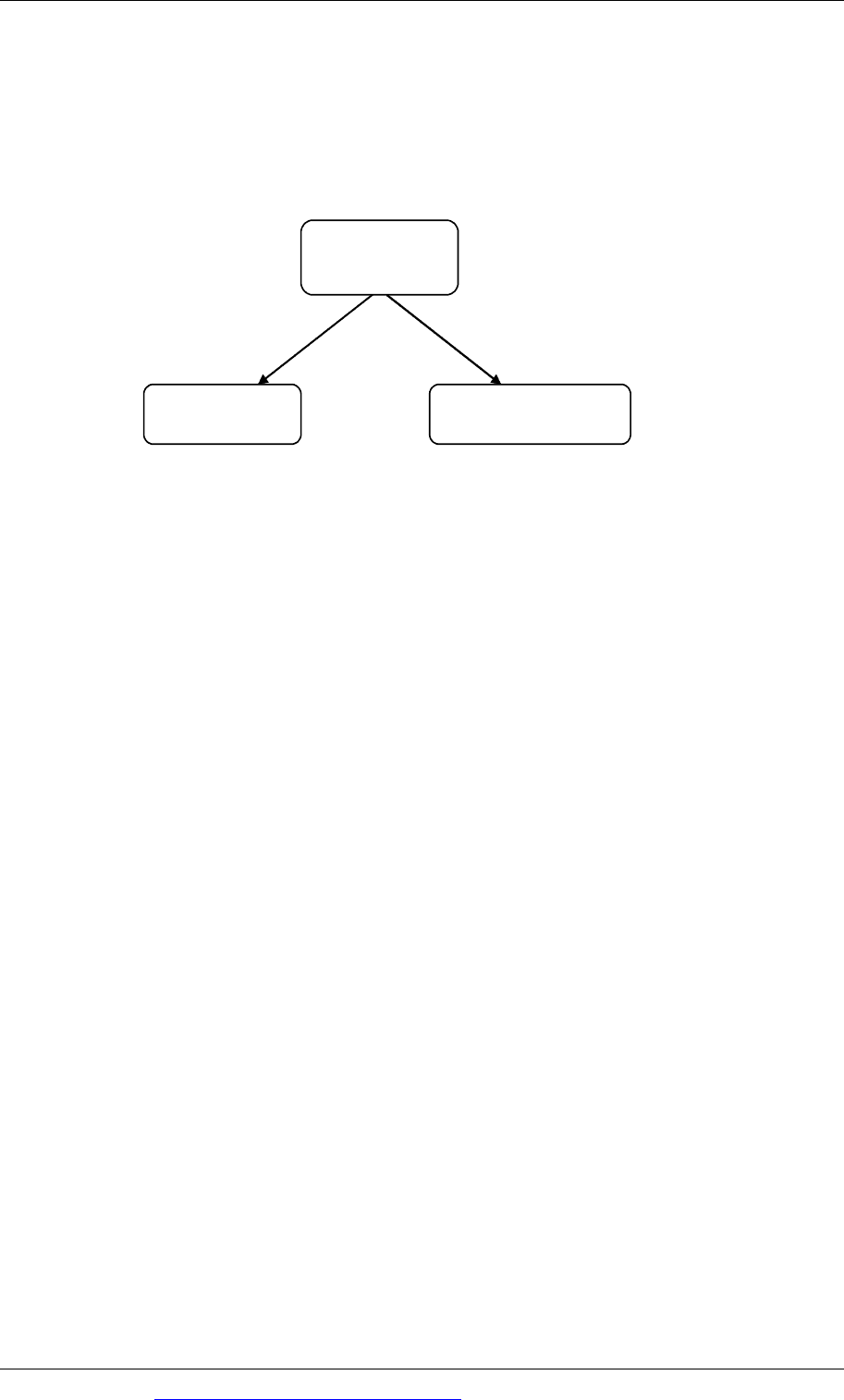

HM Revenue and Customs

HM Revenue and Customs (HMRC) is a single body that controls and administers

all areas of UK tax law.

The structure of HM Revenue and Customs can be shown as follows:

District offices

The Commissioners appoint Officers of HMRC to carry out the day to day work of

managing the tax system. Their roles include:

Issuing tax returns

Examining tax returns and accounts

Calculating tax liabilities under the self assessment tax systems and PAYE.

Accounts and payments offices

Accounts and payments offices deal with the collection and payment of tax.

3.2 The different sources of revenue law

Although tax law constantly changes, it has been established over a long period of

time.

The different sources of revenue law are as follows:

Tax legislation and statutes

Tax legislation/statutes are the main source of revenue law. Each year, following

the Budget, the legislation is updated by passing a new Finance Act.

In addition to Acts of Parliament, the government issues statutory instruments

which add detail, where needed, to any part of the legislation.

Case law

Case law refers to the decisions made in tax cases tried and tested through the

courts. The results of cases that have been through the courts tend to set a precedent

for the tax treatment of a particular item.

District Offices

Accounts and Payments

offices

HM Revenue and

Customs

Paper F6 (UK): Taxation FA2009

28 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

HMRC manuals

HMRC have their own manuals that are used by the Officers of HMRC. These

manuals are also available for use by the general public. You can view them by

using the search facility on the HMRC website – www.hmrc.gov.uk.

HMRC guidance

As the tax legislation can be complex to understand and is also open to

misinterpretation, further guidance is issued by HMRC in order to:

explain how to implement the law

give their interpretation of the law.

The main statements of guidance are as follows:

Statements of practice - These explain how the tax law is applied in a particular

situation.

Extra-Statutory Concessions – These are sometimes available to soften areas of

tax law where it would seem to be unduly harsh or unfair. These concessions

usually have to be claimed and sometimes taxpayers are unaware that they are

available.

Press Releases - These provide news of topical tax issues that arise during the

year.

Leaflets - Leaflets are available on all types of tax topics and they are an

informative source of revenue law to the general public. For instance, the

Revenue leaflet on ‘residence’ explains all the relevant issues in a way that is

understandable to most taxpayers.

3.3 The interaction of the UK tax system with that of other tax jurisdictions

The UK’s tax law uses the concepts of residence, ordinary residence and domicile to

determine how an individual or entity is taxed. However, overseas countries will

also have their own tax laws and practices.

It is therefore possible for an individual to be liable to tax in more than one country

at the same time, under completely different tax rules.

A tax treaty, or agreement, between two countries may over-rule the tax law of one

or both of those countries. In this case, the individual or entity is taxed in

accordance with the tax treaty.

However, if there is no treaty between two countries, an individual or entity may be

taxed in both countries. As this is unfair, double taxation relief will apply.

Double Taxation Relief and will be covered in detail a in later chapter.

Chapter 1: The UK tax system

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 29

Tax avoidance and tax evasion

The difference between tax avoidance and tax evasion

The need for an ethical and professional approach

4 Tax avoidance and tax evasion

4.1 The difference between tax avoidance and tax evasion

It is important to know the difference between tax avoidance and tax evasion, as the

consequences of getting it wrong can be very different.

Tax avoidance

Tax avoidance is legal. It involves complying with the tax legislation in such a way

as to minimise a taxpayer’s tax liability.

For example, an individual arranging their will in such a way as to minimise

their inheritance tax liability is using tax planning opportunities and avoiding

tax in a legal way in accordance with the tax law.

Another example may be an individual making a capital gains tax election to tax

the disposal of their business in such a way as to minimise their capital gains tax

liability.

Tax evasion

Tax evasion is illegal. It involves reducing your tax liability in a way that is not

following the tax legislation.

For example, tax evasion is deliberately omitting some investment income from

a tax return in order not to pay tax on that source of income.

Another example of tax evasion is to overstate expenses, in order to reduce the

tax liability.

Any taxpayer who carries out tax evasion could face criminal prosecution, including

penalties, surcharges, interest and sometimes imprisonment.

4.2 The need for an ethical and professional approach

ACCA expects its members to:

Adoptanethicalapproachtowork,employersandclients.

Acknowledgetheirprofessionaldutytosocietyasawhole.

Maintainanobjectiveoutlook.

Provideprofessional,highstandardsofservice, conduct andperformanceat all

times.

Paper F6 (UK): Taxation FA2009

30 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

ACCA’s ‘Code of Ethics and Conduct’ sets out five fundamental principles, which

help members to meet these expectations:

Integrity - Members should act in a straightforward and honest manner in

performing their work.

Objectivity - Members should not allow prejudice, or bias, or the influence of

others to override objectivity.

Professional competence and due care - Members should not undertake work

that they are not competent to carry out. Members have an ongoing duty to

maintain professional knowledge and skills. A member should carry out their

work with due care having regard to the nature and scope of the assignment.

Confidentiality - Members should respect the confidentiality of information

acquired as a result of professional and business relationships and should not

disclose any such information to third parties unless:

- they have proper and specific authority; or

- there is a legal or professional right or duty to disclose e.g. Money

Laundering.

Confidential information acquired as a result of professional and business

relationships should not be used for the personal advantage of members or third

parties.

Professional behaviour - Members should refrain from any conduct that might

bring discredit to the profession.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 31

Paper F6 (UK)

Taxation FA2009

CHAPTER

2

Introduction to income tax

Contents

1 Overview of income tax

2 The taxable income statement

3 Computation of income tax liability

4 Computation of income tax payable

5 Gift Aid donations paid by individuals

6 Personal Age Allowance

7 Tax planning for married couples

Paper F6 (UK): Taxation FA2009

32 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Overview of income tax

The basic charging rules

Taxable income

The tax year

Preparing an income tax computation

1 Overview of income tax

1.1 The basic charging rules

Individuals are liable to pay income tax on their taxable income for a tax year.

The scope of income tax for individuals is as follows:

Taxable person: Liable on:

UK resident individual Worldwide taxable income

Non-UK resident individual UK income only

There is no statutory definition of the term ‘resident’. An individual is generally

considered to be resident in the UK if:

he is physically present in the UK for 183 days or more in the tax year, or

he makes frequent and substantial visits to the UK. Visits are classed as frequent

if they occur for four consecutive years and are substantial if they average three

months a year.

1.2 Taxable income

Individuals are liable to:

income tax on their taxable income, and

a separate tax, capital gains tax, on their chargeable gains.

Taxable income is defined as:

income generated from all sources which is not specifically exempt, minus

tax allowable interest payments and personal allowances.

Taxable income is listed in a taxable income statement according to its nature and

source.

Chapter 2: Introduction to income tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 33

1.3 The tax year

Income tax rates and allowances are fixed for each tax year. A tax year is the period

from 6 April in one year to the following 5 April.

Tax years are quoted as the calendar years in which the tax year begins and ends.

For example, the tax year 2009/10 is the period from 6 April 2009 to 5 April 2010.

Income tax is based on the income relating to a particular tax year. For the 2010

examinations, questions will be based on the 2009/10 tax year.

The tax year is sometimes referred to as the fiscal year or the year of assessment.

1.4 Preparing an income tax computation

There are three key steps in the preparation of an income tax computation.

Step 1: Prepare a statement of taxable income for the tax year

The first step is to prepare a statement listing all the income that is chargeable to

income tax in the tax year, after deducting allowable interest payments and personal

allowances.

Step 2: Calculate the income tax liability

The next step is to calculate the income tax liability on the taxable income. Income

tax rates need to be applied carefully, as different types of income are taxed at

different rates of tax.

Step 3: Calculate the income tax payable

The last step, which may be required in some examination questions, is to calculate

how much of the income tax liability is still payable after taking account of any tax

already deducted at source. If required, the due dates of payment of income tax still

payable and the filing dates for self-assessment return forms need to be stated.

Each step involved in calculating the income tax payable is explained in more detail

in the rest of this chapter. Self-assessment is explained in a later chapter.

Paper F6 (UK): Taxation FA2009

34 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The taxable income statement

Overview of the taxable income statement

Classification of income

Employment income

Trading income

Property income

Savings income

UK dividends received

Interest payments

Personal allowance

Taxable income and exempt income

2 The taxable income statement

2.1 Overview of the taxable income statement

The first step in preparing an income tax computation is to produce a list of the

sources of income which are taxable. This should be presented as follows:

Name of individual

Income tax computation: 2009/10

See paragraph

£

Earned income

Employment income

2.3

X

Trading income

2.4

X

Property income

2.5

Savings income (gross)

2.6

Building society interest (amount received × 100/80)

X

Bank interest (amount received × 100/80)

X

Dividends received (amount received × 100/90)

2.7

X

–––––––––––––––––––––––––––––

–

–

Totalincome

X

Minus Interest payments

2.8

(X)

–––––––––––––––––––––––––––––

–

–

Netincome X

Minus Personalallowance(PA) 2.9 (6,475)

–––––––––––––––––––––––––––––

–

–

Taxableincome 2.10 X

–––––––––––––––––––––––––––––

–

–

The items in this statement are explained in more detail in the following sections.